Introduction to Accounting Principles

Think of accounting principles like the rules of the road. Without them, driving would be absolute chaos. That’s exactly how businesses would function without accounting rules — a mess of numbers with no meaning. Whether you’re a small business owner or just curious about how companies track their money, understanding accounting principles is a game-changer.

What Are Accounting Principles?

In simple words,accounting principles are the standard rules and practices that guide how accountants document and present financial information. They bring structure, logic, and uniformity to financial statements so that everyone — from CEOs to investors — can understand what’s going on.

Why Do They Matter?

Imagine trying to compare two company reports if each used a different method of tracking revenue. Total confusion, right? These principles ensure every company speaks the same financial language. These standards cultivate trust and enable stakeholders to make well-researched monetary decisions.

Fundamental Accounting Principles

Let’s take a closer look at some of the big players — the fundamental principles that every accountant lives by.

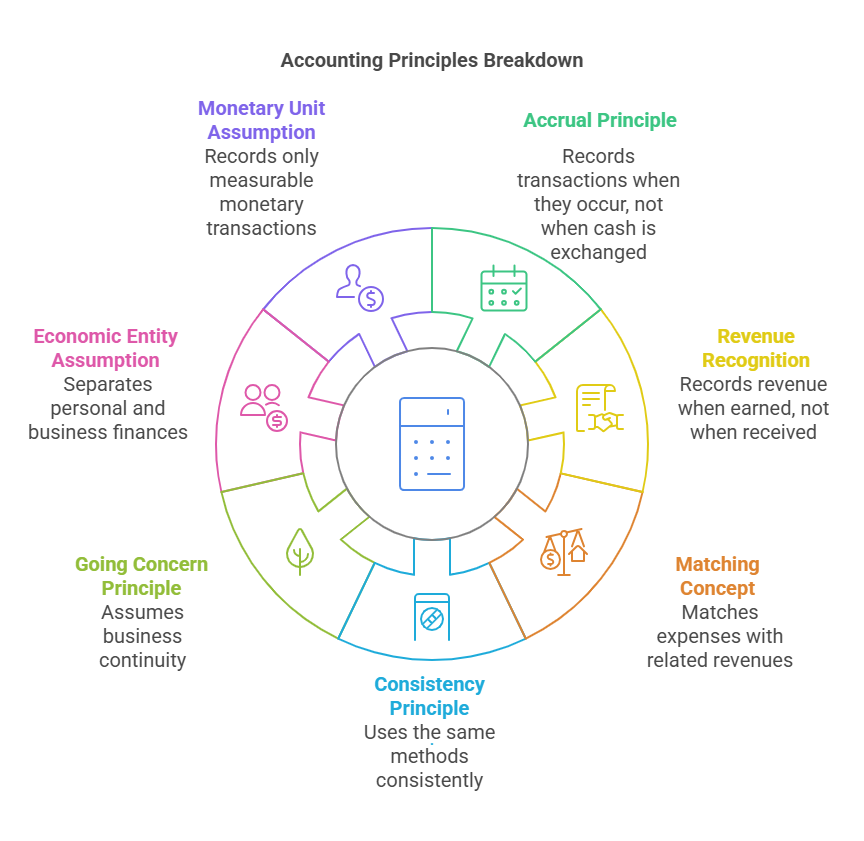

Accrual Principle

According to this principle, income and expenses must be documented at the time they occur, regardless of when the cash is actually received or paid. It gives a clearer picture of a company’s real financial position.

Revenue Recognition

Under accrual accounting, revenue is booked at the point of fulfillment rather than payment receipt. So, if you completed a job in January but got paid in February, January’s books get the credit.

Matching Concept

This principle requires that expenses be recorded in the same accounting period as the revenues they help generate. If you sell a product in March, you also record the cost of that product in March.

Consistency Principle

Businesses should maintain the same accounting approach over time to ensure reliable financial performance analysis across different periods. Imagine switching recipes every time you bake a cake — consistency is key to knowing what works.

Going Concern Principle

This assumes the business will keep running for the foreseeable future unless there’s proof it won’t. It affects how assets are valued and how liabilities are treated.

Economic Entity Assumption

This principle separates personal and business finances. Just because you own the business doesn’t mean your vacation in Bali belongs on the company’s books.

Monetary Unit Assumption

Only financial transactions that can be measured in money get recorded. Emotional value, goodwill, or employee morale? Important — but they don’t go in the ledger.

Additional Accounting Principles

These principles dig deeper, helping refine how financial data is handled.

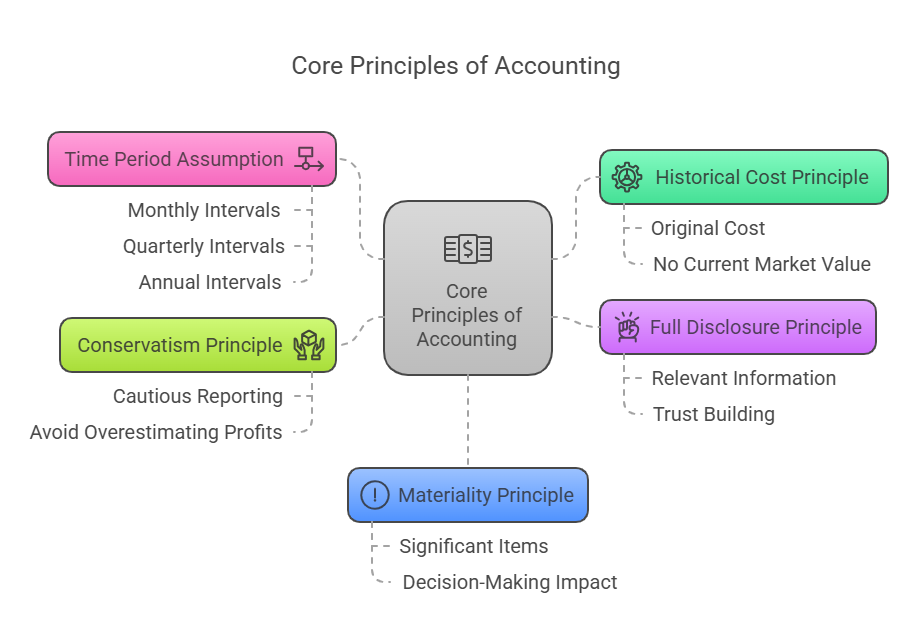

Historical Cost Principle

Assets should be recorded at their original cost — not what they’re worth today. So if your office building has tripled in value, your balance sheet still shows what you paid for it.

Full Disclosure Principle

If there’s something that could affect how someone interprets your financial statements, you need to disclose it. No hiding skeletons in the financial closet.

Conservatism Principle

Accountants are taught to play it safe. If there’s uncertainty, pick the option that’s less likely to overstate profits or assets.

Materiality Principle

Not everything needs to be reported — only the stuff that could influence decisions. Lost a pen worth $2? Not material. Lost a shipment worth $20,000? Definitely material.

Time Period Assumption

Businesses report results in consistent time frames — like monthly, quarterly, or annually — so performance can be measured and compared easily.

Understanding GAAP and Its Role

What Is GAAP?

The Generally Accepted Accounting Principles (GAAP) establish the regulatory foundation for American accounting methods. It ensures that all companies follow the same rules, which is critical for transparency.

GAAP vs IFRS: What’s the Difference?

GAAP is used in the U.S., while IFRS (International Financial Reporting Standards) is used globally. GAAP’s rule-oriented system contrasts with IFRS’s reliance on professional interpretation. Think of it like the difference between strict instructions and flexible guidelines.

How These Principles Play Out in Real Life

In Business Strategy and Decisions

Accounting principles help businesses make smart choices — from where to invest money to when to launch a product. Accurate records are the foundation of every big move.

In Financial Statements

Financial statements including cash flow reports and balance sheets are grounded in these rules, providing investors with reliable metrics to judge company performance.

In Audits and Compliance

Auditors check whether businesses are following accounting rules. If a company tries to fudge the numbers, it’s the auditors’ job to call them out.

What Happens When Rules Are Broken

Financial Consequences

Breaking accounting principles can lead to inaccurate reports, investor backlash, fines, or worse — total business collapse. Just look at companies that have faced accounting scandals (Enron, anyone?).

Legal and Ethical Risks

Not following accounting rules isn’t just bad practice — in many cases, it’s illegal. Plus, it kills your reputation faster than a bad Yelp review.

What’s Next for Accounting Principles

Embracing Tech and AI

New tools like AI and cloud accounting software are reshaping the industry. But no matter how advanced the tech gets, the principles remain the foundation.

Reinforcing Trust and Transparency

In an era of digital business and global investments, people want transparency. Following accounting principles helps build trust — which is worth more than gold in today’s market.

Conclusion

Accounting principles might sound technical, but they’re the glue that holds financial reporting together. They make the chaotic world of numbers understandable and trustworthy. Whether you’re managing a side hustle, running a company, or just trying to make smarter money decisions — understanding these principles puts you ahead of the game.

FAQs

1. What are the 5 basic principles of accounting?

They include the revenue recognition principle, matching principle, historical cost principle, full disclosure principle, and objectivity principle.

2. Why is consistency important in accounting?

It ensures that financial data can be compared across different periods, making trends and changes easier to identify.

3. How does the accrual principle benefit businesses?

It gives a more accurate picture of a company’s performance by recording income and expenses when they occur, not just when cash is received or paid.

4. Are accounting principles legally binding?

Some principles are enforced by law, especially when it comes to regulated financial reporting. Ignoring them can lead to serious legal trouble.

5. What’s the difference between GAAP and IFRS?

GAAP is the U.S. accounting standard and is more rules-based, while IFRS is used internationally and is more flexible and principles-based.