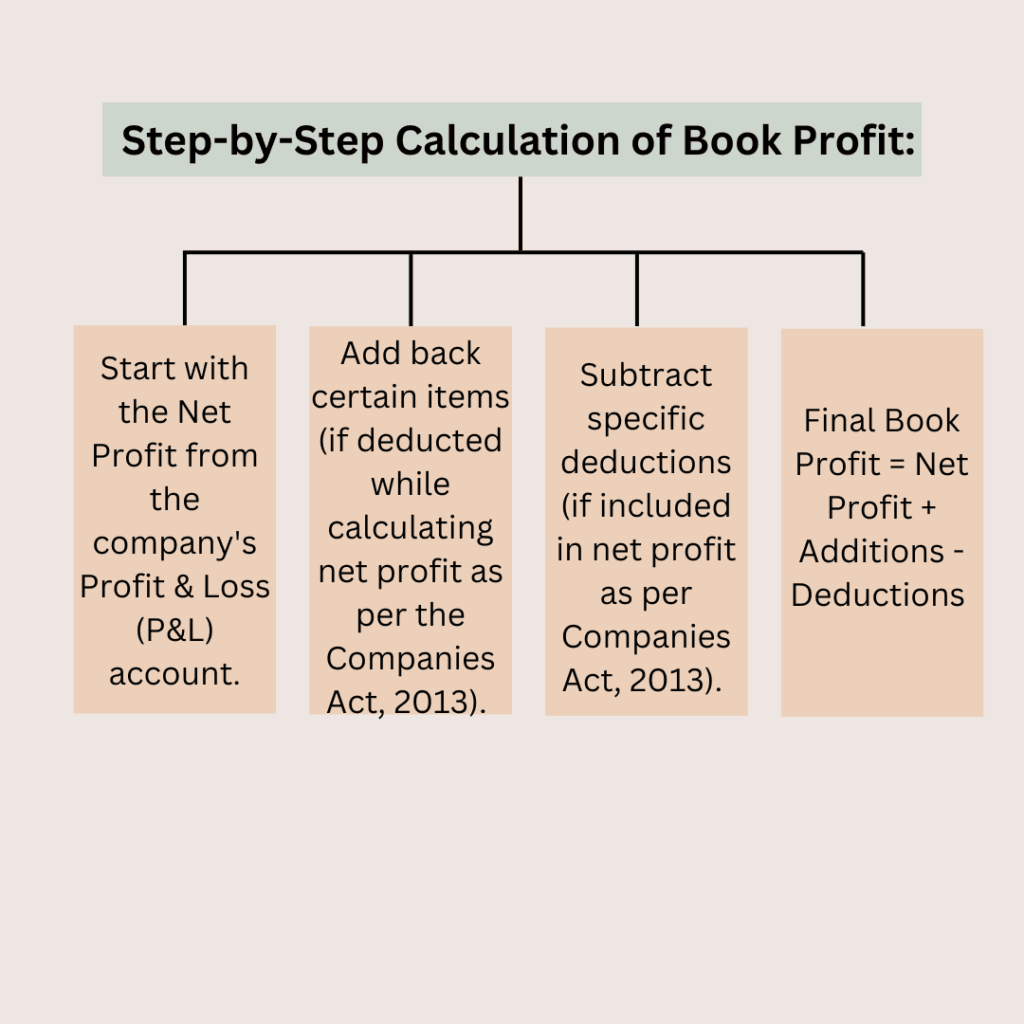

Book profit is your company’s profit adjusted for tax purposes under Section 115JB MAT. Unlike regular income, it’s calculated from your Profit & Loss Account with specific additions and deductions. This post shows you 4 simple steps to calculate it correctly, with a real ₹10 crore example to walk through.

What is Book Profit?

Book Profit is the adjusted net profit of a company, calculated based on its Profit & Loss Account as per the Companies Act, 2013, with specific additions and deductions under Section 115JB. This is different from your taxable income because:

- It includes items deducted in your financial statements but added back for tax purposes (like income tax and dividends paid).

- It excludes items that are exempt from tax (like dividend income from foreign subsidiaries).

It’s used to calculate MAT (Minimum Alternate Tax), ensuring companies with high book profits pay at least 15% tax.

How to Calculate Book Profit in 4 Steps (With Real ₹10 Crore Example)

The formula for book profit is straightforward:

Book Profit = Net Profit (from P&L) + Additions – Deductions

Step 1: Start with Net Profit from the P&L Account

Take the net profit before tax from your company’s Profit & Loss Account (prepared as per the Companies Act, 2013, not the Income Tax Act).

Example in Our ₹10 Crore Case:

| Item | Amount |

| Net Profit Before Tax | ₹10 Crore |

Step 2: Add Back Specified Items (Additions)

Add back the following amounts to your net profit (if they were deducted while calculating net profit under the Companies Act):

Common Additions to Book Profit:

- Income Tax Paid or Payable (including current and deferred tax)

- Dividends Paid or Proposed by the company

- Transfers to Reserves/Funds (General Reserve, Statutory Reserve, etc., but NOT Depreciation Reserve)

- Provisions for Subsidiary Losses (if your subsidiary made a loss)

- Deferred Tax and Other Provisions (for contingencies, doubtful debts, etc.)

- Depreciation (Companies Act basis) (if it differs from Income Tax Act depreciation)

- Expenditure Related to Exempt Income (e.g., expenses of agricultural income)

- Revaluation Reserve Adjustments (if debited to P&L)

Example: Additions in Our ₹10 Crore Case

| Addition Item | Amount |

| 1. Income Tax Paid | ₹50 Lakh |

| 2. Transfer to General Reserve | ₹1 Crore |

| 3. Depreciation (Companies Act) | ₹2 Crore |

| Total After Additions | ₹13.5 Crore |

Step 3: Deduct Specified Items (Deductions)

Subtract the following amounts from the total after additions (if they were included in net profit but should be excluded for MAT purposes):

Common Deductions from Book Profit:

- Income Exempt from Tax (e.g., agricultural income, dividend from foreign subsidiaries, income from SEZ units)

- Amounts Withdrawn from Reserves (if credited back to P&L)

- Depreciation as per Income Tax Act (instead of Companies Act depreciation, if different)

- Long-Term Capital Gains (if not taxable under normal provisions)

- Income from Life Insurance Business (if applicable)

- Share of Profit from Partnership Firms (if already included in P&L)

Example: Deductions in Our ₹10 Crore Case

| Deduction Item | Amount |

| 1. Dividend from Foreign Subsidiary (Exempt) | ₹1.5 Crore |

| 2. Depreciation as per Income Tax Act | ₹1.8 Crore |

| Total Deductions | ₹3.3 Crore |

Step 4: Calculate Final Book Profit

Apply the formula from Step 1:

Final Book Profit = Total After Additions – Total Deductions

Final Calculation for Our Example:

| Calculation Step | Amount |

| Step 1: Net Profit (from P&L) | ₹10.00 Cr |

| Step 2: Add All Additions | + ₹3.50 Cr |

| Subtotal (Before Deductions) | ₹13.50 Cr |

| Step 3: Deduct All Deductions | – ₹3.30 Cr |

| FINAL BOOK PROFIT | ₹10.20 Cr |

Bonus: How to Calculate MAT Based on Book Profit

Once you have your final book profit, calculating MAT is simple. Apply 15% to your book profit, then add 4% Health & Education Cess on the tax amount:

| MAT Calculation | Amount |

| Book Profit | ₹10.20 Cr |

| MAT Rate @ 15% | ₹1.53 Cr |

| Health & Education Cess @ 4% | ₹6.12 Cr |

| TOTAL MAT PAYABLE | ₹1.59 Cr |

Key Takeaways: Remember These 4 Rules

- Book Profit is NOT the same as taxable income — it’s calculated from your Companies Act P&L, not your tax return.

- Always start with Net Profit before tax from your audited financial statements.

- Add back items already deducted, like income tax paid, dividends, and reserve transfers.

- Deduct exempt income and adjust depreciation to the Income Tax Act basis.

Common Mistakes to Avoid

- Using taxable income instead of book profit: These are calculated on different bases. Always use the Companies Act P&L for book profit.

- Forgetting to add back depreciation reserve: Unlike other reserves, depreciation reserve should NOT be added back.

- Missing adjustments for different depreciation: If your Companies Act depreciation differs from Income Tax Act depreciation, make the adjustment carefully.

Conclusion: Master Book Profit to Master MAT

Book profit calculation is crucial for any company liable to pay MAT under Section 115JB. By following these 4 simple steps — starting with net profit, adding specified items, deducting exempt income, and calculating the final figure you can confidently compute your book profit and understand your minimum tax obligation.

Use the ₹10 crore example in this post as a template for your own numbers. If you have a complex business structure (subsidiary companies, multiple reserves, or deferred tax items), consult your CA or tax advisor to ensure accuracy.

FAQ

Who is liable to calculate book profit?

All domestic companies are required to calculate book profit for MAT purposes. This includes private companies, public companies, and even companies with no taxable income.

Can book profit ever be negative?

Yes. If your net profit is negative or if deductions exceed additions, book profit can be negative. In such cases, MAT is not payable.

What happens if my tax on normal income exceeds MAT?

If your tax calculated on normal taxable income is higher than MAT, you pay the higher amount (normal tax). MAT is a minimum tax, so it only applies when your normal tax is lower.

Can I carry forward MAT credit?

Yes. MAT credit can be carried forward for 15 assessment years. If you pay MAT in one year but your normal tax is higher in future years, you can use the MAT credit to offset the excess tax paid.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.