The cryptocurrency market has matured significantly over the past few years, and so have the regulatory frameworks governing it. If you’re a crypto investor operating across borders or considering your options in 2026, understanding how the United States and India approach digital asset taxation is no longer optional—it’s essential.

Two major markets. Two completely different philosophies. One dramatic difference in tax outcomes.

While the US has evolved a more nuanced system over the past decade, India took a harder line in 2022 and has maintained a strict, flat-rate approach ever since. For someone holding digital assets or trading cryptocurrency on both sides of the world, this comparison matters—sometimes to the tune of hundreds of thousands of rupees or dollars.

This guide breaks down exactly how each system works, explores the gaps between them, and helps you understand what 2026 really means for your crypto portfolio if you’re navigating both jurisdictions.

India’s Crypto Tax Framework – The 30% VDA Tax Regime

The Indian Approach: Simplicity Through Rigidity

India’s crypto taxation system, solidified through the Finance Act 2022, operates on a principle that sounds straightforward but proves remarkably inflexible in practice: a blanket 30% tax on all virtual digital asset gains.

What is a Virtual Digital Asset (VDA)?

Under Section 2(47A) of the Income Tax Act, a VDA is any digitally generated token or code that represents value, can be transferred or traded, and exists electronically. This remarkably broad definition includes:

- Cryptocurrencies (Bitcoin, Ethereum, altcoins)

- NFTs (officially notified ones)

- Governance and DeFi tokens

- Stablecoins (despite their “stability” branding)

Conspicuously absent: the Indian Rupee and foreign currencies. Also exempt: the RBI’s own Digital Rupee, because it’s legal tender and falls outside the speculative asset framework.

The Three Tax Anchors in India:

- Section 115BBH – The 30% flat tax on VDA gains

- Section 194S – The 1% TDS on crypto transfers (tracking mechanism)

- Section 56(2)(x) – Income from airdrops and gifts at slab rates

India’s 30% Flat Tax: How It Actually Works

The math looks deceptively simple: Gain = Sale Price – Purchase Price, then multiply by 30%.

But the devil hides in several details:

What You Can Deduct: Only the cost of acquisition. Nothing else.

What You Cannot Deduct:

- Exchange fees

- Gas fees

- Trading commissions

- Slippage costs

A trader who pays ₹5,000 in exchange fees to execute a ₹2,00,000 trade can’t reduce their taxable gain by even a rupee. The system doesn’t recognize transaction friction.

The Add-Ons:

- 4% health and education cess (applies to all income)

- Surcharges if your total income exceeds:

- ₹50 lakh (10%)

- ₹1 crore (15%)

- ₹2 crore (25%)

- ₹5 crore (37%)

For most Indian crypto investors, the effective rate lands around 31.2%. For higher earners, it climbs notably higher.

The Loss Problem: India’s Most Controversial Rule

This is where India’s system generates the most friction.

You cannot offset crypto losses against crypto gains. Not even partially.

If you make ₹3,00,000 on Bitcoin and lose ₹1,50,000 on Ethereum, you owe tax on the full ₹3,00,000. The loss simply vanishes.

Moreover:

- You cannot offset crypto losses against any other income (salary, stock gains, business income)

- You cannot carry losses forward to future years

- The loss expires entirely on March 31

For active traders who experience inevitable losing trades, this creates a tax burden that feels disproportionate to actual profitability.

Tax on Crypto Swaps: A Hidden Tax Event

Many investors don’t realize that swapping one cryptocurrency for another—say, ETH for SOL—is treated as a taxable event in India.

Why? Because the law defines a “transfer” as any exchange that results in a change of beneficial ownership, regardless of whether cash is involved.

So if you swap 2 ETH (worth ₹5,40,000) for SOL:

- Deemed sale value: ₹5,40,000

- Cost basis: ₹3,00,000

- Taxable gain: ₹2,40,000

- Tax at 30%: ₹72,000

You now owe ₹72,000 in tax… without receiving any cash. For liquidity, you’d need to sell some SOL or other holdings to cover this liability.

The 1% TDS Mechanism: Tracking, Not Necessarily Taxation

Section 194S mandates a 1% Tax Deducted at Source on crypto transfers. Think of it as a tracking mechanism disguised as a tax.

How it works:

- When you sell on an exchange: the platform deducts 1% automatically

- When you engage in P2P trades: the buyer is legally responsible for deducting 1%

Important: This 1% is not “extra” tax. It’s an advance payment credited against your final tax liability.

Thresholds:

- ₹50,000 per year for most individual traders

- ₹10,000 per year for businesses and high-frequency traders

Once you cross the threshold, every transaction gets hit with 1% deduction for the rest of that financial year.

Filing VDA Income: Schedule VDA

When you file your ITR, crypto income gets reported separately in Schedule VDA. The system requires:

- Asset type (Bitcoin, Ethereum, specific NFT, etc.)

- Acquisition date and cost

- Sale/transfer date and value (in INR)

- Resulting gain

- TDS deducted

For active traders with dozens or hundreds of transactions, this becomes tedious but manageable through aggregation.

Foreign Assets & Offshore Exchanges: Schedule FA

If you use foreign exchanges or hold crypto in offshore wallets, you must declare it in Schedule FA.

The stakes here are higher. Non-disclosure triggers penalties under the Black Money Act:

- 30% tax on the asset value

- 90% penalty

- Minimum ₹10 lakh penalty per asset

This isn’t a slap on the wrist—it’s a serious enforcement mechanism.

US Crypto Tax Framework – Complexity Over Simplicity

The American Approach: Multiple Rate Brackets, Multiple Asset Types

The United States taxes crypto gains far more complexly than India, but arguably more equitably in certain respects.

The IRS classifies most cryptocurrencies as “property” for tax purposes, meaning:

- Sales and exchanges trigger capital gains tax

- Rates depend on holding periods (short-term vs. long-term)

- Rates depend on your income bracket

- Losses can offset gains (with limits)

Short-Term Capital Gains (held ≤ 1 year): Taxed at ordinary income rates:

- 10% (income up to $11,000 for single filers in 2024)

- 12% (up to $44,725)

- 22% (up to $95,375)

- 24% (up to $182,100)

- 32% (up to $231,250)

- 35% (up to $578,125)

- 37% (above $578,125)

Add 3.8% Net Investment Income Tax (NIIT) if modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly), and you’re looking at potential rates exceeding 40%.

Long-Term Capital Gains (held > 1 year): Much more favorable:

- 0% (income up to $47,025 for single filers)

- 15% (up to $518,900)

- 20% (above $518,900)

For most middle-income Americans, long-term gains are taxed at either 0% or 15%—dramatically lower than short-term rates.

The US Advantage: Loss Harvesting

Here’s where the US system differs most sharply from India’s: losses are meaningful.

In the US:

- You can offset capital gains with capital losses dollar-for-dollar

- If losses exceed gains, you can deduct up to $3,000 of losses against ordinary income

- Remaining losses carry forward indefinitely to future years

This enables a practice called “tax-loss harvesting”—selling losing positions to offset gains, then sometimes re-entering similar positions (with timing restrictions).

A trader experiencing a ₹3,00,000 gain and ₹1,50,000 loss can reduce taxable gain to ₹1,50,000. In India, they’d owe tax on the full ₹3,00,000.

Staking Rewards, Airdrops, Mining: Income (Not Capital Gains)

The IRS takes a different view on how you acquire crypto:

Staking rewards: Taxable as ordinary income at fair market value on the date received.

Airdrops: Same—ordinary income at fair market value at the moment of receipt.

Mining: Also ordinary income.

So if you receive 0.1 BTC worth $4,000 in staking rewards, you recognize $4,000 of income in that tax year, regardless of whether you sell it later.

Later, when you sell, that $4,000 becomes your cost basis. Gains above that are capital gains (short or long-term depending on holding period).

This creates the possibility of “phantom income”—tax liability on assets you haven’t sold—which complicates cash flow for some investors.

DeFi Activities: Complex and Evolving

The IRS position on DeFi taxation remains somewhat uncertain, but the prevailing view is:

- Yield farming rewards: Ordinary income at fair market value

- Liquidity pool withdrawals with gains: Capital gains

- Smart contract interactions: Potentially each a taxable event

The tax treatment of complex DeFi strategies often depends on interpretation, and audits occasionally occur in this gray territory.

Wash Sale Rules: Do They Apply to Crypto?

Here’s where it gets interesting. Traditional wash sale rules (preventing loss deduction if you repurchase within 30 days) technically don’t explicitly apply to crypto under current IRS guidance.

However, this ambiguity has drawn regulatory scrutiny, and some tax professionals advise caution about aggressive wash-sale-style strategies with crypto, given that the IRS has been known to take a broader interpretation.

Reporting: Forms 8949 and Schedule D

US investors report capital gains and losses on:

- Form 8949 (Sales of Capital Assets) – detailed transaction list

- Schedule D (Capital Gains and Losses) – summary

- Form 1040-SR or 1040 – final return

Additionally, many exchanges report transactions via Form 1099-K or 1099-B, creating a third-party reporting obligation.

For active traders, this reporting can be extensive.

Foreign Crypto Holdings: FBAR & FATCA

If you hold crypto on foreign exchanges or wallets:

FBAR (Financial Crimes Enforcement Network):

- Mandatory if foreign financial accounts exceed $10,000 at any point in the year

- Cryptocurrency wallets likely qualify as “financial accounts”

- Failure to file carries severe penalties

FATCA (Foreign Account Tax Compliance Act):

- Affects US citizens/residents with foreign assets > $200,000 (varies by category)

- Requires Form 8938

For Americans with substantial offshore crypto holdings, these compliance obligations are serious.

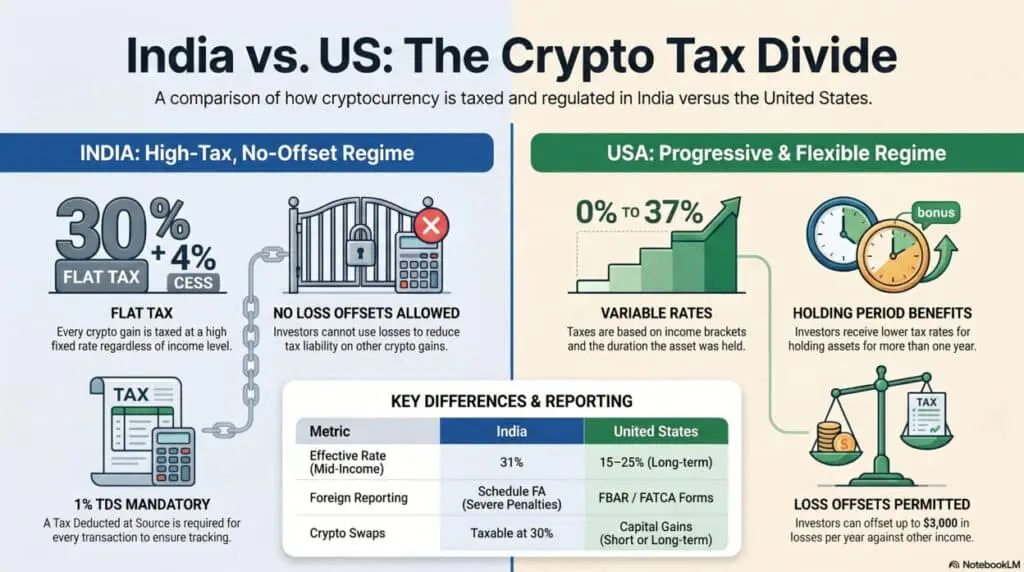

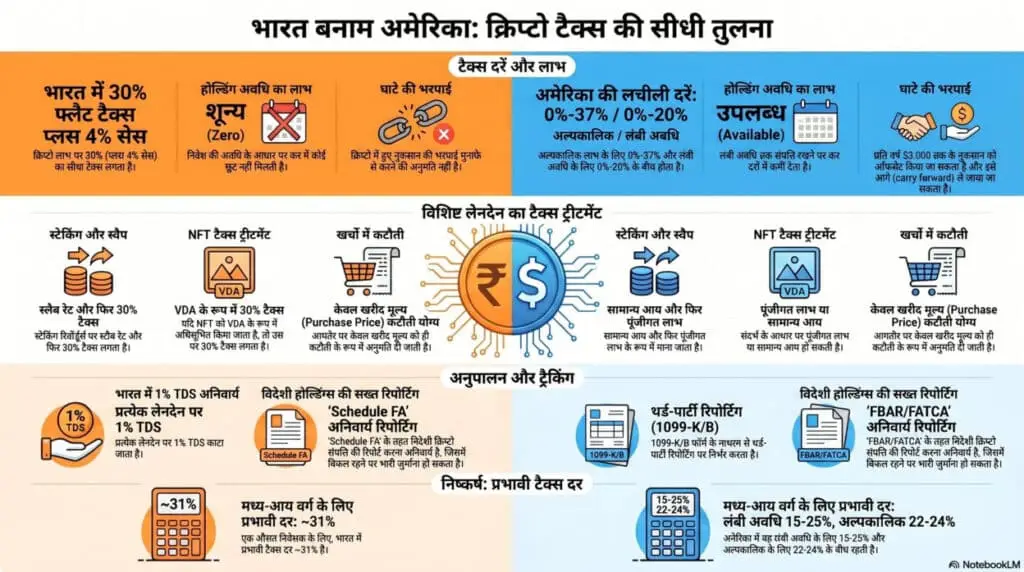

Direct Comparison – India vs. US Crypto Tax Treatment

Comparison Table: Key Metrics

| Aspect | India | US |

|---|---|---|

| Tax Rate on Gains | 30% flat (+ 4% cess) | 0%-37% (short-term) or 0%-20% (long-term) |

| Holding Period Benefit | None | Yes (long-term rate reduction) |

| Loss Offset | Not allowed | Allowed (up to $3,000/year, carry forward) |

| Staking Rewards | Slab rate as income, then 30% on appreciation | Ordinary income, then capital gains on appreciation |

| Crypto Swaps | Taxable at 30% | Capital gains (short or long-term) |

| Expense Deductions | Purchase price only | Generally purchase price only |

| NFT Tax Treatment | 30% (if notified as VDA) | Capital gains or ordinary income (context-dependent) |

| Foreign Crypto Holdings | Must report Schedule FA (severe penalties if not) | Must report FBAR/FATCA (separate forms) |

| Transaction Tracking | 1% TDS mandatory | Third-party reporting (Forms 1099-K/B) |

| Effective Rate (mid-income) | ~31% | ~15-25% for long-term; 22-24% for short-term |

Scenario Comparison: ₹50,00,000 Crypto Gain

Scenario: An investor makes a ₹50,00,000 profit from selling Bitcoin.

In India (assuming no losses):

- Taxable gain: ₹50,00,000

- Tax at 30%: ₹15,00,000

- Cess at 4%: ₹60,000

- Total tax: ₹15,60,000

- Effective rate: 31.2%

In the US (equivalent $60,000 gain for a mid-income taxpayer, held > 1 year):

- Tax at 15%: $9,000

- NIIT (if applicable): potentially +$2,140 (3.8% if > $200k income)

- Total tax: $9,000 – $11,140

- Effective rate: 15% – 18.6%

Advantage: US (assuming long-term holding)

Scenario: Active Trader with Mixed Results

Scenario: A trader generates ₹3,00,000 in gains and ₹1,50,000 in losses.

In India:

- Taxable gain: ₹3,00,000 (losses don’t offset)

- Tax: ₹3,00,000 × 30% = ₹90,000

- Net after-tax return: ₹1,50,000 gain – ₹90,000 tax = ₹60,000 (20% net return)

In the US (assuming mid-income, long-term holdings):

- Net gain: ₹3,00,000 – ₹1,50,000 = ₹1,50,000

- Tax at 15%: ₹22,500

- Net after-tax return: ₹1,27,500 (42.5% net return)

Advantage: US (significantly)

Strategic Implications for Cross-Border Investors

For NRIs and Returning Residents

If you’re an Indian resident but trade on US exchanges, or a US citizen with Indian crypto holdings, your position is complex:

Residential Status Matters:

- Indian residents are taxed on global crypto income (India’s system applies)

- Non-residents are only taxed on Indian-sourced income

- But determining “sourcing” is ambiguous

For US Citizens:

- Worldwide income taxation applies, regardless of residence

- You owe US tax on Indian crypto gains even if not resident in the US

- You may get a foreign tax credit for taxes paid to India

Tax Planning Opportunities (India)

Given India’s rigidity, optimization is limited but possible:

- Timing: Recognize gains in lower-income years if possible

- Asset type: Hold long-term without trading to avoid repeated 1% TDS

- Foreign holding: Declare properly to avoid catastrophic Black Money Act penalties

- Harvesting: India doesn’t allow loss harvesting; focus on minimizing taxable events

Tax Planning Opportunities (US)

The US system offers more flexibility:

- Long-term holdings: Prioritize holding > 1 year to access lower capital gains rates

- Loss harvesting: Offset gains with realized losses; consider portfolio balancing

- Income timing: If possible, harvest gains in years of lower income

- Charitable giving: Donate appreciated crypto to reduce taxable income (advanced strategy)

- Defi caution: Be careful with yield farming and liquidity pool strategies; document carefully

Compliance Essentials – What You Must Do

If You’re in India

- Maintain detailed records for 7 years:

- Transaction date, asset type, cost, sale price (in INR)

- Exchange used and exchange rates

- TDS deducted at source

- Report in Schedule VDA:

- All domestic and foreign crypto activity

- Even if held but not sold

- Declare foreign exchanges in Schedule FA:

- Complete asset value, location, income generated

- Failure here carries 90% penalty under Black Money Act

- File ITR timely:

- Form ITR-2 for most investors

- Form ITR-3 for business/professional traders

- Understand TDS:

- Track where 1% was deducted

- Claim in return for adjustment/refund

If You’re in the US

- Gather exchange records:

- All transactions with dates and prices

- Exchanges will send Forms 1099-K or 1099-B

- Calculate basis and gains:

- Use consistent cost basis method (FIFO, LIFO, or specific ID common for crypto)

- Maintain records showing which coins were sold

- Report on Form 8949:

- List each transaction separately (or aggregated if many)

- Calculate short vs. long-term

- File Schedule D:

- Summary of all capital gains/losses

- Net amount goes to Form 1040

- Foreign exchange reporting:

- FinCEN Form 114 (FBAR) if foreign accounts > $10,000

- Form 8938 if needed

- Do not underestimate these—penalties are severe

- Crypto-specific forms:

- Many CPAs now request detailed crypto transaction schedules

- Some platforms offer tax reports; review for accuracy

Future Outlook – What’s Changing in 2026?

India’s Potential Evolution

The Indian government has resisted pressure to lower crypto tax rates or allow loss offsets. However:

- Industry groups like Bharat Web3 Association continue lobbying for change

- Higher tax rates are pushing traders to offshore platforms

- There’s periodic discussion of “tiered” taxation based on holding period

Don’t expect major reforms in 2026, but don’t rule out clarifications on DeFi and staking definitively.

US Regulatory Developments

The Biden administration and Congress have shown interest in:

- Clarifying DeFi taxation (potentially tightening rules)

- Potentially lowering capital gains rates for middle income (unlikely in 2026)

- Enhanced reporting requirements (Form 1099-K thresholds have been unstable)

Key unknowns include whether the IRS will issue clearer guidance on wash sales, staking, and airdrops.

Global Harmonization?

As OECD efforts on taxing the digital economy evolve, some convergence may occur:

- India might face international pressure to allow loss offsets

- The US might face pressure to provide clearer rules on “property” classification

However, full harmonization remains years away.

Expert Guidance and Compliance Tools

When to Hire Professionals

Hire a crypto tax expert if:

- You trade actively (>50 transactions annually)

- You hold coins across multiple exchanges

- You engage in DeFi, staking, or yield farming

- You cross borders (US/India or other jurisdictions)

- You’re unsure about basis calculations or reporting

In India: Look for Chartered Accountants familiar with Schedule VDA and Section 115BBH In the US: Look for CPAs or tax attorneys with Form 8949 / Schedule D expertise

Recommended Tools

For transaction tracking:

- CoinTracker, Koinly, or CryptoTaxAudit (supports India and US)

- Manual spreadsheets (tedious but functional)

For gain/loss calculation:

- Excel templates specific to Indian or US rules

- Professional crypto accounting software

For compliance documents:

- Keep exchange transaction history (downloadable CSV)

- Maintain wallet transaction logs

- Save exchange fee statements

FAQs

u003cstrongu003eIf I’m an Indian citizen living in the US, which country’s tax system applies?u003c/strongu003e

You must comply with both. As an Indian citizen, you’re likely still subject to Indian tax on Indian-source income (including crypto held on Indian exchanges). Meanwhile, if you’re a US resident, the US requires taxation of worldwide income. File both returns and claim foreign tax credits where applicable.

u003cstrongu003eDoes holding crypto long-term reduce taxes in India?u003c/strongu003e

No. India’s 30% flat tax applies regardless of holding period. There’s no incentive for long-term holding like in the US.

u003cstrongu003eCan I claim trading fees as deductions in India?u003c/strongu003e

No. Only the purchase price is deductible. Exchange fees, gas fees, and brokerage are ignored by the system.

u003cstrongu003eWhat if I made losses in crypto trading in India can I adjust next year?u003c/strongu003e

No. Only the purchase price is deductible. Exchange fees, gas fees, and brokerage are ignored by the system.

u003cstrongu003eWhat if I made losses in crypto trading in India can I adjust next year?u003c/strongu003e

No. Losses cannot be carried forward. They disappear on March 31.

u003cstrongu003eIs staking income taxed differently than trading income in India?u003c/strongu003e

Yes. Staking rewards are taxed as ordinary income under Section 56(2)(x) at your slab rate initially. Later appreciation is taxed at 30%. In the US, staking is also ordinary income initially, then capital gains on appreciation.

u003cstrongu003eHow does the US tax an airdrop?u003c/strongu003e

As ordinary income at fair market value on the date received. If you later sell it, gains above that FMV are capital gains (short or long-term).

u003cstrongu003eAre there any crypto transactions that aren’t taxable in the US?u003c/strongu003e

Generally, no. Even transferring between your own wallets isn’t taxable, but executing a trade or accepting rewards generates a taxable event.

u003cstrongu003eWhat happens if I don’t report crypto on my tax return?u003c/strongu003e

In India, penalties range from 50% to 200% of unpaid tax, plus potential Black Money Act scrutiny. In the US, penalties include failure-to-file, failure-to-pay, and accuracy-related penalties (20% of underpayment); criminal prosecution is possible for egregious cases.

Conclusion: Navigating the 2026 Crypto Tax Landscape

The crypto tax environment in 2026 is more settled, more enforced, and more complex than ever. India has locked in a strict, flat-rate system that prioritizes simplicity over equity. The US has maintained a complex but flexible system that rewards long-term investing and allows tax optimization.

- For Indian investors: Compliance is non-negotiable. Foreign asset declaration is critical. Loss harvesting isn’t an option, so focus on minimizing taxable events and understanding the 1% TDS mechanism.

- For US investors: The holding period matters enormously. Long-term gains are dramatically better than short-term gains. Loss harvesting is your primary optimization tool.

- For cross-border players: Your situation is complicated, but not impossible to manage. Proper documentation, timely filing, and potentially professional guidance make all the difference.

The bottom line: understand your jurisdiction’s rules, maintain meticulous records, and plan accordingly. The tax systems may differ philosophically, but both are increasingly stringent in enforcement.

Final Disclaimer

This blog post is for informational purposes only and is not professional financial, tax, or legal advice. Crypto tax laws are complex and subject to change. Always consult qualified professionals a Chartered Accountant in India or a CPA in the US—before making trading decisions or filing tax returns based on crypto activity.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.