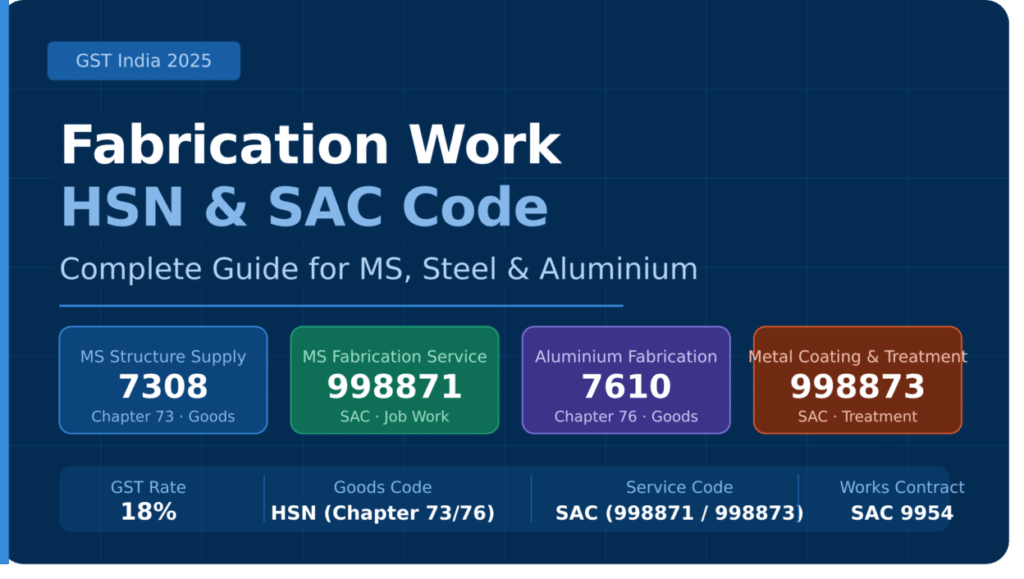

Fabrication Work HSN Code: The Complete 2026 Guide for MS, Steel & Metal Fabrication

If you’ve ever raised a GST invoice for fabrication work and stared at the HSN/SAC field wondering what number goes there, you’re not alone. Contractors, fabricators, and procurement teams get this wrong constantly, and a wrong code on your invoice can mean a mismatch notice from the GST department, a blocked ITC claim, or worse, a demand with penalty. Here’s the core problem: fabrication sits on an awkward line. Sometimes it’s a supply of goods (you’re delivering a fabricated MS structure). Sometimes it’s a supply of services (you’re working on the client’s material at their site). GST treats these two scenarios completely differently, with different HSN codes, different SAC codes, and different tax rates. In this guide, you’ll find the exact HSN and SAC codes for MS fabrication work, steel fabrication, aluminium fabrication, and job work on metal structures. You’ll also understand when to use a goods code vs a service code, what 998873 means, and how to pick the right GST rate for your invoice — without calling a CA every time. I’ve spent years working with fabrication contractors, structural steel suppliers, and industrial clients navigating GST compliance. The confusion in this space is real, and most of what’s written online is either too generic or just plain outdated. What Is an HSN Code? HSN stands for Harmonised System of Nomenclature. It’s a 6-to-8-digit international product classification system that India adopted under GST. Every physical good sold in India needs one. The CBIC (Central Board of Indirect Taxes and Customs) maps GST rates to these codes. An HSN code is a standardised 6–8 digit number that classifies physical goods for GST purposes. It works by grouping products into chapters (2 digits), headings (4 digits), and sub-headings (6–8 digits) based on material composition and product type. Most commonly used on B2B invoices where the buyer claims input tax credit. SAC stands for Services Accounting Code — the equivalent classification for services under GST. Where HSN covers goods, SAC covers what you do. Fabrication work is complicated because the same job can be either. A structural MS fabricator who purchases raw MS angle, fabricates trusses in his workshop, and delivers the finished structure to the client is supplying goods. A job worker who goes to the client’s site, uses the client’s MS material, and does cutting, welding, and assembly is supplying a service. The GST rule is clear: if you supply a fabricated product, use an HSN code. If you supply fabrication as a service (including job work), use a SAC code. HSN Codes for MS and Steel Fabrication Products (Goods) When you manufacture and supply fabricated goods made of mild steel or structural steel, Chapter 73 of the HSN schedule applies. Chapter 73 covers “Articles of Iron or Steel.” The primary HSN codes for MS and steel fabrication products fall under Chapter 73 (Iron and Steel Articles). The most relevant heading is 7308, which covers structures and parts of structures made of iron or steel — including bridges, towers, columns, beams, frames, doors, and similar fabricated items. GST rate on most Chapter 73 fabricated structural items is 18%. Here are the most-used Chapter 73 HSN codes for fabricated MS and steel goods: HSN Code Description GST Rate 7308 Structures and parts of structures of iron or steel (towers, trusses, columns, frames, bridges, shuttering) 18% 7308 10 Bridges and bridge sections 18% 7308 20 Towers and lattice masts 18% 7308 30 Doors, windows, and frames 18% 7308 40 Equipment for scaffolding, shuttering, and prop systems 18% 7308 90 Other structures (sheds, columns, beams, platforms) 18% 7326 Other articles of iron or steel 18% 7214 Bars and rods of iron or non-alloy steel 18% For MS fabrication work where you supply a finished product — a fabricated shed, staircase, railing, structural column, or mezzanine floor — HSN 7308 90 is the most commonly applicable code. For MS pipes and pipe fittings fabricated and supplied, look at HSN 7304 (seamless tubes/pipes) or 7306 (welded tubes/pipes). What “MS Structure” Means for GST Classification MS (Mild Steel) structures include everything from factory sheds and storage platforms to industrial frames and staircase structures. All of these, when fabricated and supplied as finished goods, fall under HSN 7308. The GST rate of 18% applies across the board. There is no concessional rate for MS structural work when supplied as goods. SAC Code for Fabrication Work as a Service (998873 Explained) Here’s where most people get confused. If you’re not supplying fabricated goods but instead doing fabrication on someone else’s material, you’re providing a service. GST classifies this as “Manufacturing Services on Physical Inputs Owned by Others” — what used to be called job work. SAC code 998873 covers “treatment and coating of metals and machining services,” which under the broader GST framework for manufacturing services covers metal fabrication work done as a service on materials supplied by the client. The applicable GST rate is 18%. This code applies when a fabricator works on material owned by the principal manufacturer or client. The full SAC hierarchy looks like this: SAC Code Description GST Rate 9988 Manufacturing services on physical inputs owned by others 18% 998871 Structural metal product manufacturing services 18% 998872 Fabricated metal product manufacturing services 18% 998873 Treatment and coating of metals and machining services 18% 998874 Cutlery, hand tool, and general hardware manufacturing services 18% SAC 998871 is the most directly applicable code for structural MS fabrication services — making it the correct choice for most contractors doing job work on iron/steel structures. SAC 998873 specifically applies when the work involves surface treatment, galvanizing, powder coating, or machining as part of the fabrication process. When to Use 998871 vs 998873 Use 998871 when your scope of work is: cutting, drilling, welding, assembling, and erecting steel structures from material supplied by the client. Use 998873 when your work is primarily: blasting, priming, painting, galvanizing, powder coating, heat treatment, or precision machining of metal components. Many fabrication contracts involve both. In that case, the principal supply