After decades of debate, countless committees, and navigating a labyrinth of expectations, the Direct Tax Code (DTC) 2025 is now law. The new Income-tax Bill, 2025, which replaces the six-decade-old Income Tax Act, 1961, received Presidential assent in August 2025.

This is not a simple amendment. It is not an extension of the old rules. It is a complete, ground-up replacement of India’s entire direct tax framework.

For over 60 years, Indian businesses have operated under the 1961 Act, a law so amended, patched, and complicated by circulars, notifications, and legal precedents that it became a symbol of complexity. Today, that era is over.

The new Code is designed to be a “charter for the 21st-century Indian economy,” built on the principles of simplicity and transparency. But with this simplicity comes a radical shift in how your business will calculate profits, pay taxes, and ensure compliance.

What does this mean for you, today? It means the strategies that worked last year might be obsolete next year. It means the deductions you’ve planned for are likely gone. It means your compliance model needs an immediate and total review.

This article is not a simple summary. It is a comprehensive business-first guide to the Direct Tax Code 2025, what it means, why it’s here, and the immediate strategic actions you must consider.

The Dawn of a New Tax Era: Why the Direct Tax Code 2025 Replaces the 1961 Act

To understand where we are going, we must first understand the journey. The replacement of the 1961 Act wasn’t just a “good idea”; it became an economic necessity.

The Problem with the Past: What Was Wrong with the Income Tax Act, 1961?

The 1961 Act was a law of a different India—a closed, pre-liberalization economy. As India grew, the Act was stretched to its limits, creating a system that was, by all accounts, broken.

Decades of Amendments and Complexity

The original Act was relatively straightforward. But over 60+ years, successive governments used annual Finance Acts to add, delete, and modify sections. This resulted in a legal behemoth of over 700 sections and countless subsections, many of which contradicted each other. For a business owner, getting a simple answer was often impossible without expert (and expensive) legal opinion.

Ambiguity and High Litigation

This complexity bred ambiguity. Vague language and conflicting provisions meant that taxpayers and the tax department often had vastly different interpretations of the same law. The result? India’s tax dispute system became one of the most clogged in the world, with trillions of rupees locked in litigation. This created an environment of “tax uncertainty,” the single biggest enemy of business investment and long-term planning.

The Core Philosophy of the DTC 2025: Simplification, Transparency, and Compliance

The Direct Tax Code 2025 is a direct response to these problems. Its core philosophy isn’t just to collect tax, but to change the very relationship between the taxpayer and the government.

Broadening the Tax Base

The old Act was a fortress of exemptions and deductions. You could have high “book profits” (what you tell your shareholders) but low “taxable profits” (what you tell the IT department). The new Code attacks this disconnect. Its guiding principle is: “Lower tax rates, but fewer (or no) exemptions.” By removing these deductions, the Code forces more of a company’s real income onto the tax rolls, “broadening the tax base.”

Aligning with Global Standards

The 1961 Act was out of step with global tax practices. The DTC 2025 incorporates international best practices, such as revised rules for non-resident taxation (like the Branch Profits Tax) and clear General Anti-Avoidance Rules (GAAR), making India a more predictable and competitive place for foreign investment.

Is It Official? Yes, the Income-tax Bill, 2025 is Now Law

Let’s be perfectly clear: this is not a draft.

Understanding the Timeline: From Bill to Assent (August 2025)

The new Income-tax Bill, 2025, was passed by Parliament and received the assent of the President of India in August 2025. It is now officially on the statute books.

When Does It Apply? Expected Applicability from FY 2026-27

This is the most critical question for your business. The new Code is law, but it will be effective from April 1, 2026. This means it will apply to income earned in the Financial Year 2026-27 (which you will file returns for in Assessment Year 2027-28).Key Takeaway for Businesses: You are currently in FY 2025-26, which is the last financial year to be governed by the old Income Tax Act, 1961. This gives you a precious, limited window of just over one financial year to restructure your business, update your software, and prepare for a completely new system. The planning must start today.

The Big 10: Key Changes Every Indian Business Must Understand

The Direct Tax Code 2025 is not a minor update; it’s a new operating system. We have analyzed the new law, and here are the 10 most profound changes that will impact your business, your strategy, and your bottom line, starting from FY 2026-27.

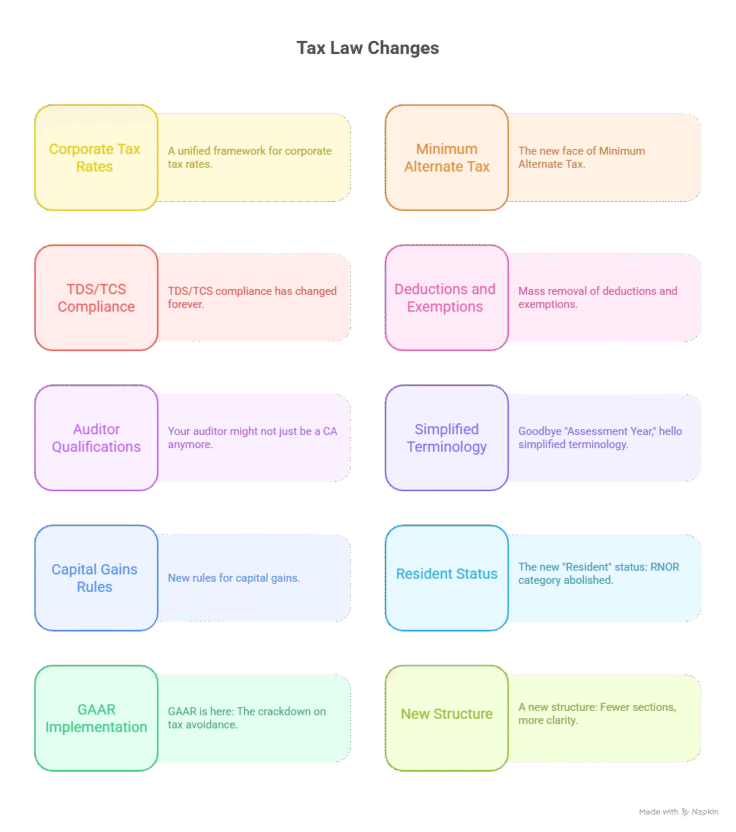

1. Corporate Tax Rates: A Unified Framework

The most significant headline is the move towards a single, unified corporate tax rate, set at 30% for all companies, domestic or foreign, on their net taxable income.

This replaces the old, complex system of different rates for domestic companies (with or without opting for special regimes like 115BAA) and foreign companies.

The New Simplicity: 30% Standard Rate

The goal is to remove ambiguity. The 30% rate is the new standard. This simplifies financial modeling and investment projections. The era of choosing between multiple “regimes” (like the 22% and 15% optional rates) is over, as those have been subsumed into this new, unified structure.

Impact on New Manufacturing Units

Businesses that previously enjoyed the 15% concessional rate under Section 115BAB will need to re-evaluate their tax projections. The new 30% rate applies to all, but this is balanced by the removal of MAT (see point 2) and simplified compliance.

Understanding the Branch Profits Tax (BPT) for Foreign Companies

While the corporate tax rate is 30% for foreign companies (down from 40% in the old regime), the DTC 2025 introduces a Branch Profits Tax (BPT) of 15%. This tax is levied on the profits of a foreign company’s Indian branch after the 30% corporate tax has been paid, specifically on profits that are deemed “repatriated” or sent back to the foreign head office. This aligns India’s tax law with global standards and is a critical new calculation for all MNCs operating in India.

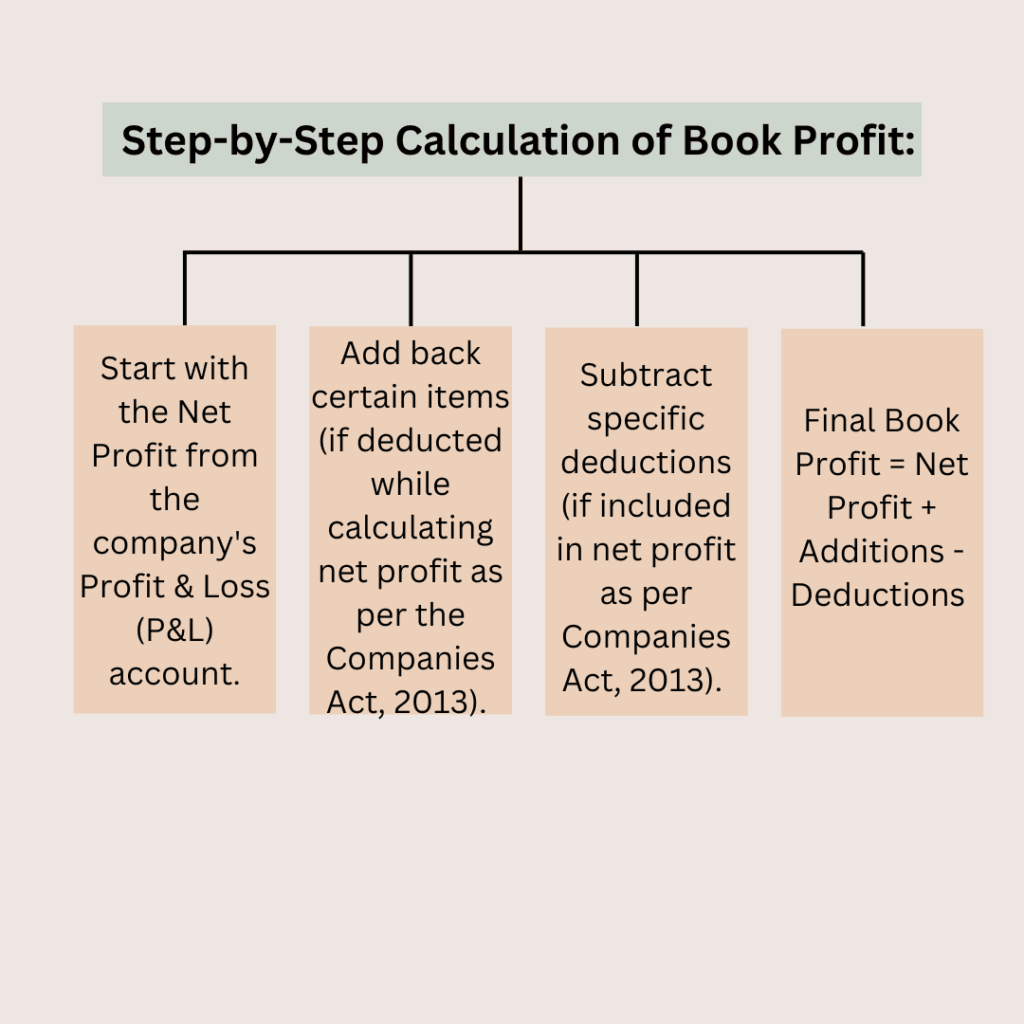

2. The New Face of MAT (Minimum Alternate Tax)

For decades, MAT was the government’s safety net, forcing profitable companies with high “book profits” but low “taxable income” (due to deductions) to pay a minimum tax (around 15%) on their book profits.

The DTC 2025 fundamentally alters this concept.

How the MAT Framework is Revised

MAT is not “abolished,” but its application is drastically changed. The new Code is built on the principle of removing deductions. With few deductions left, the gap between book profit and taxable profit will narrow dramatically. Therefore, the old form of MAT is no longer necessary for most companies.

The Big Relief: No MAT for Most Companies

The new Code is clear: companies paying the standard 30% corporate tax are no longer subject to MAT. This is a massive relief, especially for infrastructure and capital-intensive industries that were often caught by MAT provisions despite having low taxable income due to high depreciation. It ends the “tax on tax” confusion and significantly improves cash flow. The concept will only remain for very specific, niche sectors that still retain special exemptions.

3. TDS/TCS Compliance Just Changed Forever

This is perhaps the most significant operational change for every single business. The DTC 2025 has fully “rationalized” the Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) systems, aiming to reduce compliance load and improve cash flow.

Drastic Rate Reductions: The New 2% and 0.1% Rules

The labyrinth of 30+ different TDS rates (1%, 2%, 5%, 10%, 20%, 30%) is gone. It has been replaced by a few simple, low-rate “buckets.”

Most payments to vendors, contractors, and for professional services will now attract a standard TDS rate of 2% (down from 5% or 10%).

This is a massive win for service providers (consultants, agencies, freelancers) whose cash flow was perpetually locked up in TDS credits.

A Win for E-commerce: Unpacking the 0.1% TDS for Operators

The DTC 2025 directly addresses the pain points of the digital economy. The old 1% TDS (under 194-O) for e-commerce operators and the 5% for participants were complex.

The new law slashes the TDS rate for e-commerce operators to a very low 0.1%.

Simultaneously, the conflicting TCS provision (Sec 206C(1H)) on the sale of goods is removed, ending the “TDS vs. TCS” overlap that plagued digital platforms. This is a clear, simple, and pro-business move.

Simplified Compliance or More Reporting?

The trade-off for these low rates is the expectation of flawless reporting. The new system is built for data matching. While the rates are lower, the penalties for non-compliance (failure to deduct or file) will be stringent. Your accounting software must be ready for this.

4. The End of an Era: Mass Removal of Deductions and Exemptions

This is the “grand bargain” of the Direct Tax Code 2025: lower rates and no MAT in exchange for no deductions.

Why are deductions being removed?

The 1961 Act was clogged with hundreds of exemptions and deductions (e.g., for SEZs, new investments, R&D, skill development) that made the law complex and led to litigation. The new Code’s philosophy is that a business’s “taxable profit” should be as close as possible to its “real profit.”

Which business deductions are gone?

Nearly all of them. The entire Chapter VI-A (which included 80-IA, 80-IB, etc.) is gone. Special deductions for specific sectors, accelerated depreciation (beyond the normal block), and various investment-linked exemptions have been removed from the Code.

Strategic Shift: From ‘Tax Savings’ to ‘Tax Compliance’

This is a profound strategic shift. Your company’s finance department must move its focus from “tax planning” (finding deductions) to “tax compliance” (ensuring accurate reporting). The new game is about business efficiency, not tax breaks.

5. Your Auditor Might Not Just Be a CA Anymore

This is a seismic shift in the professional landscape. For 60 years, the term “tax auditor” was synonymous with “Chartered Accountant (CA).”

Not anymore.

Expansion of Tax Audit Roles

The DTC 2025 officially expands the definition of “Accountant” who can perform a tax audit under the new Code.

Company Secretaries (CS) and Cost Accountants (CMA) as Tax Auditors

The new law explicitly empowers practicing Company Secretaries (CS) and Cost and Management Accountants (CMA) to conduct tax audits and issue tax audit reports, a role previously reserved exclusively for CAs.

What this means for your business’s audit process

This move is designed to widen the pool of available professionals, potentially reducing audit costs and providing businesses with more choice. Your business can now engage a CS or CMA for your tax audit, bringing a different perspective (corporate governance from a CS, cost efficiency from a CMA) to the audit process.

6. Simplified Terminology: Goodbye “Assessment Year”

This is a simple change that makes life easier for everyone. The DTC 2025 eliminates the confusing dual-year system.

Understanding the “Tax Year” (or “Financial Year”) Concept

The old system required you to track two years:

- Financial Year (FY): The year you earn income (e.g., April 1, 2024 – March 31, 2025).

- Assessment Year (AY): The year you file and are assessed for that income (e.g., April 1, 2025 – March 31, 2026).

This FY/AY confusion is gone. The new Code uses one single term: “Tax Year” (or simply “Financial Year”).

How this simplifies filing and reporting

You will now file your return for the “Tax Year 2026-27” (income earned from April 1, 2026, to March 31, 2027). This is simple, intuitive, and aligns with global standards. It removes a major source of clerical errors in tax filings.

7. New Rules for Capital Gains

The DTC 2025 completely overhauls the taxation of capital gains, a move that will affect every investment your business makes.

How Capital Gains are taxed under DTC 2025

The old system of different rates and holding periods for “short-term” vs. “long-term” (and for different assets like equity, property, etc.) is abolished.

The new rule is shockingly simple: All capital gains are now to be treated as regular “Business Income” and will be taxed at your standard 30% corporate tax rate.

Changes in holding periods and rates

Since the distinction is gone, the concepts of “holding periods” (12, 24, 36 months) are no longer relevant for calculating the tax rate. This simplifies calculation but also means that “long-term” gains (e.g., from property or equity held for years) will now face a much higher tax (30%) than before (10% or 20% with indexation). This requires a complete re-evaluation of your company’s investment strategy.

8. The New “Resident” Status: RNOR Category Abolished

The DTC 2025 simplifies how a person’s or entity’s tax residency is determined, a critical factor for MNCs, expats, and directors.

Simple Classification: Resident vs. Non-Resident

The ambiguous, “in-between” category of “Resident but Not Ordinarily Resident” (RNOR) has been completely abolished. This status, which offered a significant tax shield on global income for returning Indians, is gone.

Under the new Code, you are either a “Resident” (taxable on global income) or a “Non-Resident” (taxable only on Indian-sourced income). The criteria for determining this are now clearer and more stringent.

Impact on Directors, Expats, and Global Income

This change has major implications. Returning Indian professionals who previously relied on RNOR status will find their global income immediately taxable. Foreign directors and expats will need to be extremely careful about the number of days they spend in India, as the “Resident” classification now has more significant financial consequences.

9. GAAR is Here to Stay: The Crackdown on Tax Avoidance

While the old Act had GAAR (General Anti-Avoidance Rules), the DTC 2025 gives it new prominence and power, solidifying it as a central tool for the tax department.

What are the General Anti-Avoidance Rules (GAAR)?

GAAR are “catch-all” provisions that allow tax authorities to disregard any business transaction or arrangement if its primary purpose is to obtain a tax benefit, even if it’s technically legal.

How will authorities determine ‘tax avoidance’?

The key test is “commercial substance.” If your business sets up a complex web of shell companies in a tax haven to route profits, and that structure has no real business purpose (no employees, no operations), GAAR can be invoked. The tax department can ignore the structure and tax the income as if the transaction never happened.

The message is clear: Business strategies must be driven by commercial logic, not just tax avoidance.

10. A New Structure: Fewer Sections, More Clarity

Finally, the new Code itself is a structural revolution.

From 700+ Sections to ~300: A Simpler Bill

The 1961 Income Tax Act had grown into a monster of 700+ sections, plus thousands of sub-sections, clauses, and schedules. It was unreadable.

The new Direct Tax Code 2025 is a lean document, with only around 319 sections and 22 schedules.

How this reduces legal ambiguity

By removing decades of layered amendments and rewriting the law in plain, modern language, the DTC aims to drastically reduce ambiguity. Clearer definitions and a logical structure mean less room for interpretation, which in turn should lead to fewer disputes and less litigation. It’s a foundational step towards tax certainty.

Strategic Planning for Businesses: How to Prepare for the DTC 2025 Transition

Knowing the “Big 10” changes is the first step. The next is applying that knowledge. With the DTC 2025 becoming effective from April 1, 2026 (for FY 2026-27), you have a limited window to prepare.

The impact of the Code is not uniform. A startup’s priorities will be vastly different from a multinational corporation’s. Here is a strategic breakdown by business type.

For Startups and MSMEs: A Focus on Cash Flow and Simplicity

For small and medium businesses, the new Code is a double-edged sword: it brings incredible simplification but demands you let go of old habits.

Re-evaluate Your Cash Flow Immediately

This is your biggest win. The old 10% or 5% TDS on your invoices was a major drain on working capital.

The New Reality: The new, low 2% TDS rate on services and the 0.1% rate for e-commerce operators means you get 98% (or 99.9%) of your invoice value in the bank, not locked up as a tax credit.

Your Action: Rework your financial projections for FY 2026-27. This improved cash flow might reduce your need for working capital loans or allow for faster reinvestment.

Review Your Business Structure

The old law had special exemptions and deductions that might have influenced your choice of a private limited company versus an LLP.

The New Reality: With most deductions gone, the “best” business structure is now the one that is simplest to manage and has the lowest compliance-cost-to-profit ratio.

Your Action: Sit with your CA or CS. Re-ask the question: “Given the new 30% unified tax and no deductions, is our current legal structure still the most efficient for us?”

Embrace New Audit Choices

You are no longer restricted to only a CA for your tax audit.

The New Reality: The DTC 2025 allows practicing Company Secretaries (CS) and Cost Accountants (CMA) to conduct tax audits.

Your Action: This creates competition and choice. Get quotes from all three types of professionals. You may find a CS or CMA is a better fit for your business model and offers a more competitive price.

For Large Corporations and MNCs: A Focus on Restructuring and Global Compliance

For large enterprises, the transition is far more complex. The focus must be on deep financial re-modelling and international tax alignment.

Re-model Your Entire Financial Statement

Your company’s “Effective Tax Rate” (ETR) is about to change, permanently.

The New Reality: The 30% unified rate is just the start. The removal of all Chapter VI-A and investment-linked deductions means your “Taxable Profit” will be much closer to your “Book Profit.”

Your Action: Your finance team must run detailed financial models now. Compare your projected ETR under the old Act (with deductions) to your ETR under the new DTC 2025 (at 30% but no deductions). This will have a direct impact on your P&L, shareholder reporting, and deferred tax asset calculations.

Plan for the Branch Profits Tax (BPT)

For all foreign companies with branches in India, this is a new, critical tax.

The New Reality: After you pay the 30% corporate tax, the new 15% Branch Profits Tax will be applied to profits repatriated to your head office.

Your Action: This requires a complete re-evaluation of your profit repatriation strategy. CFOs must decide on the optimal timing and quantum of repatriating profits versus reinvesting them in the Indian branch.

Re-evaluate All Investment Strategies (Capital Gains)

The new, simplified capital gains rule (taxing all gains as business income at 30%) is a game-changer for your treasury and investment-holding arms.

The New Reality: The old strategy of holding assets (like property or unlisted shares) for the long term to get a lower tax rate (20% with indexation) is dead.

Your Action: Your investment committee must review every single asset on your balance sheet. Does the holding strategy still make sense when the eventual profit will be taxed at a flat 30%, just like your regular business income?

The Critical Role of Your CFO and Tax Team: The Immediate Action Plan

Regardless of size, your finance and legal teams are on the clock. This is not a “wait and see” situation.

Immediate Step 1: Update All Vendor and Customer Contracts

Your legal and finance teams must start this today.

The New Reality: All your contracts have clauses that mention the old TDS rates (10% under 194J, 1% under 194-O, etc.). As of April 1, 2026, these clauses will be legally incorrect.

Your Action: Draft a standard addendum for all vendor agreements, rent agreements, and (especially) e-commerce platform contracts, updating the TDS clauses to reflect the new 2% and 0.1% rates.

Immediate Step 2: Upgrade Your Accounting and ERP Software

Your Tally, Zoho, or SAP system is hard-coded for the 1961 Act.

The New Reality: Your software is built to handle “Assessment Years,” 30+ TDS rates, and a long list of deductions. The DTC 2025 changes all of this.

Your Action: Contact your ERP/accounting software provider now. Ask for their DTC 2025 transition patch and a timeline for its rollout. You must have this new logic tested and implemented before April 1, 2026, or your compliance will fail on day one.

Immediate Step 3: Train Your People

The most powerful software is useless if your people are operating on old knowledge.

The New Reality: Your accounts payable team is conditioned to deduct 10%. Your finance managers are conditioned to find deductions. This mindset is now wrong.

Your Action: Schedule mandatory training sessions for your entire finance, legal, and leadership teams. They must un-learn 60 years of tax logic and learn the new, simplified Code.

What about Individuals? A Quick Look at the DTC 2025 for Employees and Owners

Your business is one part of the equation; your personal finances are the other. As a business owner, director, or key employee, the Direct Tax Code 2025 will dramatically change your personal income tax.

For individuals, the new Code (which becomes the default and, soon, the only regime) follows the same philosophy as it does for corporations: lower, simplified tax slabs in exchange for eliminating nearly all deductions (like 80C, 80D, HRA, etc.).

Here are the key changes you must know for your own financial planning.

The New Income Tax Slabs (Effective FY 2026-27)

The new slabs are designed to be simpler and provide significant relief to the middle class.

| Net Taxable Income (in ₹) | Tax Rate (%) |

| Up to 4,00,000 | Nil |

| 4,00,001 to 8,00,000 | 5% |

| 8,00,001 to 12,00,000 | 10% |

| 12,00,001 to 16,00,000 | 15% |

| 16,00,001 to 20,00,000 | 20% |

| 20,00,001 to 24,00,000 | 25% |

| Above 24,00,000 | 30% |

The Two Biggest Changes for Salaried Individuals

For anyone drawing a salary (including directors), these two changes are monumental:

- Rebate Makes ₹12 Lakh Tax-Free: The new Code increases the tax rebate under Section 87A to ₹60,000. The calculation is simple: at the new slab rates, an income of ₹12,00,000 results in a tax liability of exactly ₹60,000 (5% on one slab, 10% on the next). The rebate zeroes this out. For millions of professionals, this is the new “zero-tax” income level.

- Standard Deduction Increased to ₹75,000: The Standard Deduction for salaried individuals and pensioners is not only kept but is also increased from ₹50,000 to ₹75,000.

The New Math for Salaried Persons: If your gross salary is ₹12,75,000, you first subtract the ₹75,000 Standard Deduction. This leaves a taxable income of ₹12,00,000, which is then made tax-free by the ₹60,000 rebate.

How Investors are Affected: The End of Capital Gains as We Know It

This is the most radical change for individuals and is the flip side of the corporate capital gains rule.

- No More “Long-Term” vs. “Short-Term”: The complex system of 10% tax on long-term equity gains (LTCG), 15% on short-term (STCG), and 20% with indexation on property is abolished.

- The New Rule: Under the DTC 2025, all capital gains will be added to your regular income and taxed at your individual slab rate.

- The Impact: This is a massive shift.

- Low-Income Investors: If your total income (including gains) is under ₹12 lakh, your capital gains could effectively be tax-free.

- High-Income Investors: If you are in the 30% slab, your gains from shares, property, or mutual funds will also be taxed at 30%—a significant jump from the 10% or 20% you paid before. This requires a complete rethink of all personal investment strategies.

Dividends: Taxed at Your Slab Rate

The new Code continues the system of taxing dividends in the hands of the investor (after the removal of the old Dividend Distribution Tax).

- The Rule: Any dividend income you receive from your business or other investments will be added to your “Income from Other Sources” and taxed at your applicable slab rate.

- The Compliance: Companies will now be required to deduct TDS at 10% on dividend payments exceeding ₹10,000 in a financial year.

The Big Question: Will the Direct Tax Code 2025 Really Simplify Things?

This has been the promise for over a decade: “a simpler, more transparent tax law.” Now that it is here, will it deliver?

The answer, based on our analysis, is a resounding yes—but with a painful transition.

The DTC 2025 wins on its three core philosophical goals: simplification, transparency, and the reduction of litigation.

The “Pros”: Where the DTC 2025 is a Clear Victory for Businesses

- Structural Simplification: The new law itself is the biggest win. We have moved from a 700+ section legal monster (the 1961 Act) to a streamlined Code of ~300-500 sections. This isn’t just a “diet”; it’s a complete removal of decades of exemptions, circulars, and special provisions that were dead wood.

- An End to Ambiguity: The Code abolishes confusing concepts that were breeding grounds for legal disputes.

- “Assessment Year” is Gone: We now only have the “Tax Year.” This single change will eliminate millions of clerical errors and “off-by-one-year” filing mistakes.

- “RNOR” Status is Gone: The “Resident but Not Ordinarily Resident” status was a complex grey area. The new Code is binary: you are either a “Resident” (taxed on global income) or “Non-Resident” (taxed on Indian income). It’s clean and clear.

- Massive Reduction in Compliance: The rationalization of TDS is a masterpiece of simplification. Moving from 30+ different rates to just a few (like 2% and 0.1%) is a game-changer. It frees up working capital, reduces errors, and simplifies accounting for every business in India.

- Certainty in Tax Rates: A unified 30% corporate rate and the removal of MAT (for most) ends the “which regime is better for me?” paralysis. You now know your rate. You can plan, invest, and project with certainty.

The “Cons”: Potential Teething Problems and Strategic Challenges

Simplicity is not the same as “easy.” The transition will be the hardest part.

- The “Grand Bargain” Is Tough: Businesses have been addicted to deductions for 60 years. An entire generation of CAs and CFOs was trained to plan taxes, not just comply. Shifting this mindset from “how do I save tax?” to “how do I report my profit accurately?” is a cultural challenge, not a legal one.

- Software and Contract Upheaval: As outlined in the strategy section, every single ERP system and every single vendor contract in India is now obsolete. The cost and effort to update all this by April 1, 2026, is immense.

- Unintended Consequences: New laws always create new loopholes and new problems. Will the new GAAR provisions be used fairly? How will authorities interpret the new capital gains rules? We are entering a 2-3 year period of “testing” the new Code, which may see a short-term spike in disputes before the long-term peace.

Expert Opinions: What Chartered Accountants and Tax Lawyers are Saying

The consensus in the professional community is one of “cautious optimism.”

Most tax experts are thrilled to leave the 1961 Act behind. They see the DTC 2025 as a necessary, if overdue, reset that aligns India with global best practices. They celebrate the end of litigation-heavy concepts like MAT and the FY/AY confusion.

However, they also caution that the real test will be in the administration. A simple law, if administered poorly or aggressively, can be just as painful as a complex one. The success of the DTC 2025 now rests on the shoulders of the tax department and its willingness to embrace the new spirit of transparency and partnership over mere revenue collection.

Conclusion: Your 5-Point Business Checklist for the Direct Tax Code 2025

The Direct Tax Code 2025 is not a future event. It is a present-day business reality. With its provisions taking effect from April 1, 2026, you are currently in the final year of the old regime. The time to act is not next year; it is this quarter.

The era of “tax savings” is over. The era of “tax compliance” and “business efficiency” has begun. The companies that thrive will not be those that find a new loophole, but those that adapt their systems, strategy, and mindset the fastest.

This 5,000-word guide has given you the ‘what’ and ‘why’. Here is the ‘now’.

Your Immediate 5-Point Action Plan:

- Engage Your Advisor (Today): Book a meeting with your CA, CS, or Tax Lawyer. Your agenda item: “DTC 2025 Transition Strategy.”

- Launch a “Code Red” Financial Model: Task your CFO with re-projecting your P&L and ETR (Effective Tax Rate) for FY 2026-27 under the new 30% rate and zero deductions.

- Start a Legal and Software Audit: Identify every single contract with a TDS clause and every piece of accounting software hard-coded to the 1961 Act.

- Re-evaluate All Investments: With capital gains now taxed as business income (at 30%), review your company’s (and your personal) investment portfolio.

- Train Your Team: Your accounts and finance teams are operating on 60-year-old logic. Start their re-education on the new Code immediately.

FAQs

When does the new Direct Tax Code 2025 actually start?

The new Direct Tax Code (DTC) 2025 is already law, having received Presidential assent in August 2025. However, its provisions will become effective from April 1, 2026. This means it will apply to all income earned in the Financial Year 2026-27 and onwards. The current FY 2025-26 is the last year to be governed by the old Income Tax Act, 1961.

What is the new corporate tax rate for my private limited company?

The new corporate tax rate is a unified, flat 30% for all companies, whether domestic or foreign. This replaces the old, complex system of multiple rates (like 22%, 25%, 30%, and 40%). This 30% rate is part of a “grand bargain”: the rate is fixed, but most major tax deductions and exemptions have been removed.

Are all deductions like 80C, 80D, and HRA gone for individuals?

Yes. Under the new DTC 2025, which becomes the default and only tax regime, almost all popular deductions have been eliminated. This includes Chapter VI-A (like 80C for PF/insurance, 80D for health insurance), HRA exemption, and LTA. The trade-off is a new, lower tax slab structure and a higher tax-free bracket.

What is the new TDS rate for professional services or contractors?

The complex web of 30+ TDS rates is gone. The DTC 2025 rationalizes this to a few simple buckets. For most business payments, including professional services (CA, lawyer, consultant) and payments to contractors, the new standard TDS rate is just 2% (down from 10% or 5%). For e-commerce operators, the rate is even lower at 0.1%.

How are capital gains from shares or property taxed now?

The distinction between “short-term” and “long-term” capital gains has been abolished. Under the DTC 2025, all capital gains (from shares, mutual funds, property, etc.) are to be added to your regular income and will be taxed at your applicable personal income tax slab rate.

Is my income really tax-free up to ₹12.75 lakhs?

It’s slightly different. For a salaried individual:

1. You get a Standard Deduction of ₹75,000. So, a gross salary of ₹12,75,000 becomes a taxable income of ₹12,00,000.

2. The new tax slabs apply, resulting in a tax liability of ₹60,000.

3. The new Code provides a tax rebate of ₹60,000. This rebate fully cancels out the tax liability, making a gross salary of up to ₹12,75,000 effectively tax-free.

What is the single most important thing my business should do right now?

Call your tax advisor (CA, CS, or CMA) immediately. Your single most urgent task is to understand how the new 30% rate and the removal of all your existing deductions will impact your company’s “Effective Tax Rate” and cash flow, starting in FY 2026-27. You must also begin the process of updating all your vendor/customer contracts to reflect the new TDS rates.