Over 4 crore Indian taxpayers will pay zero income tax in FY 2025-26 — and most of them don’t fully understand why. Section 87A of the Income Tax Act 1961 is the reason.

Many salaried individuals either miss this rebate entirely or misapply it, ending up paying tax they don’t owe. The calculation is not complicated, but the rules differ by tax regime, income level, and the type of income you earn — and getting those details wrong costs money.

In this guide, you’ll learn exactly How Is Section 87A Rebate Calculated step by step, which tax regime gives you more benefit, and how marginal relief protects you if your income just crosses the threshold — without wading through dense legal language.

As a tax practitioner with experience filing returns for salaried and self-employed individuals across India, the most common filing mistake I see is taxpayers missing the 87A rebate claim on their ITR.

What Is Section 87A of the Income Tax Act 1961?

Section 87A sits inside Chapter VIII of the Income Tax Act 1961, which deals with rebates and reliefs. The government introduced it in FY 2013-14 to reduce tax burden on low-to-middle income resident individuals.

What is Section 87A Rebate?

Section 87A is a direct rebate on your final income tax liability – not a deduction from income. It works by subtracting the rebate amount from the tax calculated on your taxable income, before the 4% health and education cess is applied. It applies to resident individuals whose net taxable income falls within the prescribed limit for their chosen tax regime.

The key distinction: a deduction reduces your taxable income; the 87A rebate reduces the tax you owe after income is already computed. This makes it one of the most powerful provisions in the Act for eligible taxpayers.

Who Is Eligible for Tax Rebate Under Section 87A?

Eligibility under Section 87A has two firm conditions. Both must be satisfied simultaneously.

Condition 1 — Residential Status: You must be a resident individual under Section 6 of the Income Tax Act. HUFs, firms, companies, and non-resident Indians cannot claim this rebate.

Condition 2 — Taxable Income Threshold:

| Tax Regime | Income Limit (FY 2025-26) | Maximum Rebate |

|---|---|---|

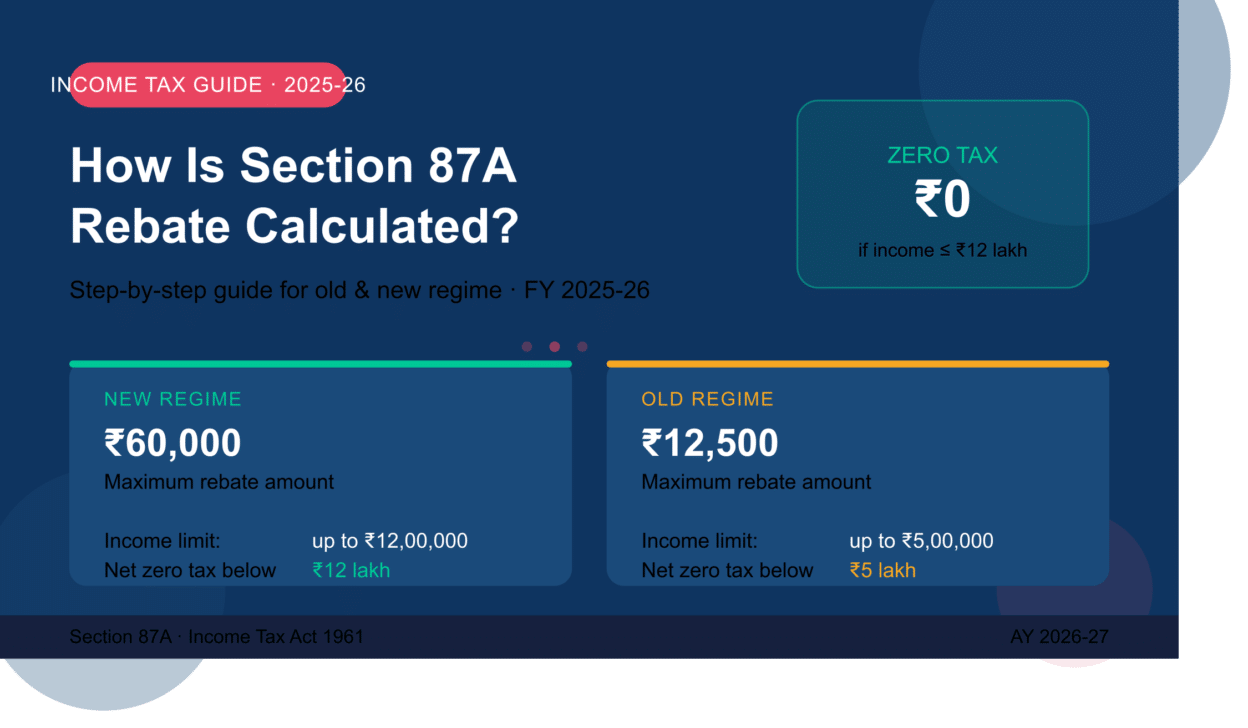

| New Tax Regime | Up to ₹12,00,000 | ₹60,000 |

| Old Tax Regime | Up to ₹5,00,000 | ₹12,500 |

The income limit applies to net taxable income — the figure you arrive at after all eligible deductions, not your gross salary or CTC.

What Counts as Taxable Income?

Your taxable income includes salary, rental income, business/profession income, and most capital gains. However, special rate capital gains — particularly long-term capital gains on listed equity under Section 112A — are excluded from the rebate calculation in the old regime. Under the new regime, Budget 2025 has aligned the treatment, but taxpayers with significant LTCG should verify their specific position with a CA before filing.

How Is Section 87A Rebate Calculated — Step-by-Step

The calculation follows a fixed sequence. Skipping or reordering steps leads to errors.

Step 1: Compute Gross Total Income

Add all income from all heads — salary (after standard deduction), house property, business/profession, capital gains, and other sources.

Step 2: Apply Deductions

Under the old regime: subtract deductions under Chapter VI-A (80C, 80D, 80G, etc.). Under the new regime: limited deductions apply (standard deduction of ₹75,000 for salaried individuals, employer NPS contribution under 80CCD(2)).

Step 3: Arrive at Net Taxable Income

This is the figure after Step 2. Compare it against the applicable threshold. If it exceeds the limit, Section 87A is not available — stop here.

Step 4: Calculate Tax as Per Slab Rates

Apply the income tax slab rates for your regime to your net taxable income.

Step 5: Apply the 87A Rebate

Subtract the rebate from the tax calculated in Step 4. The rebate is the lower of:

- The maximum rebate for your regime (₹60,000 or ₹12,500), or

- The actual tax payable

This ensures your tax liability does not go below zero.

Step 6: Add Cess

Apply 4% health and education cess on the tax after the rebate. If tax after rebate is zero, cess is also zero.

Calculation Example — New Regime (FY 2025-26)

Scenario: Salaried individual, Gross Salary ₹12,75,000

| Step | Amount |

|---|---|

| Gross Salary | ₹12,75,000 |

| Less: Standard Deduction | ₹75,000 |

| Net Taxable Income | ₹12,00,000 |

| Tax on ₹12,00,000 (as per new regime slabs) | ₹60,000 |

| Less: Rebate u/s 87A | ₹60,000 |

| Tax after rebate | ₹0 |

| Add: 4% Cess | ₹0 |

| Total Tax Payable | ₹0 |

Calculation Example — Old Regime (FY 2025-26)

Scenario: Individual with taxable income ₹4,80,000 after 80C deductions

| Step | Amount |

|---|---|

| Net Taxable Income | ₹4,80,000 |

| Tax on ₹4,80,000 (as per old regime slabs) | ₹11,500 |

| Less: Rebate u/s 87A | ₹11,500 |

| Tax after rebate | ₹0 |

| Add: 4% Cess | ₹0 |

| Total Tax Payable | ₹0 |

Note: The rebate is capped at actual tax payable. Since ₹11,500 is less than the ₹12,500 maximum, the full tax is offset.

Section 87A Under New Regime vs Old Regime — Key Differences

The 2025 Union Budget expanded the Section 87A benefit substantially under the new regime. Here is a direct comparison for FY 2025-26:

| Parameter | Old Tax Regime | New Tax Regime |

|---|---|---|

| Income threshold for rebate | ₹5,00,000 | ₹12,00,000 |

| Maximum rebate amount | ₹12,500 | ₹60,000 |

| Effective zero-tax income | Up to ₹5 lakh | Up to ₹12 lakh |

| Applicable to salaried | Yes | Yes (+ ₹75,000 std deduction) |

| Applicable to self-employed | Yes | Yes |

For most salaried individuals with income up to ₹12 lakh, the new regime now offers a substantially better outcome. A salaried person earning ₹12.75 lakh gross pays zero tax under the new regime after the standard deduction and the 87A rebate. Under the old regime, the same person would need to claim over ₹2.75 lakh in 80C and other deductions to achieve a comparable result.

Marginal Relief Under Section 87A — When Income Slightly Exceeds ₹12 Lakh

Budget 2025 also provides marginal relief to taxpayers whose income crosses the rebate threshold by a small amount. Without this relief, an individual earning ₹12,00,001 would owe tax on the entire ₹12,00,001 — a jump from zero to roughly ₹60,000 in tax, triggered by a single rupee of additional income.

Marginal relief ensures the additional tax you pay never exceeds the additional income you earned beyond the threshold.

Example: Individual with taxable income ₹12,50,000 under the new regime

- Tax on ₹12,50,000 (as per slabs) = ₹75,000

- Normal rebate under 87A = not available (income exceeds ₹12 lakh)

- Income above threshold = ₹50,000

- Marginal relief = Tax payable − excess income = ₹75,000 − ₹50,000 = ₹25,000 relief

- Effective tax after marginal relief = ₹50,000 (before cess)

The relief tapers off as income rises further above the threshold, eventually making it irrelevant.

Common Mistakes Taxpayers Make with Section 87A

Knowing the calculation is one thing. Applying it correctly during ITR filing is another.

Mistake 1 — Claiming 87A on special rate income in old regime: LTCG on equity (Section 112A) taxed at 10% cannot be offset by the 87A rebate under the old regime. The rebate applies only to tax computed on income chargeable at slab rates.

Mistake 2 — Comparing CTC to the income threshold: The ₹12 lakh limit is net taxable income after deductions, not your CTC or gross salary. Many people with a ₹13 lakh CTC actually have net taxable income below ₹12 lakh after the standard deduction.

Mistake 3 — Forgetting cess still applies to LTCG: If you have LTCG income but your slab-rate income qualifies for 87A, the cess on LTCG tax remains payable.

Mistake 4 — NRIs trying to claim the rebate: Section 87A is available only to resident individuals. Non-resident Indians cannot claim it regardless of income level.

Expert Perspective and Current Legal Position

The Central Board of Direct Taxes (CBDT) confirmed in Circular No. 01/2025 that the enhanced 87A rebate of ₹60,000 applies from Assessment Year 2026-27 (FY 2025-26), effective for ITRs filed from July 2025 onwards. This follows the Finance Act 2025 amending Section 87A.

The income tax department’s ITR utilities for AY 2026-27 have been updated to reflect the revised rebate computation. Taxpayers filing through the e-filing portal should ensure they are using the updated offline utility or the online filing portal dated post-April 2025 to get the correct rebate applied automatically.

The 87A rebate is particularly beneficial for first-time earners, those with fluctuating incomes, and individuals who recently crossed a tax bracket — groups that frequently overpay because they calculate tax without accounting for this relief.

Conclusion

Section 87A of the Income Tax Act 1961 is a straightforward but frequently overlooked tax rebate. For FY 2025-26, resident individuals with net taxable income up to ₹12 lakh under the new regime pay zero income tax — up from ₹7 lakh in the previous year. Under the old regime, the zero-tax limit remains at ₹5 lakh. The calculation requires six steps: compute gross income, apply deductions, arrive at taxable income, calculate tax on slabs, subtract the 87A rebate, and add cess. Marginal relief protects taxpayers whose income slightly crosses the threshold. The single most important check before filing your ITR is to compare your net taxable income — not your salary — against the relevant threshold.

Now it’s your turn. If you want a personalised calculation for your income, drop your question in the comments below or use the tax calculator linked in our tools section. If you found this guide useful, share it with someone who is filing their first ITR this year.

Frequently Asked Questions

Can I claim Section 87A rebate if I have capital gains income?

Under the new regime, the rebate applies to total income including most capital gains. Under the old regime, LTCG on listed equity (Section 112A) and STCG under Section 111A are excluded from the rebate.

Is the 87A rebate available on advance tax?

No. The 87A rebate is applied at the time of filing your ITR (or computing total tax liability), not at the time of advance tax payment.

What happens if I forget to claim the 87A rebate in my ITR?

You can file a revised return within the due date (typically 31 December of the assessment year) to claim the rebate. If the return is already processed, you may file a rectification request under Section 154.

Does the 87A rebate apply to senior citizens?

Yes. Senior citizens (60–79 years) and super senior citizens (80 years and above) who are resident individuals can claim the 87A rebate, subject to the same income thresholds.

How is Section 87A rebate calculated?

Section 87A rebate is calculated in six steps: (1) Compute gross total income, (2) Apply eligible deductions, (3) Arrive at net taxable income, (4) Calculate tax as per applicable slab rates, (5) Subtract the 87A rebate — the lower of the maximum rebate or actual tax payable, (6) Add 4% health and education cess on remaining tax. For FY 2025-26, the maximum rebate is ₹60,000 under the new regime (for income up to ₹12 lakh) and ₹12,500 under the old regime (for income up to ₹5 lakh).

Who is eligible for the tax rebate under Section 87A?

Resident individuals with net taxable income up to ₹12,00,000 under the new tax regime, or up to ₹5,00,000 under the old tax regime, are eligible for FY 2025-26. HUFs, firms, companies, and non-resident Indians cannot claim this rebate.

What is the maximum 87A rebate for FY 2025-26?

The maximum rebate under Section 87A is ₹60,000 under the new tax regime and ₹12,500 under the old tax regime for FY 2025-26 (AY 2026-27).

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.