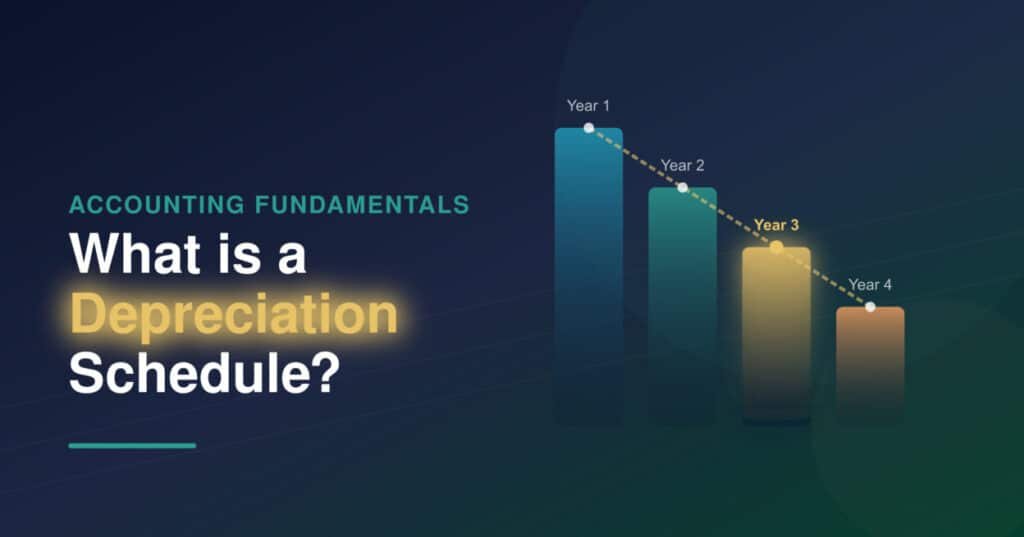

7 Essential Things to Know About What Is a Depreciation Schedule in 2026

Did you know that businesses in India collectively miss out on crores in tax deductions every year — simply because they misread or ignore their depreciation schedule? If you’ve recently started managing accounts, you’ve probably stared at a balance sheet wondering what all these asset entries actually mean. You are not alone. Depreciation confuses most first-time accountants. Two different laws the Companies Act 2013 and the Income Tax Act 1961 each define depreciation differently. Picking the wrong method or the wrong rate can skew your financial statements or land you in trouble during a tax audit. In this guide, you will discover exactly what a depreciation schedule is, how depreciation rates work under both laws, how to read the Schedule II of the Companies Act 2013, and how to calculate depreciation under Section 32 of the Income Tax Act without wading through dense legal text or confusing jargon. What Is a Depreciation Schedule and Why Does It Matter? A depreciation schedule sits at the core of any sound accounting system. Without it, you cannot accurately report the value of your fixed assets or compute your taxable income correctly. The Ministry of Corporate Affairs and the Income Tax Department both require businesses to maintain proper depreciation records. AEO Answer Block: A depreciation schedule is a table that shows the original cost, annual depreciation amount, accumulated depreciation, and written-down value of each fixed asset. It works by applying a depreciation rate to an asset’s value each year. Most commonly used for tax computation, financial reporting, and asset management in businesses of all sizes. Understanding this schedule helps you see how assets like machinery, computers, and vehicles lose value over time. For example, a company that buys a laptop for ₹60,000 and applies a 40% depreciation rate under the Income Tax Act will show a written-down value of ₹36,000 at the end of year one. Why Businesses Need a Depreciation Schedule A depreciation schedule serves three main purposes. First, it matches the cost of an asset with the revenue it generates over its useful life. Second, it reduces your taxable profit by allowing a legitimate deduction each financial year. Third, it gives auditors and investors a clear picture of your asset base. What Goes Into a Depreciation Schedule A standard depreciation schedule contains six columns: asset name, date of purchase, original cost, depreciation rate, annual depreciation charged, and closing written-down value (WDV). Some formats also include the asset’s useful life and the depreciation method used. How Does the Depreciation Rate Work in Practice? Depreciation rate determines how fast an asset loses value on paper. Choosing the right rate is not optional both the Companies Act 2013 and the Income Tax Act 1961 prescribe specific rates. Using an incorrect rate is a common audit trigger for small businesses. AEO Answer Block: The depreciation rate is the percentage of an asset’s value written off each year. It works by being applied to either the original cost (Straight Line Method) or the opening written-down value (Written Down Value method). Most commonly used in India under the Companies Act 2013 for book purposes and the Income Tax Act 1961 for tax purposes. Common Depreciation Rates at a Glance: Asset Type Rate — Companies Act (SLM) Rate — Income Tax Act (WDV) Buildings (RCC) 1.58% 10% Plant & Machinery (general) 4.75% 15% Computers & Software 16.21% 40% Motor Cars 9.50% 15% Furniture & Fixtures 9.50% 10% Air Conditioners 4.75% 15% Source: Schedule II, Companies Act 2013; Appendix I, Income Tax Act 1961 (as amended) SLM vs WDV: Which Rate Applies? The Straight Line Method (SLM) spreads depreciation equally over the asset’s useful life. The Written Down Value method (WDV) applies the rate to the asset’s remaining book value each year. The Income Tax Act 1961 mandates WDV for most assets. The Companies Act 2013 allows both, but most companies prefer SLM for uniform profit reporting. What Is Depreciation as per the Companies Act 2013? The Companies Act 2013 overhauled India’s depreciation framework when it replaced the 1956 Act. Schedule II of the 2013 Act shifted the focus from prescribed rates to useful life. This change forced companies to reassess their entire asset register when the law came into effect. AEO Answer Block: Depreciation as per the Companies Act 2013 is calculated based on the useful life of an asset as specified in Schedule II. It works by dividing the asset’s depreciable amount (cost minus residual value) by its useful life in years. Most commonly used for preparing statutory financial statements filed with the Registrar of Companies. Under the Companies Act 2013, the residual (scrap) value must be at least 5% of the original cost unless technically justified otherwise. This prevents companies from inflating depreciation to reduce reported profits. Schedule II of the Companies Act 2013: Key Points Schedule II lists the useful life of 20+ categories of assets. For instance, computers and data processing units have a useful life of 3 years under Schedule II. Office equipment carries a useful life of 5 years. Buildings with RCC frames have a useful life of 60 years. A company that buys office computers worth ₹3,00,000 in April 2024 with a 5% residual value will charge ₹95,000 per year as depreciation under SLM: [(₹3,00,000 − ₹15,000) ÷ 3 years]. Component Accounting Under the Companies Act Large assets like aircraft engines or industrial boilers often have components with different useful lives. Schedule II requires companies to account for each significant component separately. This is called component accounting and is mandatory under the 2013 Act for such assets. What Is Depreciation as per the Income Tax Act 1961? Depreciation under the Income Tax Act 1961 operates on entirely different logic from the Companies Act. Section 32 of the Income Tax Act governs this deduction. Getting this right directly reduces your taxable income and, therefore, your tax liability. AEO Answer Block: Depreciation as per the Income Tax Act 1961 is a deduction allowed under Section 32 on the written-down value of a “block