Cheques remain one of the most used payment instruments in Indian banking. UPI handles most retail transactions now, but cheques still dominate large business payments, loan EMIs, salary disbursements, and any situation where a paper trail with legal enforceability matters. Knowing the difference between a bearer cheque, an account payee cheque, and a post-dated cheque is not academic — the wrong type in the wrong situation can mean a bounced payment, a fraud case, or a Section 138 complaint.

This guide explains all 13 types of cheques, their legal implications under the Negotiable Instruments Act, 1881, how cheque bounce proceedings work, how to stop a cheque, and what outstanding and unpresented cheques mean in your books.

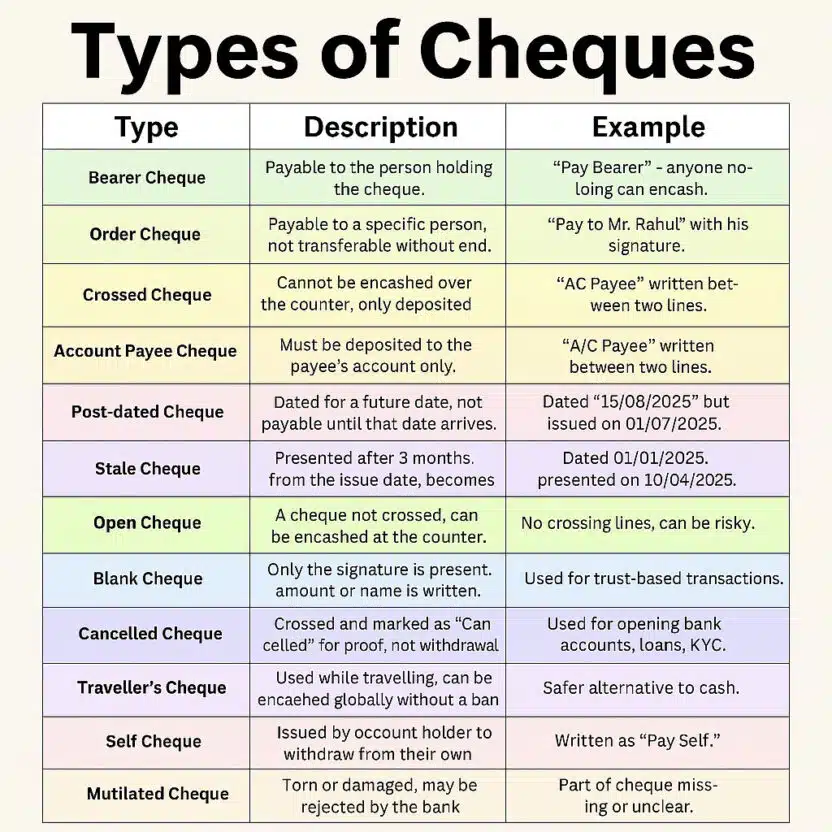

What Are the 13 Types of Cheques?

The 13 types of cheques used in India are:

- Bearer Cheque

- Order Cheque

- Crossed Cheque

- Account Payee Cheque

- Post-Dated Cheque (PDC)

- Stale Cheque

- Open Cheque

- Blank Cheque

- Cancelled Cheque

- Traveller’s Cheque

- Self Cheque

- Mutilated Cheque

- Gift Cheque

Each type has a specific purpose, risk profile, and legal standing. The sections below cover each one in detail.

What Is a Cheque? (Definition and Legal Basis)

A cheque is a written, unconditional order from an account holder (the drawer) to their bank (the drawee) to pay a specified sum to a named person or bearer (the payee) on demand.

In India, cheques are governed by Section 6 of the Negotiable Instruments Act, 1881. A cheque is legally defined as a bill of exchange drawn on a specified banker and payable on demand.

Three parties involved in every cheque:

| Party | Role |

|---|---|

| Drawer | Account holder who writes and signs the cheque |

| Drawee | The bank where the drawer holds the account |

| Payee | The person or entity receiving the payment |

A valid cheque must contain:

- Drawer’s signature

- Payee’s name (or “bearer”)

- Amount in figures and words (both must match)

- Date

- Bank name and branch (pre-printed)

- MICR code (pre-printed)

Any mismatch between figures and words, an absent signature, or a date outside the valid 3-month window will cause the bank to return the cheque.

13 Types of Cheques Explained in Detail

1. Bearer Cheque

A bearer cheque is payable to whoever presents it at the bank counter. The bank does not verify identity. Any person holding the cheque can encash it.

How to identify: The payee line reads “Pay Bearer” or names a person followed by the words “or bearer.”

Used for: Petty cash withdrawals, quick informal payments.

Risk: A lost or stolen bearer cheque gives the finder immediate access to the full amount. Banks advise against bearer cheques for amounts above routine petty cash. RBI has progressively tightened rules around bearer cheques to reduce fraud.

Legal note: If a bearer cheque bounces, the drawer faces Section 138 liability just as they would with any other cheque type.

2. Order Cheque

An order cheque names a specific payee. The bank pays only that person after verifying identity. The payee can transfer an order cheque to a third party through endorsement (signing the back), but every transfer is documented.

Example: “Pay Mr. Suresh Mehta or order.”

Used for: Standard business payments, vendor invoices, supplier settlements.

Key distinction: Bearer cheques carry the word “bearer.” Order cheques carry a name or the word “order.” When a cheque names someone and also says “bearer,” the bearer instruction applies and the cheque becomes a bearer instrument.

3. Crossed Cheque

A crossed cheque carries two parallel horizontal lines drawn across the top-left corner. These lines mean the cheque cannot be encashed at the counter — the amount must be deposited into a bank account.

Two types of crossing:

| Crossing Type | Description |

|---|---|

| General Crossing | Two plain parallel lines, sometimes with “& Co.” between them |

| Special Crossing | A specific bank name written between the lines; payment restricted to that bank only |

How to add a crossing: Draw two parallel lines on any uncrossed cheque. Once drawn, a crossing cannot be removed. Adding “Not Negotiable” between the lines means the cheque loses its negotiable character — the receiver gets no better title than the transferor.

Used for: Any payment requiring a paper trail. The crossing ensures money moves account-to-account, creating a verifiable record.

4. Account Payee Cheque

An account payee cheque adds the words “A/C Payee” or “Account Payee Only” between the crossing lines. The amount can only enter the named payee’s own bank account. No third-party encashment. No endorsement to another person.

Example: Two crossed lines with “A/C Payee Only” written between them.

Used for: Salary payments, income tax refunds, mutual fund redemptions, government disbursements, formal business settlements.

Why this is the safest cheque type: Only the named person’s bank account can receive the funds. Even if the cheque is stolen, the thief cannot deposit it in their own account or encash it over the counter. Banks process account payee cheques through clearing, creating a full audit trail.

5. Post-Dated Cheque (PDC)

A post-dated cheque carries a future date. The bank will not process it before that date. The issuer hands it over today and the payment executes on the future date.

Example: A cheque issued on 1 June 2025 but dated 1 September 2025 covers a quarterly rent payment due in September.

Used for: Loan EMIs, rent agreements, hire purchase, advance payments, supplier credit arrangements.

Section 138 liability on PDCs: If your account lacks funds on the cheque date, the payee can file a cheque bounce case. The relevant date is the date written on the cheque, not the date you handed it over.

Security cheque vs. PDC: A security cheque is a specific PDC given as collateral against a loan. If the borrower repays as agreed, the lender returns the cheque uncashed. If the borrower defaults, the lender deposits the cheque. Courts have repeatedly held that dishonour of a security cheque can attract Section 138 liability — see the section on security cheques below for detailed case law context.

6. Stale Cheque

A cheque becomes stale when the payee presents it more than 3 months after the date written on it. RBI mandated this 3-month validity period effective April 2012. Before that, cheques were valid for 6 months.

Example: A cheque dated 1 January 2025, presented on 5 April 2025, is stale. The bank returns it marked “stale cheque” or “out of date.”

What to do if you receive a stale cheque: Contact the drawer and request a reissue with a current date.

Accounting note: Do not confuse stale cheques with outstanding cheques. An outstanding cheque is within its validity window but not yet presented. A stale cheque has expired.

7. Open Cheque

An open cheque (also called an uncrossed cheque) carries no parallel lines. The payee can walk to the bank counter and receive cash directly without depositing it into an account.

Risk: Open cheques are the second most fraud-prone type after bearer cheques. Loss or theft exposes the full amount.

Conversion: Adding two parallel lines to an open cheque converts it into a crossed cheque. This action is irreversible.

8. Blank Cheque

A blank cheque carries only the drawer’s signature. The payee name, amount, and date are left unfilled.

Used for: Trusted relationships — some business partners, employers giving employees signing authority for emergency expenses. High-trust environments only.

Legal risk — blank cheque misuse: Courts in India handle a significant volume of blank cheque with signature misuse cases. The core problem: because the signature is genuine, the drawer bears the burden of proving that the amount or payee name filled in was unauthorized. Evidence courts accept includes bank statements (showing the actual loan disbursed vs. the inflated cheque amount), written correspondence about the original purpose, and witness testimony.

Practical advice: Never sign a blank cheque for someone without a written record of the purpose and maximum authorized amount. That record is your only protection if misuse occurs.

9. Cancelled Cheque

A cancelled cheque has the word “CANCELLED” written in large letters across its face, along with two parallel lines. It cannot be used for payment.

Used for:

- KYC verification

- Bank account linking for mutual fund investments

- Salary account verification by employers

- Loan applications

- ECS (Electronic Clearing Service) and NACH mandate registration

- Provident fund withdrawals

When a company’s payroll department asks for a cancelled cheque, they want to confirm your account number, IFSC code, and bank branch. No money changes hands.

Cancelled cheque vs. stopped cheque: A cancelled cheque was never issued for a transaction. A stopped cheque was issued, but the drawer instructed the bank to refuse payment before the payee presented it.

10. Traveller’s Cheque

A traveller’s cheque is a pre-printed, fixed-denomination instrument issued by banks for international travel. The buyer signs it once at purchase and countersigns it at the point of encashment. Banks and authorised dealers accept them without requiring a local account.

Benefit: Safer than carrying foreign currency cash. If lost or stolen, the issuing institution replaces them after identity verification.

Current status: Most travellers now use international debit cards or forex prepaid cards. Traveller’s cheques are still issued by some Indian public sector banks and remain accepted in many countries, but their use has sharply declined.

11. Self Cheque

A self cheque is drawn by an account holder to withdraw money from their own account. The payee field carries the word “Self” instead of another person’s name.

Example: Writing “Pay Self” or “Pay to Self” on the cheque.

Used for: Large cash withdrawals from a home branch when ATM limits are insufficient.

Bank procedure: The bank verifies the drawer’s signature and identity before paying cash. Only the account holder can encash a self cheque.

12. Mutilated Cheque

A mutilated cheque is torn, damaged, or worn to the point that critical details are unclear. Banks can reject mutilated cheques if the signature, amount, date, or MICR code is missing or unreadable.

Common causes: Accidental tearing, water damage, insect damage in cheque books, rough handling during postal transit.

Resolution: If only corners are torn but all details remain clear, the bank manager may accept it with the drawer’s written confirmation. For significant damage, request a fresh cheque from the issuer.

13. Gift Cheque

A gift cheque is issued by a bank to customers for gifting purposes on occasions like weddings, birthdays, and anniversaries. It comes in fixed denominations and carries a decorative design.

Issuing process: The buyer pays the bank upfront. The bank issues the instrument. The recipient deposits it or encashes it at the issuing bank.

Key difference from personal cheques: A gift cheque comes from the bank’s own account, not the buyer’s personal account. The transaction settles when the buyer pays the bank, not when the recipient presents the cheque.

13 Types of Cheques: Complete Comparison Table

| Type | Counter Encashment | Payee Restriction | Transfer by Endorsement | Primary Use |

|---|---|---|---|---|

| Bearer Cheque | Yes | Anyone holding it | Yes, automatically | Petty cash |

| Order Cheque | With ID verification | Named person only | Yes, with endorsement | Standard payments |

| Crossed Cheque | No | Must deposit in bank | Depends on type | Traceable payments |

| Account Payee Cheque | No | Named payee’s account only | No | Salaries, refunds |

| Post-Dated Cheque | No (before cheque date) | Named payee | No | EMIs, rent |

| Stale Cheque | No (expired) | — | — | Needs reissue |

| Open Cheque | Yes | No restriction | Yes | Cash payments |

| Blank Cheque | Depends on filled details | Whoever fills the name | Depends | High-trust situations |

| Cancelled Cheque | No | — | — | KYC, account verification |

| Traveller’s Cheque | At banks/agents | Countersignature required | No | International travel |

| Self Cheque | Yes (own branch) | Account holder only | No | Personal withdrawal |

| Mutilated Cheque | At manager’s discretion | — | — | May need replacement |

| Gift Cheque | At issuing bank | Named recipient | No | Celebrations |

Cheque Bounce: Section 138 NI Act, Procedure, and Legal Remedy

What Is Cheque Bounce?

A cheque bounces when the bank returns it unpaid. The most common reason is insufficient funds. Other reasons include:

- Signature mismatch

- Stale date (more than 3 months old)

- Overwriting without the drawer’s countersignature

- Post-dated cheque presented before the cheque date

- Stop payment instruction from the drawer

- Account closed or frozen

The bank issues a cheque return memo explaining the reason. This memo is the foundation of any Section 138 case.

Section 138 of the Negotiable Instruments Act

Section 138 makes cheque dishonour a criminal offence when:

- The cheque was issued for a legally enforceable debt or liability

- The drawer’s account lacked sufficient funds (or the account was closed)

- The cheque was presented within its 3-month validity period

Punishment under Section 138: Imprisonment up to 2 years, or a fine up to twice the cheque amount, or both.

Important: Section 138 does not apply if the cheque was given as a gift, donation, or for any purpose that is not a legally enforceable debt.

Cheque Bounce Case Procedure: Step-by-Step

Step 1 — Receive the bank’s return memo. Keep the original. This document proves the cheque was presented and returned.

Step 2 — Send a legal notice within 30 days. Draft a written demand notice to the drawer asking for payment within 15 days. Send it by registered post or speed post. The 15-day clock starts from the date the drawer receives it, not the date you send it.

Step 3 — Wait 15 days. If the drawer pays during this period, the matter ends. If they pay after you file the case, it can still result in compounding (settlement) of the offence.

Step 4 — File the complaint. Within 30 days of the 15-day period expiring, file a complaint under Section 138 in the Magistrate’s court with jurisdiction over the location of the bank branch on which the cheque was drawn.

Step 5 — Attach documents: Original bounced cheque, bank’s return memo, copy of legal notice, proof of dispatch (registered post receipt), proof of delivery or tracking record.

Step 6 — Pay court fees. Court fees for Section 138 complaints are nominal in most states — typically below ₹500 for the initial complaint. Advocate fees vary; cheque bounce lawyers in Delhi typically charge ₹5,000–₹25,000 depending on amount and complexity.

Cheque Bounce Jurisdiction

The complainant files the case in the court within whose jurisdiction the drawer’s bank branch is located. The 2015 amendment to the NI Act settled this — earlier there was confusion about whether the case belonged in the payee’s city or the drawer’s city.

Practical implication: If you are in Mumbai and the drawer’s account is in Chennai, you file in Chennai.

Legal Notice Format for Cheque Bounce

A legal notice for cheque bounce must contain:

- Cheque number, date, amount

- Name of the drawer’s bank

- Date of dishonour

- Reason stated in the bank’s return memo

- Demand for payment of the cheque amount within 15 days

- Statement that failure to pay will result in legal action under Section 138

The notice must be sent by registered post. Retain the postal receipt and delivery acknowledgment. These are mandatory evidence in court.

A sample legal notice for cheque bounce (PDF or Word format) is available on most legal document platforms and bar association websites. Download and customise with specific cheque details rather than drafting from scratch.

Cheque Bounce SMS/Message Format to Debtor

Before issuing the formal legal notice, many creditors send an informal alert to the debtor:

“Dear [Name], your cheque No. [XXXX] dated [DD/MM/YYYY] for ₹[Amount] drawn on [Bank Name] was returned unpaid due to [reason as per bank memo]. Please arrange full payment within 15 days to avoid legal action under Section 138 NI Act.”

This message alone does not constitute the legal demand notice under Section 138. The formal registered post notice is still mandatory.

Security Cheque and Section 138: Legal Position

A security cheque is a post-dated cheque given as collateral to secure repayment of a loan or obligation. If the borrower repays, the lender returns the cheque. If the borrower defaults, the lender deposits it.

Can a Security Cheque Attract Section 138?

Yes. The Supreme Court has held in multiple judgements that dishonour of a cheque issued as security can attract Section 138 liability. The landmark position established through cases like M.S. Narayana Menon v. State of Kerala and later decisions is that the nature of the debt — not the label “security cheque” — determines liability.

Key principle: If the cheque was issued for a legally enforceable debt and the account lacked funds when the cheque was presented, Section 138 applies regardless of whether the cheque was labelled a security instrument.

Defence available to the drawer: The drawer can prove the cheque was not issued for a legally enforceable debt, or that the debt has already been repaid, or that the cheque was presented in bad faith (e.g., before the borrower defaulted).

For the most current position on security cheque case law, search for “latest Supreme Court judgement on security cheque 2024 2025” — the law has evolved through several High Court and Supreme Court decisions.

How to Stop Payment of a Cheque

When Stop Payment Is Justified

Stop payment is appropriate when: goods or services were not delivered as agreed, you discover the payee committed fraud, there was an error in the cheque amount, or the relationship that prompted the cheque has broken down before presentation.

Stop payment must reach the bank before the cheque is presented. Once the bank processes the payment, stop payment has no effect.

Cheque Stop Payment Letter Format

A formal stop payment letter to your bank should contain:

- Your full name and account number

- Cheque number to be stopped

- Cheque date and amount

- Payee’s name as written on the cheque

- Reason for stop payment request

- Your signature and date

Stop payment letter format in Word (sample text):

“I/We, [Name], holder of Savings/Current Account No. [XXXX] at [Bank Name, Branch], hereby request you to stop payment of Cheque No. [XXXX] dated [DD/MM/YYYY] for ₹[Amount] drawn in favour of [Payee Name]. The reason for this request is [reason]. Please acknowledge receipt of this instruction.”

Most banks now accept stop payment instructions through net banking, mobile banking, or phone banking. A written letter creates the strongest paper trail.

Bank charges: Stop payment fees typically range from ₹100 to ₹500 per cheque, depending on the bank.

Legal Risk of Stopping Payment Without Cause

Stopping a cheque to delay or avoid a legitimate debt does not eliminate the underlying obligation. The payee can file a civil suit for recovery of the amount plus damages. Stop payment is a banking right, not a debt-avoidance tool.

Blank Cheque Misuse: Cases and Legal Protection

How Misuse Happens

The most common pattern: a borrower signs a blank cheque as “security” for a loan. The lender fills in an amount higher than the actual loan when the borrower defaults. A Section 138 case follows. The borrower argues the amount was unauthorised. The lender argues the cheque was freely signed.

How Courts Handle It

Courts place the initial burden on the complainant to prove the debt existed and the cheque was issued for that debt. Once established, the burden shifts to the accused to prove the cheque was not issued for a legally enforceable debt or that the amount was falsified.

Evidence that has successfully defended blank cheque misuse cases:

- Bank statements showing actual disbursed loan amount vs. inflated cheque amount

- Correspondence (emails, WhatsApp messages, letters) defining the original purpose

- Witness testimony from people who were present when the cheque was handed over

- Receipts or agreements showing actual transaction amounts

Prevention: Write a brief note on paper before handing over any signed cheque — even to a known party — stating: the date, the purpose, the maximum authorised amount, and both parties’ names. Both parties sign it. That document is your defence.

Outstanding and Unpresented Cheques in Accounting

Outstanding Cheque Meaning

An outstanding cheque is a cheque the business has issued and recorded in its books, but which the payee has not yet presented to the bank for payment. The company’s books show the payment as made; the bank’s records do not yet reflect the debit.

In bank reconciliation statements: Outstanding cheques appear as a deduction from the bank balance to arrive at the book balance. The sequence is:

Bank balance as per statement → Add: deposits in transit → Less: outstanding cheques = Balance as per books

Unpresented Cheques Meaning

Unpresented cheques and outstanding cheques refer to the same thing. Some accountants and exam syllabi use “unpresented” to describe cheques issued by the entity that have not yet cleared the bank. Both terms describe cheques in transit between issuance and bank debit.

Old unpresented cheques: A cheque remaining unpresented for more than 3 months becomes stale. At that point, write back the liability in your books (debit bank, credit the party) after confirming with the payee whether they still hold the cheque or need a reissue.

How to Show Cheque Number While Reconciling Bank Accounts in Tally

In Tally Prime:

- Go to Gateway of Tally → Accounting Vouchers → Payment and ensure you enter the cheque number in the Narration or Cheque Number field when recording each payment.

- For bank reconciliation, go to Gateway of Tally → Banking → Bank Reconciliation.

- Select the bank ledger. The screen shows all unreconciled entries.

- Match each entry against your bank statement using the cheque number as the reference.

- Enter the bank date against each matched entry to mark it as reconciled.

Tally automatically filters by cheque number if you have used it consistently during data entry.

Cheque Return Entry in Tally

When a deposited cheque is returned by the bank unpaid:

- Debit: Party’s account (or Debtors account) — restores the receivable

- Credit: Bank account — reverses the deposit entry

- Debit: Bank charges account (for dishonour fee charged by bank)

- Credit: Bank account (for the bank’s dishonour charge)

This pair of entries restores the bank balance and re-opens the receivable from the party who gave you the bounced cheque.

Cheque Discounting

Cheque discounting is a short-term financing arrangement. A business holding a post-dated cheque sells it to a financier at a discount in exchange for immediate funds. The financier collects the full amount when the cheque matures.

Example:

You hold a customer’s account payee cheque for ₹1,00,000 dated 60 days ahead. A finance company pays you ₹95,000 today and collects ₹1,00,000 from your customer’s bank on the cheque date. The ₹5,000 is the discount (financing fee).

Cheque-based private finance in Chennai and other South Indian cities is an established informal credit mechanism. Traders and small businesses use post-dated cheques as collateral for working capital loans. The financier holds the cheques as security and charges a monthly rate on the disbursed amount — typically 2–4% per month in informal markets.

Regulatory note: Formal cheque discounting by NBFCs and banks is regulated. Informal cheque discounting by individuals or unregistered entities operates outside RBI oversight. Borrowers and lenders in informal arrangements accept legal risk if the cheque bounces.

Risk for the discounting firm: If the cheque drawer’s account lacks funds on the cheque date, the discounting firm can file under Section 138. Recovery through courts takes time, and legal costs reduce the return on the discount.

GST on Cheques and Cheque Books

GST on Cheque Book Issuance

Banks charge a fee for issuing cheque books. GST at 18% applies to this service charge. If your bank charges ₹50 for a cheque book of 20 leaves, you pay ₹59 including GST.

GST on Cheque Return Charges

When a bank returns a cheque unpaid, it charges the depositor a cheque return fee. GST at 18% applies to this charge. The cheque return memo from your bank will reflect the fee and GST separately.

GST on the Cheque Transaction Amount

The amount written on a cheque does not attract GST. GST applies to banking service fees only, not to the payment being made.

For the current applicable rates on specific banking charges, check your bank’s Most Important Terms and Conditions (MITC) document or consult the bank’s fee schedule. GST Council notifications occasionally revise rates on financial services.

Promissory Note vs Bill of Exchange vs Cheque

All three are negotiable instruments under the NI Act, 1881. They serve different purposes and involve different parties.

| Feature | Promissory Note | Bill of Exchange | Cheque |

|---|---|---|---|

| Parties | 2 (maker, payee) | 3 (drawer, drawee, payee) | 3 (drawer, bank, payee) |

| Drawee | No bank required | Any person or entity | Always a bank |

| Acceptance required | No | Yes, by the drawee | No |

| Payable on | Demand or future date | Demand or future date | Demand only |

| Validity period | No fixed limit | No fixed limit | 3 months |

| Section 138 applies | No | No | Yes |

Promissory note: A written promise by the maker to pay a specific sum to the payee. No bank involved. Used in loan agreements, inter-company lending.

Bill of exchange: A written order from the drawer directing the drawee to pay the payee. The drawee must “accept” the bill. Used in trade credit and international commerce.

Cheque: A bill of exchange drawn on a bank, payable on demand. No acceptance required. The bank pays immediately on presentation as long as the account has funds.

Cheque Book Requisition and Printing

Cheque Book Requisition Slip

A cheque book requisition slip is a form submitted to the bank when you need a new cheque book. Most banks allow online requests through net banking or mobile banking. For branch submission, the slip asks for your account number, last cheque leaf number, and number of leaves required.

Delivery time: 3–7 working days in most Indian banks.

PNB customer ID on cheque book: Your Punjab National Bank customer ID is printed on the cover page of your cheque book. It is separate from your account number and is used for PNB ONE (net banking) login credentials.

Cheque Printing Format

RBI prescribes the standard cheque layout under the Cheque Truncation System (CTS-2010) specifications. The critical fields are:

- Bank name and branch (pre-printed)

- Account number (pre-printed in MICR zone)

- Cheque number (pre-printed)

- MICR code at bottom (pre-printed)

- Date field

- Payee name line

- Amount in figures

- Amount in words

- Drawer’s signature space

Cheque Printing Format in Excel

Businesses that print their own cheques use Excel templates aligned to their cheque book’s physical dimensions. The standard CTS cheque measures 8 inches × 3.66 inches. The template maps each field to a cell positioned to match the printed cheque layout.

Free cheque printing software in Excel is available on accounting websites. After entering payee name, amount, and date, the template populates the cheque fields. Print on plain paper first and overlay your cheque leaf to verify alignment before printing on actual cheque stock.

Cheque Printing Printers and Machines

Standard laser printers cannot replicate MICR (Magnetic Ink Character Recognition) ink used in the numeric line at the bottom of cheques. Banks use MICR readers during clearing.

For businesses printing high volumes:

- MICR desktop printers: ₹15,000–₹30,000

- Commercial MICR printers: ₹50,000–₹80,000+

- Cheque scanning machines: ₹10,000–₹30,000 (for verification and archiving)

Joint Account Cheques

Joint accounts operate under one of two mandates:

- Either or Survivor: One signature suffices. Either account holder can issue and encash cheques independently.

- Jointly: Both signatures are required on every cheque.

A jointly mandated account with only one signature on a cheque will have that cheque returned by the bank. Confirm your mandate before issuing cheques from a joint account.

Authorization Letter to Collect a Cheque

If you cannot collect a cheque in person, authorise someone else through a written letter containing:

- Your full name and contact number

- The authorized person’s full name and ID details

- The cheque details (amount, date, issuer name)

- Your signature and date

Banks typically require the authorization letter alongside a photocopy of your identity document. For high-value cheques, individual banks may require the account holder’s physical presence. Confirm with your branch before sending a representative.

Property Tax Cheque: In Favour of Which Authority

The payee name on a property tax cheque must exactly match the legal name of your local municipal body. Common examples:

| City | Payee Name on Cheque |

|---|---|

| Surat | Surat Municipal Corporation |

| Mumbai | Brihanmumbai Municipal Corporation |

| Delhi | As per your zone: South/North/East MCD |

| Ahmedabad | Ahmedabad Municipal Corporation |

| Pune | Pune Municipal Corporation |

| Chennai | Greater Chennai Corporation |

Verify the exact name on your property tax demand notice before writing the cheque. A minor deviation in the payee name can cause the bank to reject the instrument.

Cheque Security Features (CTS-2010 Compliant Cheques)

RBI’s CTS-2010 specifications mandate security features on all cheques to prevent fraud:

- Watermark: “CTS-INDIA” watermark visible when held against light

- Void pantograph: The word “VOID” appears when the cheque is photocopied

- UV-reactive ink: Bank logo and certain fields glow under ultraviolet light

- Prohibitive colouring: Background colours designed to show tampering clearly

Cheque security stickers: Holographic or tamper-evident labels applied to high-value cheques. The label changes appearance when peeled or photocopied. Banks and large corporates use them for cheques above certain thresholds.

Cheque Register: Meaning and Use

A cheque register is an internal log of every cheque issued or received by a business. Each entry records: cheque number, date, payee or payer, amount, and current status (issued / presented / cleared / returned / stopped / stale).

Benefits:

- Simplifies monthly bank reconciliation

- Tracks outstanding and unpresented cheques

- Provides evidence in Section 138 disputes

- Detects gaps in cheque book series (potential theft)

In Tally and most accounting software, the cheque register populates automatically when you enter cheque numbers against bank payment and receipt vouchers.

Frequently Asked Questions (FAQs)

What is the validity period of a cheque in India?

A cheque is valid for 3 months from the date written on it. After 3 months, it becomes a stale cheque and banks will not accept it.

What happens when a cheque bounces?

The bank returns the cheque with a return memo stating the reason. The payee can send a legal notice to the drawer within 30 days demanding payment within 15 days. If the drawer does not pay, the payee can file a case under Section 138 of the NI Act.

Is a security cheque subject to Section 138?

Yes, the Supreme Court has held that dishonour of a cheque issued as security for a legally enforceable debt attracts Section 138 liability.

What is the difference between an outstanding cheque and an unpresented cheque?

They mean the same thing. Both refer to a cheque issued by the business but not yet presented to the bank for payment.

Can I stop payment on a cheque after issuing it?

Yes, you can instruct your bank to stop payment at any time before the cheque is presented. Most banks accept stop payment requests through net banking, mobile banking, or a branch visit and charge a nominal fee.

What is cheque discounting?

Cheque discounting is a financing arrangement where a business sells a post-dated cheque to a financier at a discount to receive immediate funds. The financier collects the full cheque amount on the maturity date.

What is the difference between a cheque and a promissory note?

A cheque is drawn on a bank, payable on demand, and Section 138 applies on dishonour. A promissory note is a promise to pay and does not involve a bank as the drawee. Section 138 does not apply to promissory notes.

What is a blank cheque and what are the misuse risks?

A blank cheque carries only the drawer’s signature with the amount, date, and payee left unfilled. Misuse occurs when someone fills in an unauthorized amount. The drawer bears the burden of proving misuse in court, making blank cheques legally risky.

Conclusion

Cheque literacy is practical risk management. Knowing which cheque type to use, how to handle a bounce, how to read an outstanding cheque in your bank reconciliation, and when a security cheque can become a criminal case keeps your business out of preventable disputes.

For most payments, account payee crossed cheques are the safest choice. For accounting teams, the cheque register and Tally reconciliation entries covered above eliminate most reconciliation headaches. For anyone dealing with a bounced cheque, the 30-day window for sending the legal notice is non-negotiable — miss it and you lose your Section 138 remedy.

This article is for educational purposes. It does not constitute legal or financial advice. For specific legal issues involving cheque bounce or Section 138 proceedings, consult a qualified advocate.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.