If you want to know how to compute income tax on salary for the fiscal year 2025-26, this guide will walk you through the entire process step by step.. Most salaried employees in India know how much tax their employer deducts each month. What they often do not have is a clear picture of why that number is what it is — or whether it has been computed correctly.

Income tax on salary follows a defined process under the Income Tax Act 1961. Once the steps are clear, the calculation is straightforward. This guide walks through each one using a single real-world example so the numbers stay grounded throughout. If you prefer to skip the manual steps, you can use the free Income Tax Calculator on Finance and Tax Guide to compare both regimes instantly.

How to Calculate Income Tax on Salary: What You Need to Know First

Before working through the numbers, it helps to understand what counts as salary income for income tax purposes. Gross salary is broader than just the monthly figure credited to your bank account. Under the provisions of income tax law, it includes every monetary benefit received from an employer during the financial year.

A typical salary structure for a salaried employee in India includes:

- Basic Salary — Fully taxable, forms the base for other calculations

- House Rent Allowance (HRA) — Partially exempt if you are living in a rented house

- Leave Travel Allowance (LTA) — Exempt for actual domestic travel, twice in a four-year block

- Special Allowance — Fully taxable

- Performance Bonus — Fully taxable in the year it is received

- Employer’s PF Contribution — Exempt up to ₹7.5 lakh per year across PF, NPS, and gratuity combined

Some components reduce your tax burden directly; others do not. Understanding which is which is the first step in accurate tax calculation.

Real Example Used in This Guide: Arjun, Software Engineer, Pune

To keep the calculation concrete, this guide follows one person through every step.

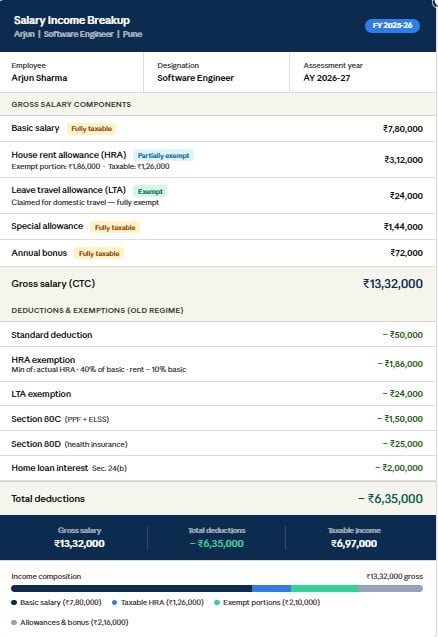

Arjun is 34 years old, works as a software engineer at a mid-sized IT company in Pune, and earns the following annual income for FY 2025-26:

| Salary Component | Annual Amount (Rs.) |

|---|---|

| Basic Salary | 7,80,000 |

| House Rent Allowance (HRA) | 3,12,000 |

| Leave Travel Allowance (LTA) | 24,000 |

| Special Allowance | 1,44,000 |

| Annual Bonus | 72,000 |

| Gross Salary | 13,32,000 |

Arjun lives in a rented flat in Pune and pays Rs. 22,000 per month in rent (Rs. 2,64,000 annually). He has an active home loan on a property in his hometown and makes regular investments in PPF and ELSS.

Step 1: Choose the Tax Regime

The first decision in how to calculate income tax on salary is choosing the right tax regime. For FY 2025-26, two options are available under the Income Tax Act 1961. For a full side-by-side breakdown, see the New vs Old Tax Regime comparison guide on this site.

New Tax Regime — Income Tax Slabs FY 2025-26

The new tax regime is now the default under Section 115BAC. It offers lower income tax slabs but does not allow most common deductions — no HRA exemption, no LTA, no Section 80C, and no home loan interest deduction under Section 24(b).

New Tax Regime — Income Tax Slabs for FY 2025-26:

| Annual Taxable Income | Tax Rate |

|---|---|

| Up to Rs. 4,00,000 | Nil |

| Rs. 4,00,001 – Rs. 8,00,000 | 5% |

| Rs. 8,00,001 – Rs. 12,00,000 | 10% |

| Rs. 12,00,001 – Rs. 16,00,000 | 15% |

| Rs. 16,00,001 – Rs. 20,00,000 | 20% |

| Rs. 20,00,001 – Rs. 24,00,000 | 25% |

| Above Rs. 24,00,000 | 30% |

What the new regime does allow for salaried employees:

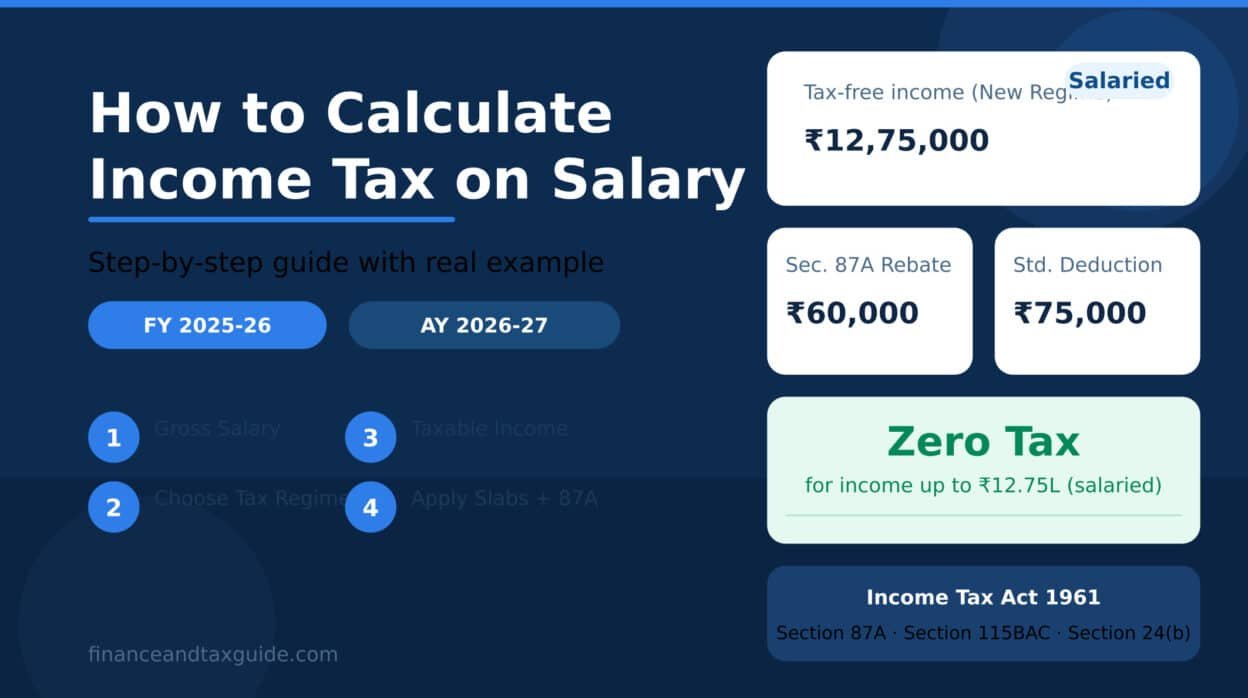

- Standard deduction of Rs. 75,000 (revised upward from Rs. 50,000 in FY 2024-25)

- Section 87A rebate up to Rs. 60,000 for taxable income up to Rs. 12,00,000

- Employer’s contribution to NPS under Section 80CCD(2)

Old Tax Regime — Income Tax Slabs FY 2025-26

The old tax regime carries higher slab rates but permits a range of deductions and exemptions. Taxpayers who claim HRA, have a home loan, invest in 80C instruments, or pay health insurance premiums often find the old regime more efficient despite the higher base rates.

Old Tax Regime — Income Tax Slabs for FY 2025-26 (Age below 60):

| Annual Taxable Income | Tax Rate |

|---|---|

| Up to Rs. 2,50,000 | Nil |

| Rs. 2,50,001 – Rs. 5,00,000 | 5% |

| Rs. 5,00,001 – Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

What the old regime allows:

- Standard deduction of Rs. 50,000

- HRA exemption (based on a three-point formula)

- Leave Travel Allowance (LTA) exemption

- Section 80C deductions up to Rs. 1,50,000

- Home loan interest deduction up to Rs. 2,00,000 under Section 24(b)

- Health insurance premiums under Section 80D

- Section 87A rebate up to Rs. 12,500 for taxable income up to Rs. 5,00,000

The right choice depends entirely on the numbers. Neither regime is universally better — the one that results in lower tax for a specific income and deduction profile is the right one for that year.

Step 2: Compute Your Taxable Income

Taxable income is gross salary minus all eligible deductions and exemptions. The figure differs under each regime because the old regime permits more reductions.

Taxable Income Under the New Tax Regime

Under the new regime, only the standard deduction applies for most salaried employees.

Gross Salary = Rs. 13,32,000

Less: Standard Deduction = Rs. 75,000

─────────────────────────────────────────────────

Taxable Income (New Regime) = Rs. 12,57,000Taxable Income Under the Old Tax Regime

The old regime involves more steps.

Calculating the HRA Exemption:

House rent allowance exemption is the lowest of these three figures:

- Actual HRA received from employer = Rs. 3,12,000

- 40% of Basic Salary (Pune is a non-metro city) = 40% of Rs. 7,80,000 = Rs. 3,12,000

- Rent Paid minus 10% of Basic Salary = Rs. 2,64,000 minus Rs. 78,000 = Rs. 1,86,000

The exempt HRA amount is Rs. 1,86,000.

Deductions Summary (Old Regime):

| Deduction | Applicable Section | Amount (Rs.) |

|---|---|---|

| Standard Deduction | — | 50,000 |

| HRA Exemption | — | 1,86,000 |

| LTA Exemption | — | 24,000 |

| PPF + ELSS Investment | Section 80C | 1,50,000 |

| Health Insurance Premium | Section 80D | 25,000 |

| Home Loan Interest | Section 24(b) | 2,00,000 |

| Total Deductions | 6,35,000 |

Gross Salary = Rs. 13,32,000

Less: Total Deductions = Rs. 6,35,000

─────────────────────────────────────────────────

Taxable Income (Old Regime) = Rs. 6,97,000Step 3: Apply the Income Tax Slabs and Calculate Tax

With taxable income established for both regimes, the next step is applying the slab rates to calculate the base tax amount.

New Tax Regime Tax Calculation (Taxable Income: ₹12,57,000)

| Income Slab | Rate | Tax (Rs.) |

|---|---|---|

| Up to Rs. 4,00,000 | Nil | 0 |

| Rs. 4,00,001 – Rs. 8,00,000 | 5% | 20,000 |

| Rs. 8,00,001 – Rs. 12,00,000 | 10% | 40,000 |

| Rs. 12,00,001 – Rs. 12,57,000 | 15% | 8,550 |

| Total Tax Before Cess | 68,550 |

Arjun’s taxable income of Rs. 12,57,000 exceeds Rs. 12,00,000, so the Section 87A rebate is not available here under the new regime. The rebate applies only when taxable income is up to Rs. 12,00,000.

Tax Before Cess = Rs. 68,550

Add: 4% Health and Education Cess = Rs. 2,742

─────────────────────────────────────────────────

Final Tax Liability (New Regime) = Rs. 71,292Old Tax Regime Tax Calculation (Taxable Income: ₹6,97,000)

| Income Slab | Rate | Tax (Rs.) |

|---|---|---|

| Up to Rs. 2,50,000 | Nil | 0 |

| Rs. 2,50,001 – Rs. 5,00,000 | 5% | 12,500 |

| Rs. 5,00,001 – Rs. 6,97,000 | 20% | 39,400 |

| Total Tax Before Cess | 51,900 |

Arjun’s taxable income of Rs. 6,97,000 is above Rs. 5,00,000, so the Section 87A rebate under the old regime — which applies only up to Rs. 5,00,000 — is not available either.

Tax Before Cess = Rs. 51,900

Add: 4% Health and Education Cess = Rs. 2,076

─────────────────────────────────────────────────

Final Tax Liability (Old Regime) = Rs. 53,976Final Comparison

| New Regime | Old Regime | |

|---|---|---|

| Gross Salary | Rs. 13,32,000 | Rs. 13,32,000 |

| Total Deductions | Rs. 75,000 | Rs. 6,35,000 |

| Taxable Income | Rs. 12,57,000 | Rs. 6,97,000 |

| Base Tax | Rs. 68,550 | Rs. 51,900 |

| Section 87A Rebate | Nil | Nil |

| 4% Cess | Rs. 2,742 | Rs. 2,076 |

| Final Tax | Rs. 71,292 | Rs. 53,976 |

For Arjun, the old tax regime saves roughly ₹17,300 in tax. His deductions of ₹6,35,000 reduce taxable income enough to overcome the old regime’s higher slab rates. This is a common outcome for salaried individuals with active home loans, HRA claims, and 80C investments. You can verify this result using the Income Tax Calculator for FY 2026-27 which compares both regimes side by side.

Step 4: Section 87A Rebate and How It Reduces Tax Liability

Section 87A of the Income Tax Act 1961 provides a direct rebate on computed tax — not a deduction from income. For FY 2025-26, the rebate limits are:

New Tax Regime: Rebate up to Rs. 60,000 for individuals with taxable income up to Rs. 12,00,000. This effectively makes income up to Rs. 12 lakh tax-free. For salaried employees who also claim the Rs. 75,000 standard deduction, a gross salary of up to Rs. 12,75,000 results in zero tax liability.

Old Tax Regime: Rebate up to Rs. 12,500 for individuals with taxable income up to Rs. 5,00,000.

In Arjun’s case, neither rebate applies because his taxable income exceeds the threshold under both regimes. But for someone earning a gross salary of Rs. 12,50,000, the Section 87A rebate under the new regime can eliminate the entire tax bill.

Marginal Relief Under Section 87A

When taxable income is just above the Rs. 12,00,000 rebate threshold under the new regime, a marginal relief provision prevents a disproportionate jump in tax. If taxable income is Rs. 12,20,000 — Rs. 20,000 above the threshold — the tax payable after marginal relief cannot exceed Rs. 20,000. This protects taxpayers from an outsized burden caused by crossing the limit by a small margin.

Add Cess and Check for Surcharge

Health and Education Cess

A flat 4% cess applies to the final tax amount for all taxpayers, after the Section 87A rebate. It funds health and education programmes and is non-negotiable regardless of income level.

Surcharge

Surcharge applies on the tax amount — not on income — for individuals with high annual income.

| Annual Income | Surcharge Rate |

|---|---|

| Up to Rs. 50,00,000 | Nil |

| Rs. 50,00,001 – Rs. 1,00,00,000 | 10% |

| Rs. 1,00,00,001 – Rs. 2,00,00,000 | 15% |

| Above Rs. 2,00,00,000 | 25% |

For the large majority of salaried individuals earning below ₹50 lakh annually, surcharge does not apply. For a complete picture of how TDS is deducted from salary and remitted, refer to the TDS TCS Master Table for FY 2026-27.

Deductions and Exemptions That Affect Your Income Tax on Salary

Understanding which deductions reduce taxable income — and under which regime — is central to knowing how to calculate income tax on salary correctly.

Deductions Available Under Both Regimes

- Standard Deduction — Rs. 75,000 (new regime) or Rs. 50,000 (old regime) for salaried individuals

- Section 80CCD(2) — Employer’s contribution to NPS (up to 10% of basic plus DA)

- Leave encashment on retirement — Exempt up to prescribed limits

Deductions Available Only Under the Old Regime

Section 80C covers a wide range of investments and expenses: contributions to PPF, EPF, and NPS; ELSS mutual fund investments; life insurance premiums; five-year tax-saving fixed deposits; and tuition fees paid for children. The combined limit is Rs. 1,50,000 per year.

House Rent Allowance (HRA) is exempt to the extent calculated using the three-factor formula — actual HRA received, 50% or 40% of basic salary depending on city, and rent paid minus 10% of basic salary. The lowest of the three is the exempt amount.

Home loan interest under Section 24(b) allows a deduction of up to Rs. 2,00,000 per year on interest paid for a self-occupied property. For a let-out property, the full interest is deductible, subject to an overall set-off limit of Rs. 2,00,000 against salary income.

Leave Travel Allowance (LTA) covers actual travel expenses for domestic journeys within India, for the employee and immediate family. The exemption applies twice in a block of four calendar years. Receipts must be submitted to the employer to claim the benefit.

Section 80D allows deduction of health insurance premiums — up to Rs. 25,000 for self, spouse, and children; an additional Rs. 25,000 (or Rs. 50,000 for senior citizens) for parents.

Section 80E provides a deduction on interest paid on an education loan with no upper cap. It applies for up to eight years from the year repayment begins.

How to Use an Income Tax Calculator for FY 2025-26

A salary calculator for FY 2025-26 is useful, but only as accurate as the data entered. Before using one, keep these figures ready:

- Gross salary broken into components — basic, HRA, LTA, special allowance, bonus

- Monthly rent paid and city of residence (for HRA exemption under old regime)

- 80C investments with exact amounts and instruments

- Home loan interest certificate from the lender showing principal and interest split

- Health insurance premium amounts for self and parents

- Any other annual income — savings account interest, FD interest, capital gains

The Finance and Tax Guide Income Tax Calculator computes taxable income under both regimes, applies the income tax slabs, factors in Section 87A where applicable, adds cess, and presents a clear comparison — for free.

What Changed in FY 2025-26 Compared to the Previous Year

The Union Budget 2025 introduced several changes applicable to salaried taxpayers from April 1, 2025. These form the basis of all calculations for FY 2025-26 (AY 2026-27):

| Parameter | FY 2024-25 | FY 2025-26 |

|---|---|---|

| Basic Exemption — New Regime | Rs. 3,00,000 | Rs. 4,00,000 |

| Standard Deduction — New Regime | Rs. 50,000 | Rs. 75,000 |

| Section 87A Rebate — New Regime | Rs. 25,000 (up to Rs. 7L income) | Rs. 60,000 (up to Rs. 12L income) |

| Effective Tax-Free Ceiling (Salaried) | Rs. 7,75,000 | Rs. 12,75,000 |

The Union Budget 2026 confirmed that these slab rates and benefits continue unchanged into FY 2026-27.

Practical Points That Affect Your Tax Calculation

Compare both regimes every year. Income, rent, investments, and loan balances change year to year. A regime that was optimal in a previous year may not be so now. This comparison takes under ten minutes using an income tax calculator.

HRA and landlord PAN requirement. Where annual rent exceeds ₹1,00,000, the landlord’s PAN must be submitted to the employer along with rent receipts. Without it, the HRA exemption is disallowed.

LTA requires travel documentation. Leave travel allowance is exempt only on submission of actual travel receipts. The benefit covers two domestic journeys in a four-year block. Unclaimed LTA is added to taxable income.

Use the final home loan certificate. Banks issue provisional certificates at the start of the year and final certificates after year-end. Always use the final certificate to ensure the correct home loan interest deduction is claimed.

Reconcile Form 26AS before filing. Check Form 26AS and the Annual Information Statement (AIS) to confirm that TDS deducted by the employer matches what is credited against your PAN. Discrepancies can delay refunds. If you spot a discrepancy, the Income Tax Portal rectification guide explains how to file a correction online.

Submit employer declaration on time. At the start of each financial year, employers ask employees to declare their regime preference and estimated deductions. A late or missing declaration results in the employer defaulting to the new regime for TDS. Submitting an accurate declaration keeps monthly TDS aligned with actual liability.

Frequently Asked Questions

Is gross salary of Rs. 12,75,000 really tax-free in FY 2025-26?

For salaried employees under the new tax regime, yes. The Rs. 75,000 standard deduction brings taxable income down to Rs. 12,00,000. The Section 87A rebate then eliminates the tax computed on that amount. The result is zero tax liability. This applies to salary income – special rate incomes such as short-term capital gains on equity are excluded from the Section 87A rebate.

Can the tax regime be changed each year?

Salaried employees without business income can switch regimes each financial year. The choice is made through a declaration to the employer at the start of the year or at the time of filing the income tax return. There is no restriction on switching annually.

What is the difference between gross salary and taxable income?

Gross salary is the total of all components received from the employer before any deductions. Taxable income is gross salary reduced by the standard deduction and applicable exemptions. Income tax slabs are applied to taxable income, not gross salary.

What happens when an employer deducts more TDS than the actual tax liability?

Excess TDS is claimed as a refund when the income tax return is filed. The refund is processed by the Income Tax Department and credited to the bank account registered with the tax portal.

Is there a tax benefit on home loan principal repayment?

Under the old tax regime, principal repayment qualifies as a deduction under Section 80C, within the Rs. 1,50,000 annual limit. Home loan interest is separately deductible under Section 24(b). Neither deduction is available under the new tax regime.

Summary: How to Calculate Income Tax on Salary for FY 2025-26

Calculating income tax on salary involves five steps: identify gross salary and its components, choose the applicable tax regime, compute taxable income by deducting eligible exemptions, apply the FY 2025-26 income tax slabs to arrive at base tax, check for the Section 87A rebate, and add the 4% health and education cess.

For FY 2025-26, the new tax regime is the default and has been substantially improved — a raised basic exemption of ₹4,00,000, a higher standard deduction of ₹75,000, and a Section 87A rebate covering incomes up to ₹12,00,000. Despite this, the old regime remains the better option for individuals with home loan interest, HRA, and active 80C investments — as Arjun’s example above demonstrates.

The right approach is to calculate your tax liability under both regimes using your actual income and deduction figures, compare the two outcomes, and choose accordingly. Use the free Income Tax Calculator to do this in under two minutes. For personalised guidance, consult a qualified Chartered Accountant or registered tax practitioner.

For personalised guidance, consult a qualified Chartered Accountant or registered tax practitioner.

Disclaimer: This article is for general informational purposes only. Tax laws are subject to change. Consult a qualified tax advisor for advice specific to your financial situation.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.