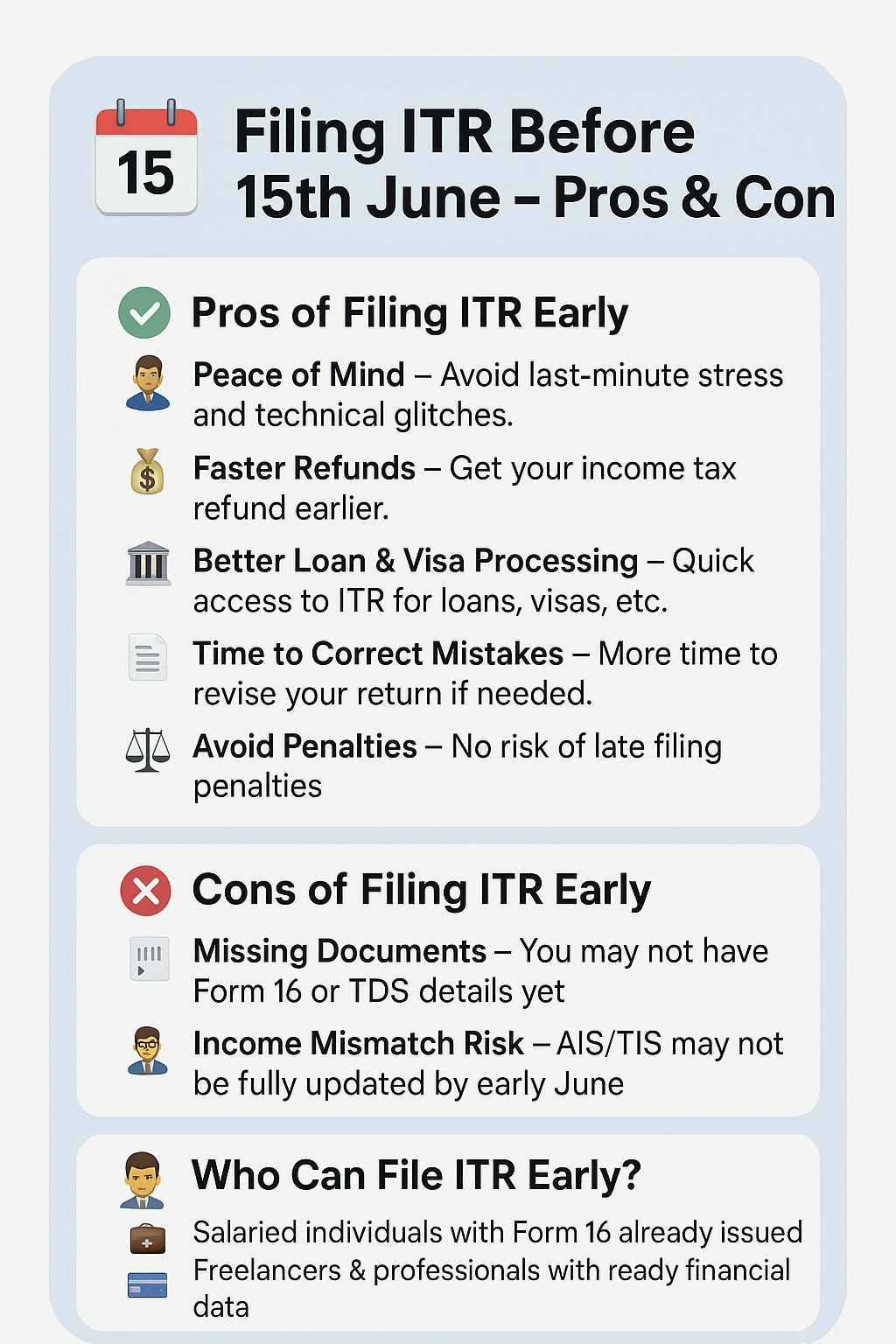

Why May 31 Is a Critical Financial Date for Every Indian Taxpayer

Every year, millions of Indian taxpayers scramble in the last days of July when the ITR filing deadline looms. But what most people don’t realize is that the real groundwork for a smooth, penalty-free tax filing begins in May itself — specifically before May 31. we’re going deep on the 3 financial things to do before May 31, along with a bonus reminder checklist and everything you need to know to stay compliant, save money, and avoid penalties. Whether you’re a salaried employee, a freelancer, an investor, or a business owner — this guide is for you.

Let’s break it all down.

Why May 31 Matters: The Financial Calendar You Need to Understand

India’s financial year runs from April 1 to March 31. The new financial year (FY 2025-26) has already begun, but many tasks from the previous financial year (FY 2024-25) are still pending.

May is the critical transition month. This is when:

Your employer files TDS returns and generates Form 16

The Income Tax Department updates the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS)

- Advance tax planning for Q1 begins

- Investment proof deadlines start approaching for the new FY

Miss this window and you’re looking at wrong ITRs, unverified returns, interest penalties on advance tax, and last-minute investment decisions made in panic. To stay ahead of all compliance deadlines year-round, bookmark our Complete Guide to Accounting in India 2026.

Here’s what you must do — right now, before May 31.

Task 1: File and Verify Your ITR (If Applicable)

What Is ITR and Why Does It Matter?

The Income Tax Return (ITR) is a form submitted to the Income Tax Department of India, declaring your income, deductions, and taxes paid for the previous financial year. Filing your ITR on time is not just a legal obligation — it’s a gateway to financial credibility.

Your ITR is needed for:

- Loan approvals (home loan, car loan, personal loan)

- Visa applications to foreign countries

- Claiming tax refunds

- Carrying forward capital loss to future years

- Government tenders and contracts

When Should You File?

The general deadline for non-audit taxpayers is July 31 of the assessment year. But the earlier you file, the better — especially if you’re expecting a refund. May is the perfect time to start preparing, so your July filing is smooth and error-free.

Step-by-Step: How to Check AIS and TIS Before Filing

This is the most important pre-filing step that most taxpayers skip — and it costs them dearly.

What is AIS?

The Annual Information Statement (AIS) is a comprehensive document available on the Income Tax e-filing portal that shows all financial transactions reported against your PAN — salary, interest income, dividends, mutual fund transactions, property purchases, foreign remittances, and more.

What is TIS?

The Taxpayer Information Summary (TIS) is a simplified version of AIS that provides category- wise processed values for ease of filing.

How to Check Your AIS/TIS:

1. Log in to incometax.gov.in

2. Go to “Annual Information Statement (AIS)” under the Services tab

3. Download both AIS and TIS in PDF or JSON format

4. Cross-check every entry against your actual income sources

What to look for:

- Salary income: Match with your employer’s salary slips and Form 16

- Interest income: Check savings account interest, FD interest, and RD interest

Capital gains: Match with your broker’s P&L statement

Capital gains: Match with your broker’s P&L statement - Dividends: Cross-verify with your Demat account statements

- Property transactions: Verify any buying/selling of immovable property Foreign income: If applicable, check DTAA provisions

Common AIS Errors and What to Do:

If you find incorrect or missing information in your AIS, you can submit feedback directly on the portal by clicking the “Optional” feedback button next to each transaction. The department will review it, and the corrected data will reflect in your TIS.

Don’t rush your filing based on incorrect AIS data — this is one of the biggest mistakes taxpayers make.

Match Salary, Interest, and Capital Gains

After checking your AIS, match the figures with:

- Form 16 Part A (TDS deducted by employer) — available from your HR/finance department by mid-June

- Form 16 Part B (Salary breakup and deductions) — provided by your employer

- Bank statements for interest income

- Capital Gains Statement from your broker (Zerodha, Groww, Angel One, etc.)

- Mutual Fund CAS (Consolidated Account Statement) from CAMS or KFintech

ITR Verification: The Step Most People Forget

This is critical: Filing your ITR is NOT enough. You MUST verify it. An unverified ITR is treated as if it was never filed. This means:

- No refund processing

- No carry-forward of losses

- Potential notice from the Income Tax Department

How to verify your ITR:

- E-verify via Aadhaar OTP (fastest and most recommended) Net banking e-verification

- Bank ATM-based verification

- Demat account-based verification

- Physical signed ITR-V sent to CPC Bengaluru by post (last resort).

Deadline for verification: 30 days from the date of filing.

⚠ Wrong or unverified ITR = NOT valid filing. Period.

Task 2: Complete Your Investment Proof Planning

Why Plan Investments in May for the New Financial Year?

FY 2025-26 has just begun. You have the entire year ahead of you. So why plan investments now? Because last-minute investments = poor decisions.

Every year, lakhs of taxpayers invest blindly in January-March just to save taxes, without

understanding what they’re investing in. They end up locking money in wrong products, missing better options, or making sub-optimal choices under time pressure.

May is the ideal time to:

- Review last year’s investment performance

- Understand your tax liability for the current year

- Plan your deductions systematically, m

- Start SIPs early to benefit from rupee cos

Tax-Saving Sections to Plan

Section 80C – Up to ₹1.5 Lakh Deduction

Section 80C is the most popular tax-saving provision that qualify :

- ELSS (Equity Linked Savings Scheme) — Best for wealth creation with 3-year lock-in

- PPF (Public Provident Fund) — Safe, 15-year lock-in, tax-free returns

- EPF (Employee Provident Fund) — Auto-deducted for salaried; employer contribution also qualifies

- NSC (National Savings Certificate) — Post office scheme, 5-year lock-in

- Tax-Saving FD — 5-year lock-in, interest taxable

- ULIP (Unit Linked Insurance Plan) — Market-linked + insurance

- Sukanya Samriddhi Yojana — For parents with daughters below 10 years

- Home Loan Principal Repayment — Principal component qualifies under 80C

- Tuition Fees — For up to 2 children

Pro Tip: Start your ELSS SIP from May itself. If you invest ₹12,500/month, you complete your ₹1.5 lakh 80C target by March — without any last-minute rush.

Section 80D — Health Insurance Premium (Up to ₹1 Lakh)

Health insurance is not just a tax-saving tool — it’s essential financial protection. Section 80D allows:

- Up to ₹25,000 deduction for self, spouse, and children’s health insurance premium

- Additional ₹25,000 for parents’ health insurance (up to ₹50,000 if parents are senior citizens)

- ₹5,000 for preventive health check-ups within the above limits

Action point for May: Review your existing health insurance policy. Is the coverage adequate? Did you pay the premium for FY 2025-26? Ensure you have your premium receipt.

NPS — National Pension System (Additional ₹50,000 Under 80CCD(1B))

Over and above the 80C limit, you can claim an additional ₹50,000 deduction under Section 80CCD(1B) by investing in NPS (National Pension System).

This is one of the most under-utilized deductions in India. Start your NPS contribution in May to spread it across the year.

ELSS and SIP Alignment

Review your existing SIP portfolio:

- Are your funds performing well against their benchmark?

- Are your SIPs aligned with your financial goals?

- Are you investing in old, underperforming ELSS funds just for tax saving?

May is the time to course-correct. Switch to better funds if needed, set up new SIPs, and align your investment calendar with your tax-saving goals.

Investment Proof Planning Checklist for May

Here’s a practical checklist to complete this month:

- Review last year’s 80C investments and their performance

Set up ELSS SIP for FY 2025-26 (if not already done)

Set up ELSS SIP for FY 2025-26 (if not already done) - Renew health insurance policy for FY 2025-26

- Check NPS balance and plan monthly contributions

- Review PPF passbook and plan annual contribution

- Check if home loan EMI breakup is available for principal + interest claim

- Note tuition fees paid for children’s education

Task 3: Check Your Advance Tax Liability

What Is Advance Tax?

Advance tax is the payment of income tax in installments during the financial year itself, instead of paying it all at the end of the year. It is applicable if your estimated tax liability for the year exceeds ₹10,000 after TDS.

In simple terms: the government wants its share of your tax throughout the year — not just at the end.

Who Needs to Pay Advance Tax?

Most salaried employees whose TDS is deducted by their employer don’t need to worry much about advance tax. But if you have additional income beyond your salary, you likely need to pay advance tax. This includes:

- F&O (Futures & Options) income — Treated as business income

- Intraday trading income — Speculative business income

- Freelance or consulting income — Professional income

- Rental income — After standard deduction

- Capital gains — Short-term and long-term gains from stocks, mutual funds, or property

- Dividend income — Taxable above ₹5,000 from a company

- Interest income — FD interest, savings account interest beyond ₹10,000

Advance Tax Due Dates for FY 2025–26

| Installment | Due Date | % of Total Tax to Be Paid |

| 1st | June 15, 2025 | 15% |

| 2nd | September 15, 2025 | 45% (cumulative) |

| 3rd | December 15, 2025 | 75% (cumulative) |

| 4th | March 15, 2026 | 100% (cumulative) |

Note: Senior citizens (above 60 years) who don’t have business income are exempt from paying advance tax.

Why You Must Check Advance Tax Liability Before May 31

The first advance tax installment is due on June 15. You have very little time between June 1 and June 15 to estimate your income, calculate tax, and make the payment.

If you start calculating in May, you can:

- Estimate your total income for FY 2025-26 accurately

- Factor in expected capital gains, freelance income, rent, etc.

- Subtract expected TDS deductions

- Calculate 15% of the net tax liability

- Pay by June 15 without stress

Penalty for Not Paying Advance Tax

If you fail to pay advance tax on time, you’ll attract interest under:

- Section 234B — Interest at 1% per month for default in advance tax payment

- Section 234C — Interest at 1% per month for deferment of each installment

These interest charges add up quickly and can result in significant extra outflow — money that could have stayed in your pocket.

⚠ Missing advance tax = interest penalty later. There’s no escaping it.

How to Calculate and Pay Advance Tax

- Step 1: Estimate your gross total income for the full year from all sources

- Step 2: Subtract standard deduction (₹75,000 for salaried in new regime or ₹50,000 in old regime) and other deductions

- Step 3: Calculate income tax as per the applicable tax slab (old or new regime)

- Step 4: Subtract TDS already deducted or likey to be deducted

- Step 5: If balance tax > ₹10,000, you must pay advance tax

- Step 6: Pay 15% of the amount calculated above before June 15

How to Pay: Log in to incometax.gov.in → e-Pay Tax→Select Challan 280 → Select “(0021) Income Tax (Other than Companies)” → Payment mode (net banking/debit card/UPI) → Enteramount and pay

Bonus Reminder: 3 More Things to Do in May

Beyond the three main tasks, here are three bonus actions to complete before May 31:

1. Update Your Bank Account Details on the Income Tax Port

Your tax refund is processed directly to your bank account. An ou account will delay your refund — sometimes by months.

Action: Log in to incometax.gov.in → Profile → My Bank Account → Ve account is correct and pre-validated.

2. Download Your AIS Statement

Even if you’ve already checked your AIS online, download a PDF copy for yo helps when:

- You need to respond to an income tax notice

- You’re filling in details in your ITR

- You’re verifying transactions with your financial advisor

3. Check Form 26AS Equivalent Summary

Form 26AS is the tax credit statement that shows all TDS deducted against your PAN, advancetax paid, self-assessment tax paid, and high-value transactions.

With the introduction of AIS, Form 26AS has been simplified — but it’s still a critical document.Ensure that:

- All TDS entries match what your employer/bank/payer has deducted

- Advance tax payments made earlier are reflected

- Any discrepancy is reported and resolved before filing

Old Tax Regime vs New Tax Regime: Which to Choose for FY 2025-26?

Since Budget 2025, the new tax regime has been made even more attractive with revised slabs and a higher standard deduction of ₹75,000. Here’s a quick comparison:

New Tax Regime Slabs (FY 2025–26)

| Income Range | Tax Rate |

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 to ₹7,00,000 | 5% |

| ₹7,00,001 to ₹10,00,000 | 10% |

| ₹10,00,001 to ₹12,00,000 | 15% |

| ₹12,00,001 to ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

Tax rebate under Section 87A: Up to ₹60,000 rebate if income is ≤ ₹12,00,000 in the new regime — effectively making income up to ₹12 lakh tax-free.

Old Tax Regime — Still Worth It?

The old regime makes sense if your deductions (80C + 80D + HRA + home loan interest + NPS,etc.) exceed approximately ₹3.75 lakh or more. Otherwise, the new regime is generally better.

Pro Tip: Use an online tax calculator or consult a tax professional to determine which regimesaves you more tax based on your specific situation.

Common Mistakes to Avoid in May

Here are the top mistakes Indian taxpayers make in May — and how to avoid them:

Mistake 1: Assuming your AIS is always correct

AIS is populated based on data reported by third parties (banks, employers, brokers). Errors are common. Always verify before filing.

Mistake 2: Not verifying the ITR after filing

Thousands of taxpayers file their return but forget to verify it. An unverified ITR = invalid return.

Mistake 3: Waiting until July to start investment planning

If you start your 80C investments in January-March, you miss 9 months of returns. Start in April- May for maximum benefit.

Mistake 4: Ignoring advance tax if you have freelance/F&O income

Many freelancers and traders think “I’ll pay everything in March.” That costs them 1% interest per month in penalties.

Mistake 5: Not updating bank details before filing

An invalid bank account means your refund bounces and gets stuck in processing for months.

Frequently Asked Questions (FAQ)

Is it mandatory to file ITR before May 31?

No, the general ITR filing deadline for individuals is July 31 of the assessment year. However, May 31 is important for completing preparatory steps — verifying AIS/TIS, collecting Form 16, and ensuring your ITR is error-free when you file.

What happens if I don’t verify my ITR?

If you don’t verify your ITR within 30 days of filing, it is treated as if you never filed. You may face penalties, lose refunds, and lose the right to carry forward losses.

Can I change from old to new tax regime every year?

Salaried individuals and non-business taxpayers can switch between old and new regime every year. However, taxpayers with business income can only switch once from the old to the new regime.

Who is required to pay advance tax?

Any taxpayer whose estimated tax liability for the year (after TDS) exceeds ₹10,000 is requiredto pay advance tax. This typically includes those with freelance income, capital gains, F&O trading profits, or rental income.

What is the penalty for not paying advance tax?

You will be charged interest under Section 234B (1% per month for non-payment) and Section 234C (1% per month for deferment of each installment).

How do I check my advance tax liability?

Log in to the Income Tax e-filing portal → Services → Challan Status. Or calculate it manually by estimating your annual income from all sources, computing tax, and subtracting TDS already deducted.

What is AIS and how is it different from Form 26AS?

AIS (Annual Information Statement) is a comprehensive statement of all financial transactions linked to your PAN, including purchases, sales, dividends, and interest. Form 26AS is a tax credit statement showing TDS/TCS deducted and taxes paid. AIS is more detailed and has largely supplemented Form 26AS.

What if I find wrong information in my AIS?

You can submit feedback directly on the AIS portal. Select the incorrect transaction, click “Optional” feedback, and explain the discrepancy. The system updates TIS accordingly.

Should I invest in ELSS or PPF for 80C?

It depends on your risk appetite and liquidity needs. ELSS has a 3-year lock-in and is market- linked (higher return potential). PPF has a 15-year lock-in but offers guaranteed, tax-free returns. A combination of both works well for most investors.

What documents should I keep ready for ITR filing?

1. Form 16 (from employer)

2. Bank statements (all accounts)

3. AIS / TIS printout

4. Capital gains statement from broker

5. Mutual fund CAS from CAMS/KFintech

6. Home loan statement (interest + principal breakup) ![]()

7. Health insurance premium receipt

8. Rent receipts (if claiming HRA)

9. Investment proofs for 80C, 80D, NPS

Conclusion: Don’t Wait for the Last Minute

The Indian tax system rewards those who plan ahead and penalizes those who procrastinate. May is your window of opportunity to get your financial house in order — before the deadlinespile up in June and July.

To recap, here are the 3 things you must do before May 31:

- 1. File/Verify your ITR (if already filed) and check your AIS/TIS meticulously

- 2. Plan your investment proofs for FY 2025-26 — 80C, 80D, NPS, ELSS/SIP

- 3. Calculate your advance tax liability and be ready for the June 15 deadline

And don’t forget the bonus reminders:

- Update your bank details on the income tax portal

- Download your AIS statement

- Check your Form 26AS

May end = financial cleanup time, not planning time.

If you found this guide helpful, share it with your friends, family, and colleagues who mightbenefit. And don’t forget to subscribe to our YouTube channel — Finance And Tax Guide —where we break down complex tax and finance topics into simple, actionable content everyweek.

Disclaimer: This blog post is for educational and informational purposes only. It does notconstitute professional tax or financial advice. Please consult a qualified Chartered Accountant ortax professional for advice specific to your situation.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.