Expanding a business across borders is the modern benchmark for success. It’s a sign of ambition, growth, and global reach. But as soon as your operations touch down in a new country, you enter a complex, high-stakes financial world governed by a web of international tax laws. This is where two of the most critical—and often misunderstood—concepts in global finance come into play: international tax planning and transfer pricing.

For many, these terms conjure up images of shadowy loopholes and aggressive avoidance schemes. But in today’s transparent, post-BEPS (Base Erosion and Profit Shifting) world, that view is dangerously outdated. Modern international tax planning is not about if you pay tax, but about where, when, and how much you pay, all while remaining in full compliance. It’s about strategy, risk management, and long-term sustainability.

And at the very heart of that strategy lies transfer pricing—the mechanism that governs the price of all transactions between related entities within a multinational group. Getting it wrong doesn’t just mean a higher tax bill; it can mean crippling penalties, double taxation, and endless disputes with tax authorities.

In this comprehensive guide, we will demystify international tax planning and transfer pricing. We’ll move from the basic definitions to the core principles, explore the advanced strategies multinationals use, and unpack the new global rules that are changing the game. Whether you are a CFO, a finance manager, or a business owner dreaming of expansion, this article will serve as your blueprint for navigating the complex but critical world of international tax.

The Two Pillars: What is International Tax Planning?

At its core, international tax planning is the process of structuring your company’s global operations and transactions to legally minimize your total tax liability.

However, the modern definition has evolved far beyond simply lowering the tax bill. It’s a strategic function that balances tax efficiency with operational goals and robust risk management.

Beyond “Saving Tax”: The Real Goals

A common misconception is that tax planning is just about finding the lowest tax rate. In reality, a sustainable strategy has three equally important goals.

Achieving Tax Efficiency vs. Tax Avoidance

- Tax Efficiency is the legitimate use of all available legal provisions, tax treaties, and incentives to reduce a tax burden. This could mean structuring an acquisition in a way that allows for the deduction of interest expenses or placing a regional headquarters in a country with a favorable tax treaty network.

- Tax Avoidance (or aggressive tax planning) involves exploiting legal loopholes in ways that go against the intent of the law, often using artificial structures with no real business purpose. This is what global regulators are cracking down on.

- Tax Evasion is the illegal non-payment or under-payment of taxes, which is a criminal offense.

A good international tax plan focuses only on efficiency, ensuring all structures are defensible and have a clear business, or “economic,” substance.

Managing Global Risk and Ensuring Compliance

The cost of non-compliance is almost always higher than the tax itself. A solid plan prioritizes risk management. This means:

- Avoiding “double taxation” (where the same profit is taxed in two different countries).

- Minimizing the risk of costly and time-consuming tax audits.

- Ensuring you can defend your tax positions against challenges from authorities.

- Staying ahead of rapid changes in global tax law (like the BEPS project).

Aligning Tax Strategy with Business Objectives

Your tax strategy should support your business, not dictate it. A “tax-perfect” structure that creates massive operational headaches is a failure.

A human-centered tax plan asks:

- Are we expanding into Germany? How does our tax structure support a German holding company?

- Are we launching a new digital product? How does our intellectual property (IP) structure protect its value and manage the resulting income?

- Are we acquiring a target in Asia? How do we finance that acquisition in a tax-efficient way and integrate their operations?

Key Concepts Every Multinational Enterprise (MNE) Must Know

To build a plan, you need to understand the building blocks. These are the core concepts that determine where and how your company is taxed.

Permanent Establishment (PE) Risk

This is perhaps the most critical risk for any expanding business. A “Permanent Establishment” is a fixed place of business in a foreign country that is significant enough for that country to claim taxing rights over your profits.

What constitutes a PE? It used to be simple—a factory, a shop, a permanent office. Today, the lines are blurred. A PE can be triggered by:

- A “dependent agent” (like a local sales employee) who has the authority to habitually conclude contracts in your company’s name.

- A home office of a senior executive who makes key management decisions from that location.

- A construction project that lasts longer than a specified period (often 6-12 months).

If you accidentally create a PE in a country, you could suddenly be liable for corporate taxes, VAT, and payroll taxes there, along with penalties for failing to register.

Controlled Foreign Corporations (CFC) Rules

CFC rules are an anti-abuse measure. They are designed to prevent companies from shifting “passive income” (like interest, dividends, and royalties) into offshore subsidiaries in low-tax or no-tax jurisdictions (tax havens) and leaving it there indefinitely to avoid tax.

Here’s how they work: If your company (the parent) in a high-tax country (e.g., the US, UK, Germany) controls a subsidiary in a tax haven, the CFC rules may force you to treat that subsidiary’s passive income as your own income in the current year, even if the subsidiary never paid you a dividend. This immediately subjects that income to tax in your home country.

Double Taxation Avoidance Agreements (DTAAs) or Tax Treaties

No company wants to pay tax on the same income twice. Double Taxation Agreements (DTAAs), or tax treaties, are bilateral agreements between two countries to prevent this.

They are the rulebook for cross-border transactions. They specify:

- Who gets to tax what: They define what constitutes a PE, so a company isn’t taxed in two places at once.

- Reduced Withholding Taxes: They often lower or eliminate withholding taxes on cross-border payments.

Withholding Taxes (on Dividends, Interest, and Royalties)

When you make certain payments to a foreign entity, the source country’s government often requires you to “withhold” a percentage of that payment and send it directly to them as tax.

- Example: Your US company owes a €1,000,000 royalty payment to its French parent company. The US domestic withholding tax rate might be 30%. You would have to pay €300,000 to the IRS and only €700,000 to your French parent.

- The Treaty Solution: The US-France tax treaty, however, might reduce the withholding tax on royalties to 0%. By properly filing for treaty benefits, you can pay the full €1,000,000 to your parent, significantly improving cash flow.

Your international tax plan is the “macro” strategy for how your company is structured. Now, let’s look at the “micro” tool that governs 90% of your day-to-day cross-border transactions: transfer pricing.

Demystifying Transfer Pricing: The Heart of International Tax

If your multinational company was a single entity, everything would be simple. But it’s not. It’s a group of related legal entities (a parent and its subsidiaries) that are constantly transacting with each other across borders.

- Your factory in Vietnam sells components to your assembly plant in Mexico.

- Your R&D center in Ireland licenses intellectual property to your US sales entity.

- Your parent company in the UK provides management and IT services to all its subsidiaries.

- Your holding company in Switzerland lends money to your Brazilian operation.

Transfer Pricing is the system for setting the price for these internal, intra-group transactions.

What is Transfer Pricing? A Simple Analogy

Imagine you own two companies: “ParentCo” in a country with a 30% tax rate and “SubCo” in a country with a 10% tax rate.

ParentCo produces a product for $50. It needs to “sell” it to SubCo, which then sells it to the final customer for $150.

- Aggressive Pricing: You set the transfer price at $50.

- ParentCo’s profit: $50 (price) – $50 (cost) = $0. (Tax paid: $0)

- SubCo’s profit: $150 (final price) – $50 (transfer price) = $100. (Tax paid: $10)

- Total Tax Paid: $10

- Fair Pricing: You set the transfer price at $100 (what an independent party might pay).

- ParentCo’s profit: $100 (price) – $50 (cost) = $50. (Tax paid: $15)

- SubCo’s profit: $150 (final price) – $100 (transfer price) = $50. (Tax paid: $5)

- Total Tax Paid: $20

By simply changing the internal “transfer price,” you shifted $100 of profit from a high-tax country to a low-tax country, reducing your global tax bill. This is exactly what tax authorities are trying to prevent.

The “Arm’s Length Principle”: The Golden Rule of Transfer Pricing

To stop this artificial profit shifting, more than 100 countries, led by the Organisation for Economic Co-operation and Development (OECD), have agreed on a single governing rule: The Arm’s Length Principle.

This principle is defined in Article 9 of the OECD Model Tax Convention. In simple terms, it states:

The price for a transaction between related parties must be the same as the price would have been if the two parties were independent, unrelated, and acting in their own best interests.

In our analogy, tax authorities would force you to prove that the $50 price was “arm’s length.” If you couldn’t, they would launch an audit, disregard your $50 price, and recalculate your taxes based on the $100 “arm’s length” price. This would result in a bill for $15 in back taxes for ParentCo, plus interest, plus significant penalties.

Your entire transfer pricing strategy, documentation, and defense rest on your ability to prove that your internal prices are arm’s length.

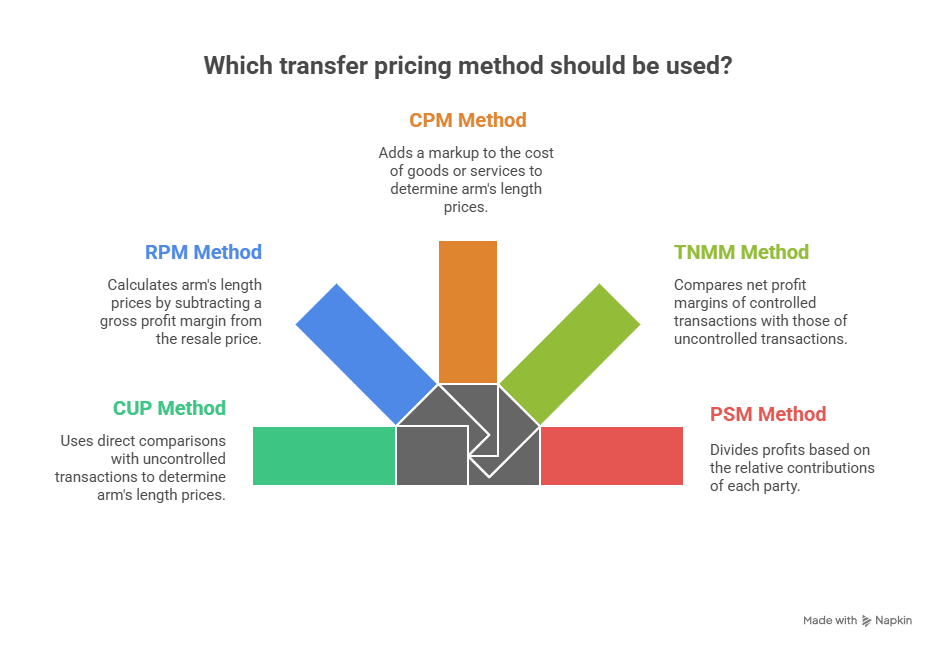

The “How-To”: The 5 Core Transfer Pricing Methods

So, how do you prove your price is “arm’s length”? You can’t just guess. The OECD provides five specific methods to establish and test your pricing. These methods are split into two categories.

Traditional Transaction Methods

These methods are preferred by tax authorities because they directly compare the price or margins of a specific transaction to an independent one.

Method 1: Comparable Uncontrolled Price (CUP) Method

This is the “gold standard” and the most direct method. You compare the price and conditions of your controlled (internal) transaction to those of an uncontrolled (external) transaction.

- Internal CUP: Your company sells the exact same product to both its own subsidiary and an independent third-party customer. The price charged to the third party is the CUP.

- External CUP: You find a transaction between two completely independent companies for the same product under the same conditions.

- Best for: Commodity goods (e.g., oil, coffee, copper), financial transactions (e.g., loans).

- Challenge: Requires very high comparability. Any differences in product, market, or terms must be reliably adjusted for.

Method 2: Resale Price Method (RPM)

This method is used for distributors and resellers. It starts with the final price the product is sold to an independent customer and works backward.

- How it works:

- Start with the Resale Price (the price your subsidiary sells to a final customer).

- Subtract a “Resale Price Margin” (a gross margin that an independent distributor would need to cover its costs and make a fair profit).

- The result is the arm’s length transfer price for the product your subsidiary bought from the parent.

- Example: SubCo (in Germany) buys goods from ParentCo (in Japan) and sells them to German customers for $100. If a comparable independent German distributor earns a 20% gross margin, the arm’s length transfer price is $80 ($100 – 20%).

- Best for: Marketing and distribution operations.

Method 3: Cost Plus Method (CPM)

This method is used for manufacturers and service providers. It starts with the costs of the supplier and adds a markup.

- How it works:

- Calculate the supplier’s (e.g., your internal factory’s) Costs of Goods Sold (COGS) for the product or service.

- Add a “Cost Plus Mark-Up” (a gross mark-up that an independent manufacturer would earn for a similar function).

- The result is the arm’s length transfer price.

- Example: Your factory in Vietnam (SubCo) manufactures a product for ParentCo. The total cost is $50. If comparable independent factories in Vietnam earn a 10% mark-up on their costs, the arm’s length transfer price is $55 ($50 + 10%).

- Best for: Routine manufacturing, assembly, and internal R&D or IT services.

Transactional Profit Methods

When you can’t find comparable transactions (like for unique products or integrated services), you move to comparing profits.

Method 4: Transactional Net Margin Method (TNMM)

This is now the most commonly used method in the world due to its flexibility. Instead of comparing gross margins (like RPM/CPM), it compares the net profit margin (like operating profit) of one of the entities (the “tested party”) to the net profit margins of independent companies performing similar functions.

- How it works: You test your subsidiary’s operating profit (relative to sales, costs, or assets) against a “benchmark” range of profits earned by comparable independent companies found in a database. As long as your subsidiary’s profit falls within that arm’s length range, your pricing is accepted.

- Best for: Almost any transaction where one side performs less complex functions (e.g., a “limited-risk” distributor or a “contract” manufacturer).

Method 5: Profit Split Method (PSM)

This is the most complex method, reserved for highly integrated or unique transactions where both sides contribute significant, valuable, and unique intellectual property.

- Example: Two subsidiaries in different countries co-develop a new piece of pharmaceutical or software technology. It’s impossible to say one is just a “supplier” and one is a “distributor.”

- How it works: You first calculate the total combined profit from the entire value chain. Then, you “split” that profit between the entities based on their relative contributions (e.g., who performed what R&D, who took on what risk, who owns the underlying IP).

- Best for: Co-development of valuable IP, integrated global financial trading.

How to Choose the “Most Appropriate Method”

You don’t get to just pick the method that gives you the lowest tax bill. The rules require you to select the “most appropriate method” based on a “functional analysis”—a deep dive into the facts and circumstances of the transaction, asking:

- What functions does each entity perform? (R&D, manufacturing, marketing, risk management)

- What assets does each entity use? (Factories, technology, customer lists)

- What risks does each entity assume? (Market risk, credit risk, inventory risk)

The entity that does more—performs key functions, owns valuable IP, and assumes major risks—is entitled to the majority of the profit.

The New Global Rulebook: The OECD/G20 BEPS Project

For decades, the rules we just discussed were the entire game. But in the 2010s, it became clear they weren’t working. Highly digitalized companies (like Google, Apple, and Amazon) were legally booking billions in profits in jurisdictions where they had no sales and few employees, resulting in minimal tax.

This led to public and political outrage, culminating in the OECD/G20 Base Erosion and Profit Shifting (BEPS) Project.

What is BEPS and Why Was It Created?

BEPS is the single most significant overhaul of international tax rules in a century. It’s a package of 15 “Actions” designed to stop MNEs from “shifting” profits from high-tax jurisdictions (where value is created) to low-tax jurisdictions (where there is little “substance”).

Most of the 15 Actions are highly technical, but the entire project has been consolidated into two revolutionary “Pillars.”

Pillar One: Taxing the Digital Giants

Pillar One is a radical departure from the old rules. It’s no longer just about where your factory or employees are. It’s about where your customers are.

- Who it affects: The very largest MNEs (initially, those with global revenue over €20 billion).

- What it does: It takes a portion of these companies’ “residual profits” (their super-profits) and re-allocates the taxing rights to the “market jurisdictions”—the countries where their users and customers are located, even if the company has no physical presence there.

- The Impact: This is a direct answer to the “digital tax” problem. It means a company can no longer sell into a country from an offshore hub and pay no tax there.

Pillar Two: The 15% Global Minimum Tax (GloBE)

Pillar Two is even more revolutionary. It has effectively ended the concept of the “zero-tax haven” for large MNEs.

- Who it affects: Large MNEs (with global revenue over €750 million).

- What it does: It ensures that these MNEs pay a minimum effective tax rate (ETR) of 15% on their profits in every single jurisdiction where they operate.

- How it works (The “Top-up Tax”):

- Your MNE calculates its ETR in every country.

- Imagine in Country A (a “tax haven”), your ETR is only 5%.

- Pillar Two’s “Income Inclusion Rule” (IIR) kicks in. Your ultimate Parent company (e.g., in the US) will be forced to pay a “top-up tax” of 10% (15% – 5%) to its own government on those Country A profits.

- The Impact: This completely removes the incentive to shift profits to a 0% tax jurisdiction, because you’ll just end up paying the 15% tax back home anyway. This is the “end of the race to the bottom” on corporate tax rates.

The “Economic Substance” Doctrine: Why Shell Companies No Longer Work

Flowing from the BEPS project, a powerful “economic substance” doctrine is now law in most major economies. Tax authorities no longer care about legal ownership—they care about commercial reality.

You can no longer have a “shell company” in the Cayman Islands that “owns” your billion-dollar patent but has no R&D staff, no offices, and one part-time director. Tax authorities will simply disregard this “brass plate” company and attribute the patent’s income to the company where the real R&D work (the “key people functions”) was actually done.

Key Strategies in Modern International Tax Planning

So, given this new, transparent, and complex world, what do “good” international tax planning strategies look like today? They are all about substance, alignment, and efficiency.

Strategic Holding Company Locations

A holding company owns the shares of your operating subsidiaries. Choosing its location is a critical decision. The old strategy was to pick a 0% tax location. The new, post-BEPS strategy is to pick a “substance” jurisdiction that offers a good balance of benefits.

Factors to Consider: Tax Treaties, IP Protection, and Substance

- Vast Tax Treaty Network: A location like the Netherlands, UK, or Singapore is popular because it has treaties with 100+ countries, reducing withholding taxes on dividends and royalties flowing up from all your subsidiaries.

- IP Protection: A jurisdiction with strong legal protection for intellectual property (like Ireland or Switzerland).

- Participation Exemption: A rule that states dividends and capital gains received by the holding company from its subsidiaries are not taxed. This is crucial for reinvesting profits.

- Substance: A location where you can actually base real C-suite executives and management functions to justify the company’s existence.

Optimizing Your Intellectual Property (IP) Structure

Your IP (patents, software, brand) is often your most valuable asset. The strategy is to house this IP in a location that aligns with its development and maximizes its after-tax value.

The “Patent Box” or “IP Box” Regime

Many countries (like the UK, Switzerland, and Ireland) offer “Patent Box” (or IP Box) regimes. These are special, low corporate tax rates (e.g., 6-10%) applied specifically to income derived from qualifying IP (like patent royalties). This is a government-approved incentive to encourage R&D, and it’s fully BEPS-compliant.

Managing IP Development vs. IP Ownership

Your IP structure must align with “economic substance.” The entity that legally owns the IP must also be the entity that functionally controls, funds, and manages its development and risks. You can’t have your US team do all the R&D and then “sell” the resulting patent to a Bermuda shell company for $1. This is a primary target for transfer pricing audits.

Centralized Group Functions

As MNEs grow, they find efficiencies by centralizing key functions rather than duplicating them in every country. This creates new intra-group transactions that require transfer pricing.

Treasury and In-House Financing (Intra-group loans)

Instead of 20 subsidiaries all getting external bank loans, a central “Treasury” company can raise capital on behalf of the group and then lend it to subsidiaries (an intra-group loan). The transfer pricing challenge is setting an “arm’s length” interest rate for these loans.

Centralized Procurement or Management Services

A central entity may provide IT, HR, legal, and marketing “management services” to all subsidiaries. These subsidiaries must pay an “arm’s length” fee for these services. This fee is often calculated using the Cost Plus Method (the total cost of the service center plus a small, arm’s length mark-up, typically 5-10%).

Compliance and Documentation: Your Shield in an Audit

You can have the best strategy in the world, but if you can’t prove it to a tax auditor, it’s worthless.

The BEPS project (specifically Action 13) created a new, global “three-tiered” standard for transfer pricing documentation. This is your mandatory annual compliance burden.

The Three-Tiered Documentation Standard

The Master File (The Global Blueprint)

This is a high-level report that gives a “blueprint” of your entire global MNE group. It describes:

- Your organizational structure.

- Your major business lines and value drivers.

- Your overall transfer pricing policies.

- Your main intangible assets, financing arrangements, and tax rulings.

The Local File (The Country-Specific Proof)

This is the detailed, “on-the-ground” report that every country requires. It provides the specific proof for that country’s transactions. It includes:

- A description of the local company and its management.

- The “functional analysis” for all its intra-group transactions.

- The method selection (CUP, TNMM, etc.) for each transaction.

- The benchmarking analysis (the database search for comparable companies) that proves your pricing is arm’s length.

- A copy of all intercompany legal agreements.

This is your primary shield in an audit.

Country-by-Country (CbC) Reporting

For large MNEs (over €750 million revenue), this is an annual, high-level data file submitted to tax authorities. It shows, for every country you are in:

- Total Revenue

- Profit Before Tax

- Tax Paid

- Number of Employees

- Stated Capital

- Tangible Assets

This is a risk-assessment tool. If a tax authority sees a CbC report showing a company has €500M in profit, 2 employees, and €0 tax paid in their jurisdiction, that company is getting audited.

The High Cost of Non-Compliance

Failing to prepare this documentation, or getting the analysis wrong, is extremely costly.

- Penalties: Most countries have severe, automatic penalties for failing to provide a Local File on request.

- Tax Adjustments: The auditor will recalculate your profits, leading to a large tax bill.

- Interest: You will pay interest on the underpaid tax, often at a high rate.

- Double Taxation: The worst-case scenario. Country A audits you and says your price should have been $100, not $80. You pay them back-tax. But Country B (where the other entity is) refuses to give you a refund for the tax it already collected on that $20 of profit. That $20 is now taxed in both countries. This can raise your ETR to 60-70% on that transaction.

Proactive Defence: What is an Advance Pricing Agreement (APA)?

An APA is the ultimate risk-management tool. Instead of waiting to be audited, you proactively go to one or more tax authorities, present your entire transfer pricing methodology, and ask them to agree to it in advance.

- Unilateral APA: An agreement between you and one tax authority (e.g., the IRS).

- Bilateral APA: An agreement between you and two tax authorities (e.g., the IRS and the German tax authority).

If granted, the APA provides you with legal certainty that your transfer pricing will not be challenged for a fixed period (usually 3-5 years), as long as you stick to the agreed method.

The Future: What’s Next for International Tax and Transfer Pricing?

The world of international tax never stands still. The changes from 2020-2025 have been the most significant in history, and the pace is only accelerating.

The Rise of AI and Data Analytics in Tax Audits

Tax authorities are now tech companies. They are using AI and sophisticated data analytics to process your CbC reports, tax returns, and even public information to “risk-score” taxpayers for audits. They can now spot anomalies and inconsistencies in seconds that would have taken a human auditor weeks to find.

Increased Focus on ESG and Tax Transparency

Tax is no longer just a financial issue; it’s a reputational one. A company’s tax strategy is now a core part of its Environmental, Social, and Governance (ESG) narrative. Investors, activists, and the public are demanding to know that companies are paying their “fair share.” Aggressive tax planning, even if legal, can lead to massive brand damage.

The Evolving Challenges of the Digital and “Work from Anywhere” Economy

The BEPS rules are still catching up to new realities:

- Remote Work: What happens when your senior developer, who is key to your IP, moves to Spain to work remotely? Does she accidentally create a “Permanent Establishment” for your company in Spain?

- The Metaverse & NFTs: How do you tax an asset that only exists digitally, was created by an anonymous developer, and is “located” on a decentralized blockchain?

These are the questions tax planners and authorities are grappling with right now.

Conclusion: From Defensive Compliance to Strategic Advantage

International tax planning and transfer pricing have evolved from a niche, back-office compliance function into one of the most critical strategic pillars of a global business.

Gone are the days of simple “tax avoidance” and shell companies. We are in a new era of mandatory transparency, global minimum taxes, and economic substance. In this world, a “human-first” approach to tax planning is the only one that wins.

The goal is no longer to simply find the lowest tax rate. The goal is to build a resilient, sustainable, and defensible global structure. A structure that supports your business operations, stands up to scrutiny from auditors, avoids double taxation, and aligns with your public reputation.

Companies that treat transfer pricing as a mere compliance checkbox will be buried in audits, penalties, and reputational risk. Companies that embrace it as a strategic tool—a way to align their tax, finance, and operational models—will create a powerful and lasting competitive advantage.

FAQs

What is the main difference between international tax planning and transfer pricing?

International tax planning is the overall strategy for managing a company’s global tax liabilities. Transfer pricing is a specific tool within that strategy used to set prices for transactions between a company’s own related entities, ensuring compliance with the arm’s length principle.

What is the “arm’s length principle”?

It’s the international standard that states transactions between related companies (e.g., a parent and its subsidiary) should be priced as if they were two independent, unrelated companies. This prevents artificial profit shifting to low-tax countries.

What is the OECD’s BEPS project?

BEPS stands for Base Erosion and Profit Shifting. It’s a global project by the OECD and G20 to combat tax avoidance. It created new rules (like the 15% global minimum tax) to ensure multinational enterprises pay tax where their real economic activities occur.

What are the 5 main transfer pricing methods?

The five methods are: (1) Comparable Uncontrolled Price (CUP) Method, (2) Resale Price Method (RPM), (3) Cost Plus Method (CPM), (4) Transactional Net Margin Method (TNMM), and (5) Profit Split Method (PSM).

Why is transfer pricing documentation (Master File/Local File) so important?

This documentation is your primary evidence to prove to tax authorities that your inter-company pricing is compliant with the arm’s length principle. Without it, you are defenseless in an audit and face significant penalties and tax adjustments.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.