In a world driven by numbers, where fortunes are made and lost in the blink of an eye, the integrity of financial data is paramount. Yet, beneath the polished surface of balance sheets and income statements, a darker world of deception often lurks. From multi-billion dollar corporate scandals that topple giants to intricate cyber-frauds that vanish with digital dust, financial crime is more sophisticated than ever.

But who stands guard against this rising tide of deceit? Who are the detectives of the financial world, the bloodhounds who can sniff out a single fraudulent entry among millions?

Enter the Forensic Accountant.

This is not your typical bean-counter’s tale. Forget the dusty ledgers and monotonous calculations. We are diving headfirst into the thrilling, high-stakes world of forensic accounting and fraud detection. This comprehensive guide will take you behind the scenes, exploring the skills, techniques, and real-life dramas that define this critical profession. Whether you’re a student aspiring to a dynamic career, a business owner aiming to protect your assets, or simply a curious mind, prepare to be captivated.

What Exactly is Forensic Accounting? More Than Just Crunching Numbers

At its core, forensic accounting is the specialized practice of combining accounting, auditing, and investigative skills to examine the finances of an individual or business. The term “forensic” itself means “suitable for use in a court of law.” This is the key differentiator: the findings of a forensic accountant are intended to be used in legal proceedings.

Think of it this way: a traditional accountant is like a family doctor, performing regular check-ups to ensure a company’s financial health. A forensic accountant is the specialist surgeon, called in when there’s a critical issue—a suspicion of fraud, a legal dispute, or a financial crime that needs to be dissected and understood.

The Forensic Accountant vs. The Traditional Auditor: A Tale of Two Mindsets

While both roles involve scrutinizing financial records, their objectives and mindsets are worlds apart.

| Feature | Traditional Auditor | Forensic Accountant |

| Objective | To express an opinion on the fairness of financial statements. | To determine if fraud has occurred and to quantify the loss. |

| Scope | A general review of financial data. | Specific, targeted investigation of a particular issue. |

| Mindset | Professional skepticism. | “Proof of wrongdoing” mindset. Assumes nothing. |

| Techniques | Sampling and testing of transactions. | In-depth analysis, interviews, evidence gathering. |

| Reporting | Audit report to stakeholders. | Detailed report and expert testimony for legal proceedings. |

The Two Pillars of Forensic Accounting: Investigation and Litigation Support

The work of a forensic accountant typically falls into two major categories, each serving a distinct purpose in the pursuit of financial truth.

Investigative Accounting: Following the Money Trail

This is the reactive side of the profession. When a “red flag” is raised—perhaps a whistleblower’s tip, an anonymous letter, or an anomaly discovered during a routine audit—the forensic accountant is deployed. Their mission is to investigate allegations of fraud, such as:

- Asset Misappropriation: The most common type of fraud. This includes everything from an employee stealing petty cash to complex schemes involving fake invoices and shell companies to siphon off funds.

- Financial Statement Fraud: This is often the most costly type of fraud, perpetrated by senior management to deceive investors and creditors. It involves deliberately misrepresenting the company’s financial health by inflating revenues, hiding liabilities, or manipulating expenses. The infamous Enron and Satyam scandals are classic examples.

- Corruption: This includes bribery, conflicts of interest, and extortion. A forensic accountant might investigate a purchasing manager who accepts kickbacks from a supplier in exchange for a lucrative contract.

Litigation Support: The Accountant in the Courtroom

Litigation support involves providing assistance and expertise in legal matters. Here, the forensic accountant acts as a financial expert, helping to resolve disputes and presenting complex financial information in a clear, understandable way. Their services are crucial in cases such as:

- Shareholder and Partnership Disputes: Valuing a business or determining profits in a contentious separation.

- Insurance Claims: Calculating economic losses from business interruptions, property damage, or employee theft.

- Divorce Proceedings: Tracing and valuing marital assets, especially when one party is suspected of hiding funds.

- Expert Witness Testimony: This is the pinnacle of litigation support. The forensic accountant takes the stand in court to explain their findings to a judge and jury, breaking down intricate financial schemes into simple, compelling testimony.

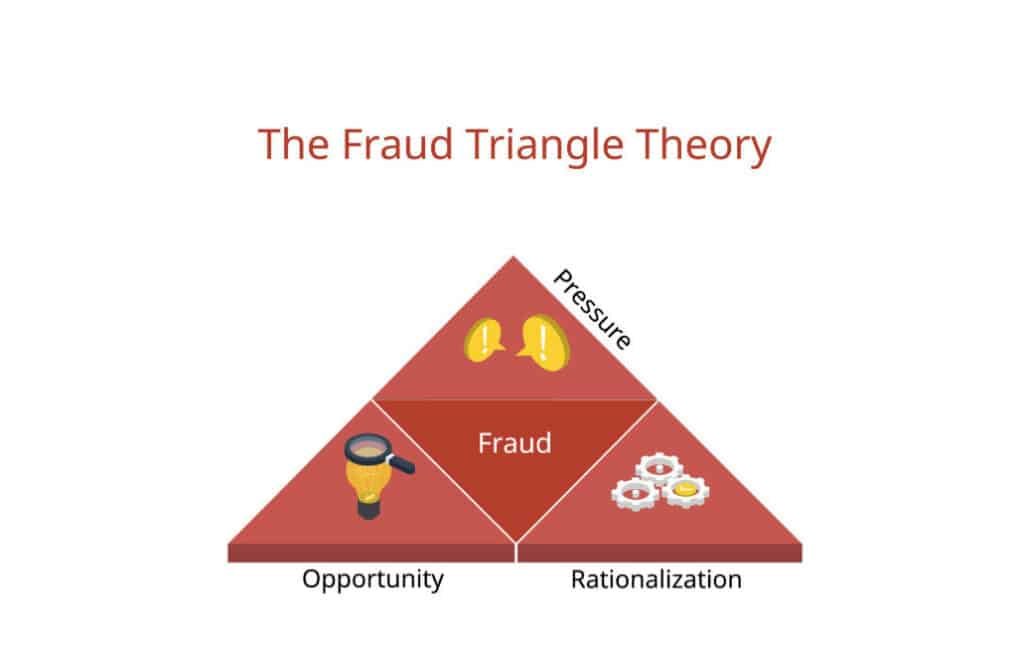

The Psychology of Deceit: Understanding the Fraud Triangle

To catch a fraudster, you must first understand what drives them. Why do seemingly ordinary, trusted employees or executives cross the line into criminal behavior? Criminologist Donald R. Cressey developed a powerful model to explain this: the Fraud Triangle. It posits that for fraud to occur, three elements must be present.

Pressure: The Motivation Behind the Crime

This is the “why.” The individual feels a non-shareable financial pressure. This could be:

- Personal Vices: Gambling debts, drug addiction, or an extravagant lifestyle beyond their means.

- Financial Hardship: Mounting medical bills, a spouse’s job loss, or overwhelming debt.

- Work-Related Pressure: An intense pressure to meet unrealistic earnings targets or performance goals set by the company.

Opportunity: The Opening to Commit the Act

This is the “how.” The individual perceives a clear opportunity to commit the fraud, conceal it, and avoid being caught. This often arises from:

- Weak Internal Controls: Lack of segregation of duties (e.g., the same person authorizes payments, signs checks, and reconciles the bank account).

- Poor Management Oversight: A lack of supervision or review of employees’ work.

- Abuse of Trust: The individual is in a position of authority and trust, allowing them to override controls.

Rationalization: The Justification for the Dishonesty

This is the internal “it’s okay because…” conversation. The fraudster justifies their actions to themselves, allowing them to maintain their self-image as an honest person. Common rationalizations include:

- “I’m just borrowing the money; I’ll pay it back.”

- “The company owes me. I’m underpaid and overworked.”

- “It’s not hurting anyone; it’s a big, faceless corporation.”

- “I’m doing it for the good of the company, to save it from bankruptcy.”

A forensic accountant keeps the Fraud Triangle in mind during an investigation. It helps them identify potential suspects, understand motives, and pinpoint weaknesses in a company’s defenses.

The Forensic Accountant’s Arsenal: Skills and Superpowers

Becoming a successful forensic accountant requires a unique blend of left-brain analytics and right-brain creativity. It’s not just about being good with numbers; it’s about seeing the story behind the numbers.

The Essential Skill Set: Are You a Financial Detective in the Making?

- Meticulous Attention to Detail: The ability to spot a tiny inconsistency that could unravel a massive fraud. It’s looking for the single stray thread in a perfectly woven tapestry.

- Analytical Mindset: Not just identifying what happened, but why it happened. Connecting disparate pieces of information to see the bigger picture.

- Stellar Interviewing Skills: A forensic accountant must be part psychologist, part journalist. They need to interview witnesses and suspects, build rapport, and know when someone is being deceptive.

- Deep Understanding of Legal Concepts: They must know the rules of evidence, understand legal procedures, and be able to work seamlessly with lawyers.

- Crystal-Clear Communication: The ability to take complex financial jargon and explain it in simple, layman’s terms to a jury or a client is perhaps the most critical skill of all.

- Unshakeable Integrity: The profession demands the highest ethical standards. A forensic accountant must remain objective and impartial, no matter how high the stakes.

The Techniques of the Trade: Uncovering Hidden Truths

Forensic accountants use a variety of powerful techniques and technologies to follow the digital and paper trails left by fraudsters.

Data Analytics and Computer Forensics

In today’s digital age, the smoking gun is rarely a piece of paper; it’s a string of data on a server. Forensic accountants use sophisticated software to analyze vast amounts of electronic data (a process known as e-discovery). They can:

- Recover Deleted Files: Find emails, spreadsheets, and documents that a suspect thought were long gone.

- Identify Patterns and Anomalies: Use data mining to flag suspicious transactions, such as payments to vendors who share an address with an employee, or duplicate invoice numbers.

- Apply Benford’s Law: This fascinating statistical principle states that in many naturally occurring sets of numbers, the first digit is more likely to be small. For example, the number 1 appears as the leading digit about 30% of the time, while 9 appears less than 5% of the time. If the numbers in a company’s financial records deviate significantly from this pattern, it can be a red flag for fabricated figures.

The Art of the Interview

Beyond the data, the human element is key. A forensic accountant conducts interviews to gather information, corroborate evidence, and assess credibility. They might interview the whistleblower, co-workers, and, eventually, the suspect themselves. These are not casual chats; they are strategically planned conversations designed to elicit crucial information.

The Investigation Blueprint: A Step-by-Step Guide to a Forensic Audit

Every forensic investigation is unique, but it generally follows a structured process to ensure that all evidence is collected legally and that the findings are robust and defensible.

Step 1: Accepting the Engagement and Planning

It all starts with a meeting. The forensic accountant meets with the client (a company’s board, lawyers, etc.) to understand the nature of the suspicion. They define the scope of the investigation: What is the alleged fraud? Who is involved? What is the time period in question? Based on this, they develop a detailed investigation plan.

Step 2: Gathering Evidence

This is the heart of the investigation. The team collects all relevant information, which can include:

- Financial Records: General ledgers, invoices, bank statements, expense reports.

- Electronic Evidence: Emails, server logs, hard drives, and mobile phone records.

- Public Records: Property records, corporate filings, and social media activity.

- Interviews: Speaking with employees and other relevant parties.

Crucially, they must maintain a meticulous chain of custody for all evidence to ensure it is admissible in court.

Step 3: Analyzing the Evidence

The collected data is then painstakingly analyzed. The team looks for patterns, anomalies, and red flags. This is where techniques like data mining and Benford’s Law come into play. They trace transactions, reconstruct events, and build a timeline of the fraudulent activity.

Step 4: Reporting the Findings

Once the analysis is complete, the forensic accountant prepares a detailed report. This report is a clear, concise, and factual summary of the investigation. It outlines:

- How the fraud was perpetrated.

- The financial loss incurred.

- The evidence supporting the conclusions.

- Recommendations for improving internal controls to prevent future occurrences.

Step 5: Testifying in Court

If the case goes to trial, the forensic accountant may be called as an expert witness. They will present their findings to the court, explain the complex financial evidence in simple terms, and withstand cross-examination from the opposing counsel. Their credibility and clarity on the stand can make or break a case.

A Booming Field: Career Scope for Forensic Accountants in India

With the rise of corporate governance standards, stricter regulations, and an unfortunate increase in white-collar crime, the demand for forensic accountants in India is skyrocketing. The field offers a dynamic and rewarding career path for those with the right skills and temperament.

Where are the Opportunities?

Forensic accountants are in high demand across a wide range of sectors:

- Professional Services Firms: The “Big Four” (Deloitte, PwC, EY, KPMG) and other major consulting firms have large and growing forensic practices.

- Corporations: Large companies are building in-house forensic teams to conduct internal investigations and manage fraud risk.

- Banking and Insurance: These sectors are particularly vulnerable to fraud and heavily rely on forensic experts to investigate money laundering, fraudulent claims, and cybercrime.

- Government and Law Enforcement: Agencies like the Serious Fraud Investigation Office (SFIO), the Central Bureau of Investigation (CBI), and the Economic Offences Wing (EOW) employ forensic accountants to investigate complex financial crimes.

- Insolvency and Bankruptcy: Under the Insolvency and Bankruptcy Code (IBC), forensic audits are often required to investigate the reasons for a company’s failure and to trace any diverted assets.

Key Job Roles and Salary Prospects

The career ladder in forensic accounting is steep and lucrative.

| Job Role | Average Annual Salary (INR) |

| Forensic Accountant (Entry-Level) | ₹6,00,000 – ₹9,00,000 |

| Internal Auditing Manager | ₹10,00,000 – ₹15,00,000 |

| Financial Forensic Consultant | ₹12,00,000 – ₹20,00,000 |

| Senior Manager/Director (Forensics) | ₹25,00,000+ |

(Note: Salaries are indicative and can vary based on experience, certification, and employer.)

Getting Certified: Your Gateway to the Profession

While a background in accounting or finance is essential, specialized certifications can significantly boost your career prospects. The most globally recognized credential is the Certified Fraud Examiner (CFE) from the Association of Certified Fraud Examiners (ACFE). In India, certifications like the Certified Forensic Accounting Professional (CFAP) are also highly valued.

Frauds That Shook the World: Case Studies

The best way to understand the impact of forensic accounting is to look at the real-world scandals they helped uncover. These cases serve as cautionary tales and highlight the critical role of financial investigation.

The Satyam Computers Scandal (2009): India’s Enron

- The Fraud: The chairman of Satyam, Ramalinga Raju, confessed to manipulating the company’s accounts for years, inflating revenues and profits to the tune of over ₹7,000 crore (approximately $1.5 billion). He created fake invoices, falsified bank statements, and essentially invented a company that was far more successful on paper than it was in reality.

- The Aftermath: The scandal sent shockwaves through the Indian corporate world. Forensic accountants were brought in to unravel the complex web of deceit. They had to sift through mountains of fabricated data to determine the true financial position of the company. The case led to stricter corporate governance norms and a greater emphasis on the role of independent auditors in India.

The Enron Scandal (2001): A House of Cards

- The Fraud: Enron, a US energy trading company, used complex and deceptive accounting practices to hide massive debts and inflate its earnings. They created special purpose entities (SPEs) to move liabilities off their balance sheet, making the company appear incredibly profitable when it was actually on the brink of collapse.

- The Aftermath: When the truth came out, Enron’s stock price plummeted, and the company filed for bankruptcy, wiping out thousands of jobs and billions in shareholder value. Forensic investigators played a crucial role in exposing the fraud, leading to the conviction of top executives and the dissolution of Arthur Andersen, one of the world’s largest accounting firms at the time. This scandal directly led to the Sarbanes-Oxley Act of 2002, a landmark piece of legislation aimed at preventing corporate fraud.

Bernie Madoff’s Ponzi Scheme (2008): The $65 Billion Lie

- The Fraud: Bernie Madoff, a respected Wall Street figure, orchestrated the largest Ponzi scheme in history. For decades, he paid returns to earlier investors using capital from new investors, rather than from actual investment profits. His firm’s financial statements were a complete fabrication.

- The Aftermath: The scheme collapsed during the 2008 financial crisis, and thousands of investors lost their life savings. Forensic accountants were tasked with the monumental job of tracing billions of dollars through a labyrinth of accounts to identify what could be recovered for the victims. The case highlighted the devastating human cost of financial fraud and the importance of due diligence.

The Future is Here: Technology and the Evolution of Forensic Accounting

The world of fraud detection is in a constant state of flux. As businesses become more digital, so do the criminals. The future of forensic accounting lies in leveraging cutting-edge technology to stay one step ahead.

- Artificial Intelligence (AI) and Machine Learning: AI algorithms can analyze massive datasets in real-time, identifying subtle patterns and anomalies that a human investigator might miss. They can learn from past fraud cases to predict and flag suspicious behavior before significant losses occur.

- Blockchain Analysis: While cryptocurrencies can be used for illicit activities, the underlying blockchain technology provides a permanent and immutable ledger. Forensic accountants with expertise in blockchain analysis can trace the flow of digital assets to uncover money laundering and other crimes.

- Predictive Analytics: Instead of just reacting to fraud, the focus is shifting to preventing it. By analyzing historical data and external factors, predictive models can assess the risk of fraud in different areas of a business, allowing for proactive measures to be taken.

The forensic accountant of the future will be a hybrid professional—part accountant, part data scientist, part investigator—adept at using technology to find the truth in a sea of data.

Conclusion

Forensic accounting is more than a profession; it’s a calling. It’s for those who are driven by a desire for truth and justice, who possess an insatiable curiosity, and who thrive on solving complex puzzles. In an age of digital complexity and moral ambiguity, the role of the forensic accountant has never been more vital.

They are the guardians at the gate of our financial systems, the unsung heroes who work in the shadows to expose the truth, protect investors, and hold the guilty accountable. They remind us that while numbers can be used to lie, they cannot lie forever. In the end, the truth will always be found in the details.

FAQs

What is forensic accounting?

Forensic accounting is a specialized field of accounting that combines accounting, auditing, and investigative skills to examine financial records in order to uncover illegal activity. The findings from a forensic audit are suitable for use in a court of law, hence the term “forensic.” Think of them as financial detectives.

How is forensic accounting different from a regular audit?

A regular audit aims to provide an opinion on whether a company’s financial statements are presented fairly and accurately. It’s like a general health check-up. Forensic accounting, on the other hand, is performed to investigate a specific suspicion of fraud or wrongdoing. It’s like calling in a specialist surgeon to find and fix a specific problem.

What is the Fraud Triangle?

The Fraud Triangle is a framework used to explain why someone decides to commit fraud. It consists of three elements that are usually present when fraud occurs:

Pressure: A financial need or motivation (e.g., debt, addiction, medical bills)

Opportunity: A perceived chance to commit the fraud with a low risk of being caught (e.g., weak internal controls).

Rationalization: A personal justification for the dishonest act (e.g., “The company owes me,” or “I’m just borrowing it”).

What skills does a forensic accountant need?

A successful forensic accountant needs a unique blend of skills, including:

1. Strong analytical abilities and attention to detail.

2. A skeptical and investigative mindset.

3. Excellent communication and interviewing skills.

4. A deep understanding of accounting principles, legal procedures, and rules of evidence.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.