TDS TCS Master Table FY 2026-27 | New Income Tax Act 2025

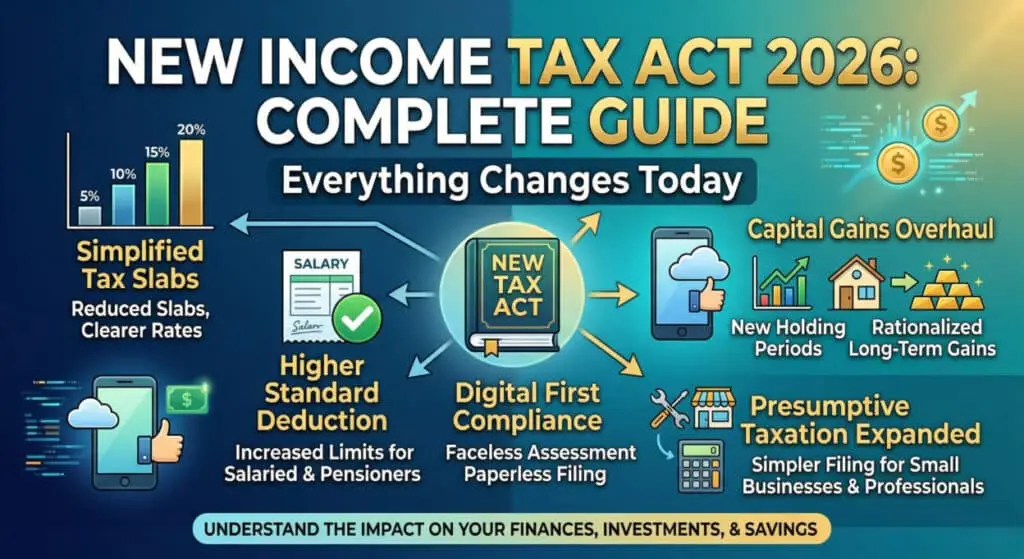

The New Income Tax Act 2025 has completely overhauled India’s TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) framework. Effective from Tax Year 2026-27, all old TDS sections (like 192, 194A, 194C, 194J etc.) are now renumbered and reorganised under new sections 392, 393, and 394. This is the most comprehensive restructuring of TDS/TCS provisions since the Income Tax Act 1961. In this blog post, we present the complete and updated TDS TCS Master Table FY 2026-27 for Tax Year 2026-27, covering all payment categories, new section numbers, applicable rates, threshold limits, and the new form numbers under the new Income Tax Act 2025. Whether you are a CA, accountant, tax professional, or individual taxpayer — this master reference will help you stay fully compliant. ⚠️ IMPORTANT: This table is based on the New Income Tax Act 2025 (effective Tax Year 2026-27). The old section numbers (192, 194A, etc.) are replaced by new sections (392, 393, 394). Always refer to the official Act for compliance. 1. What is TDS (Tax Deducted at Source)? TDS stands for Tax Deducted at Source. It is a mechanism under the Income Tax Act where the payer (deductor) deducts a specified percentage of tax from the payment made to the payee (deductee) and deposits it with the Government of India. The deductee can claim credit for TDS deducted while filing their Income Tax Return (ITR). TDS applies to a wide variety of payments including salaries, interest, rent, professional fees, contract payments, commission, dividends, lottery winnings, and more. Under the New Income Tax Act 2025, all TDS provisions are now consolidated under Section 392 and 393. What is TCS (Tax Collected at Source)? TCS stands for Tax Collected at Source. Unlike TDS (deducted by payer), TCS is collected by the seller from the buyer at the time of sale of specified goods or services. Common examples include sale of scrap, timber, minerals, motor vehicles above ₹10 lakh, and remittances under Liberalised Remittance Scheme (LRS). Under the new Act, TCS provisions are covered under Section 394. 2. Key Changes in TDS/TCS Under New Income Tax Act 2025 The New Income Tax Act 2025 has introduced sweeping changes to how TDS and TCS are structured. Here are the most critical changes every taxpayer and professional must know: 3. New Section Numbers: Old vs New Mapping Here is a quick reference table mapping old TDS/TCS sections to the new sections under the Income Tax Act 2025: Old Section New Section Category 192 (Salary) 392 TDS on Salary 192A (PF Withdrawal) 392 TDS on PF Withdrawal 193 (Interest on Securities) 393(1) Interest Income 194A (Interest from Banks) 393(1) Interest Income 194C (Contracts) 393(1) Contract Payments 194D (Insurance Commission) 393(1) Commission 194H (Other Commission) 393(1) Commission 194-I (Rent) 393(1) Rent 194-IA (Immovable Property) 393(1) Immovable Property 194J (Professional/Technical) 393(1) Professional & Technical 194K (Mutual Fund) 393(1) Specified Mutual Fund 194M (Contract/Professional – Large Payments) 393(1) Contract/Professional 194N (Cash Withdrawal) 393(3) Payment to any person 194O (TDS by ECO) 393(1) Others 194P (Specified Senior Citizen) 393(1) Others 194Q (Purchase of Goods) 393(1) Others 194R (Perquisite/Benefit) 393(1) Others 194S (VDA/Crypto) 393(1) Others 194T (Payment to Partner) 393(3) Payment to any person 194B (Lottery) 393(3) Payment to any person 194BA (Online Gaming) 393(3) Payment to any person 206C (TCS) 394 TCS 4. TDS Master Table – Salary & PF Withdrawal (Section 392) Salary TDS and PF withdrawal TDS now fall under the umbrella of Section 392 of the new Income Tax Act 2025. The applicable rates remain based on average slab rates for salary, and 10% for PF withdrawal above the threshold. New Section Code Category Nature of Payment Rate Threshold New Form 392 (Old: 192) 1001 TDS on Salary Govt Employee (non-union) Average Rate (Slab) As per slab Form 138 (Old: 24Q) 392 (Old: 192) 1002 TDS on Salary Private Employee Average Rate (Slab) As per slab Form 138 392 (Old: 192) 1003 TDS on Salary Indian Govt Employee Average Rate (Slab) As per slab Form 138 392 (Old: 192A) 1004 TDS on PF Withdrawal PF Withdrawal 10% ₹50,000 Form 140 (Old: 26Q) Key point: For salary TDS, the employer must consider the employee’s regime choice (New or Old Tax Regime) while computing average TDS rate. No change in this process under the new Act. 5. TDS Master Table – Commission & Rent (Section 393(1)) TDS on commission and rent continues with largely the same rates but is now governed by Section 393(1) with new transaction codes. New Section Code Category Nature of Payment Rate Threshold New Form 393(1) [194D] 1005 Commission Insurance Commission 2% ₹20,000 Form 140 393(1) [194H] 1006 Commission Other than Insurance 2% ₹20,000 Form 140 393(1) [194-IB] 1007 Rent – Individual/HUF Rent by Individual/HUF 2% ₹50,000 pm Form 141 393(1) [194-IB] 1008 Rent – Specified Person Plant & Machinery 2% ₹50,000 pm Form 140 393(1) [194-I] 1009 Rent – Specified Person Building 10% ₹50,000 pm Form 140 TDS on Rent – Individual/HUF (Form 141): When an individual or HUF pays rent exceeding ₹50,000 per month, TDS @ 2% is deducted. This is deposited using Form 141 (previously Form 26QC). No TAN required for individuals/HUF paying rent. 6. TDS Master Table – Immovable Property (Section 393(1)) TDS on purchase and transfer of immovable property is an important compliance requirement for homebuyers. The rates and thresholds under the new Act are as follows: New Section Code Category Nature of Payment Rate Threshold New Form 393(1) [194-I] 1010 Immovable Property Transfer of Immovable Property (Non-agricultural) 1% ₹50 Lakh Form 141 (Old: 26QB) 393(1) [194-IA] 1011 Immovable Property Joint Development Agreement 10% No threshold Form 140 393(1) [194-IC] 1012 Immovable Property Compensation / Enhanced Compensation 10% ₹5 Lakh Form 140 Homebuyers Note: If you are buying a property worth ₹50 lakh or more, you must deduct TDS @ 1% from the sale consideration and deposit it using Form 141. The seller’s PAN is mandatory. 7. TDS Master Table – Interest Income (Section 393(1)) TDS on interest income has been