Navigating the labyrinthine world of income tax can be a daunting task, especially for small taxpayers. Every year, as the tax season approaches, a flurry of questions and confusion arises. One such area of contention that has recently been in the limelight is the availability of the tax rebate under Section 87A Rebate of the Income Tax Act, 1961, on Short-Term Capital Gains (STCG). This issue has been a bone of contention between taxpayers and the Income Tax Department, leading to a significant dispute that has finally been addressed by the Income Tax Appellate Tribunal (ITAT).

This comprehensive blog post will delve deep into the nuances of the tax rebate under Section 87A Rebate, the ongoing STCG dispute, and the landmark ITAT rulings that have brought much-needed clarity to the matter. We will explore the eligibility criteria for the rebate, the arguments from both sides of the dispute, a detailed analysis of the ITAT’s decisions, and the practical implications for taxpayers. So, whether you are a seasoned investor or a novice trying to understand the intricacies of tax laws, this guide will equip you with the knowledge you need to navigate this complex issue.

What is the Tax Rebate under Section 87A?

Section 87A Rebate of the Income Tax Act provides a rebate to resident individuals, which can significantly reduce their tax liability. This provision was introduced to provide relief to taxpayers in the lower income brackets. Let’s break down the key aspects of this rebate.

Who is Eligible for the Rebate?

To be eligible for the tax rebate under Section 87A, a taxpayer must meet the following conditions:

Residency and Total Income Criteria

- Resident Individual: The rebate is available only to resident individuals. It cannot be claimed by Hindu Undivided Families (HUFs), Association of Persons (AOPs), Body of Individuals (BOIs), firms, or companies.

- Total Income Threshold: The eligibility for the rebate is linked to the taxpayer’s total income. The threshold has been revised over the years, and it’s crucial to know the applicable limit for the relevant assessment year.

Changes in Eligibility over the Years

The income threshold for claiming the rebate under Section 87A Rebate has been progressively increased by the government to provide more relief to small taxpayers. Here’s a quick look at the evolution of this limit:

- Initial Introduction: When the rebate was first introduced, the income limit was much lower.

- Recent Amendments: In recent years, especially with the introduction of the new tax regime, the income threshold has been substantially increased.

How much is the Rebate?

The amount of rebate available under Section 87A has also seen changes over time. The rebate is the lower of the actual income tax payable or the maximum prescribed limit.

Evolution of the Rebate Amount

The maximum rebate amount has been increased in tandem with the changes in the income threshold, offering more significant tax savings to eligible individuals.

Eligibility for Section 87A Rebate

To qualify for this tax relief, you must meet two primary conditions:

- Residency: You must be a resident individual in India. This rebate is not available for HUFs, firms, or non-residents.

- Income Threshold: Your total taxable income must be below the limit specified for your chosen tax regime.

Rule of Rebate Calculation

A crucial point to remember is that the rebate is always the lower of two amounts:

- The maximum rebate amount allowed under your tax regime.

- Your actual income tax liability (calculated before adding the Health and Education Cess).

Rebate Amounts: New vs. Old Tax Regime

1. Under the New Tax Regime: The rebate here is tiered and has been updated for the upcoming financial year.

- For Financial Year 2024-25 (AY 2025-26): If your income is up to ₹7 lakh, you are eligible for a rebate of up to ₹25,000.

- For Financial Year 2025-26 (AY 2026-27): The benefit increases significantly. If your income is up to ₹12 lakh, you can claim a rebate of up to ₹60,000.

2. Under the Old Tax Regime: The rules remain consistent.

- If your income is up to ₹5 lakh, you can claim a tax rebate of up to ₹12,500.

Future Changes

There are specific incomes against which this rebate cannot be claimed:

- Current Rule: The rebate cannot be used to offset tax payable on Long-Term Capital Gains (LTCG) under Section 112A.

- Upcoming Change: Starting from Financial Year 2025-26, the rebate will no longer be applicable against tax on any income that is subject to special tax rates.

The “Tax Payable” Conundrum

The language of Section 87A states that the rebate is available on the “income-tax payable on the total income”. This phrasing is at the heart of the STCG dispute, as the interpretation of “total income” and “tax payable” has been a subject of debate.

Section 87A Rebate on Short-Term Capital Gains (STCG)

The primary point of contention revolves around whether the tax rebate under Section 87A can be claimed against the tax payable on STCG, especially those taxed at a special rate under Section 111A.

A Primer on Short-Term Capital Gains (STCG)

Before we delve into the dispute, let’s quickly understand what STCG is.

What are Capital Gains?

Capital gains arise from the sale or transfer of a capital asset, such as property, stocks, mutual funds, etc. The gain is the difference between the selling price and the cost of acquisition of the asset.

STCG under Section 111A vs. Other STCG

- STCG under Section 111A: This refers to the short-term capital gains arising from the sale of equity shares listed on a recognized stock exchange, units of an equity-oriented mutual fund, or units of a business trust, where the transaction is subject to the Securities Transaction Tax (STT). These gains are taxed at a special rate of 15% (plus applicable cess and surcharge).

- Other STCG: Short-term capital gains from the sale of assets other than those covered under Section 111A are taxed at the normal slab rates applicable to the individual.

The Contention of the Income Tax Department

The Income Tax Department has been of the view that the rebate under Section 87A is not available against the tax payable on STCG under Section 111A. Their arguments are based on the following premises:

- Special Rate of Tax: The department contends that since STCG under Section 111A is taxed at a special rate, it should be treated differently from the income taxed at normal slab rates.

- Legislative Intent: The department argues that the legislative intent behind Section 87A was to provide relief to small taxpayers on their regular income, and not on income from capital gains, which is considered to be in the nature of a bonus or a windfall.

- Exclusion of Long-Term Capital Gains (LTCG): The department has also pointed to the fact that the rebate is explicitly not available on LTCG taxed under Section 112A. They have tried to draw a parallel to STCG, even though there is no explicit exclusion for STCG in the law.

The Taxpayer’s Argument

Taxpayers, on the other hand, have put forth strong counter-arguments, which are primarily based on a literal interpretation of the law. Their key arguments are:

- No Explicit Exclusion: The most compelling argument from the taxpayer’s side is that Section 87A does not explicitly exclude STCG under Section 111A from the purview of the rebate. The law simply states that the rebate is available on the “income-tax payable on the total income”.

- Definition of “Total Income”: The “total income” as defined under the Income Tax Act includes all sources of income, including capital gains. Therefore, the tax payable on the total income would naturally include the tax on STCG.

- Plain Reading of the Law: Taxpayers have argued for a plain and literal reading of the statute. In the absence of any specific provision to the contrary, the rebate should be available on the entire tax liability, including the tax on STCG.

Marginal Relief for Taxpayers

In the new tax regime, you pay zero tax up to an income of ₹7 lakhs thanks to the Section 87A rebate. But what happens if your income is, say, ₹7,15,000? Without a special rule, you’d face a “tax cliff”—a small increase in income would cause a massive jump in your tax bill.

This is where Marginal Relief comes in. Think of it as a safety net that ensures your tax increase is never more than your income increase over the ₹7 lakh threshold.

The Core Principle: Your final tax payable (before cess) cannot be more than the extra income you earned above ₹7 lakhs.

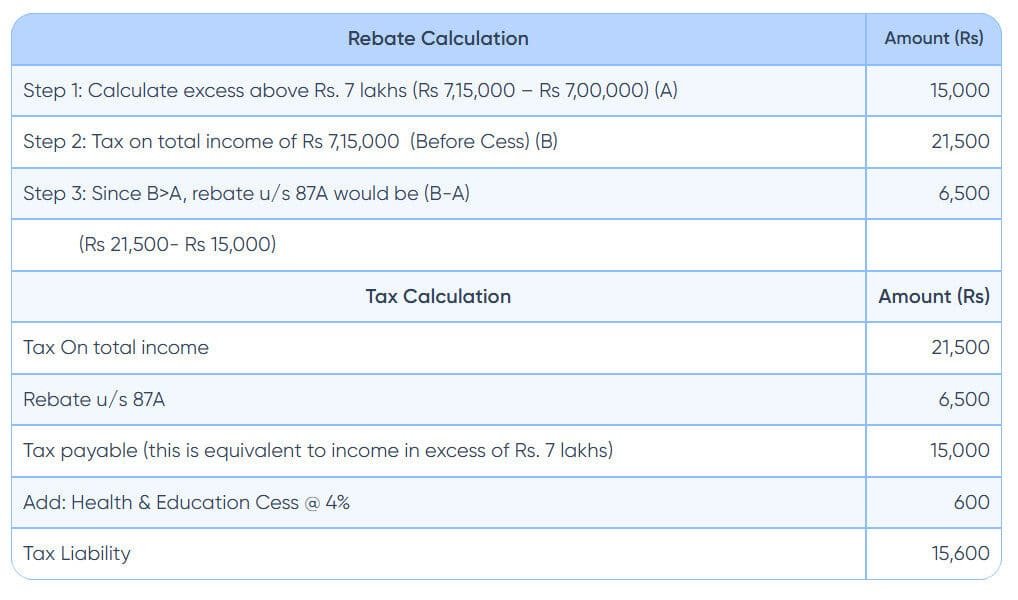

Let’s see how this works with Mr. Ravi, whose income is ₹7,15,000 for FY 2024-25.

- Find the “Extra” Income: First, we see how much he earned over the limit.

- ₹7,15,000 – ₹7,00,000 = ₹15,000

- Calculate the “Normal” Tax: Next, we calculate the tax on his total income as per the slab rates.

- Tax on ₹7,15,000 comes to ₹21,500.

- Apply the Safety Net: Now, compare the two figures. The normal tax of ₹21,500 is much higher than his extra income of ₹15,000. This is unfair!

- Marginal relief steps in and caps his tax payable (before cess) at his extra income amount.

Solution

| Rebate Calculation | Amount (Rs) |

| Step 1: Calculate excess above Rs. 7 lakhs (Rs 7,15,000 – Rs 7,00,000) (A) | 15000 |

| Step 2: Tax on total income of Rs 7,15,000 (Before Cess) (B) | 21500 |

| Step 3: Since B>A, rebate u/s 87A would be (B-A) | 6500 |

| (Rs 21,500- Rs 15,000) | |

| Tax Calculation | Amount (Rs) |

| Tax On total income | 21500 |

| Rebate u/s 87A | 6500 |

| Tax payable (this is equivalent to income in excess of Rs. 7 lakhs) | 15000 |

| Add: Health & Education Cess @ 4% | 600 |

| Tax Liability | 15600 |

Steps to Claim Income Tax Rebate in FY 2024-25?

Step 1: Calculate Your Total Earnings First, add up all your income from every source (salary, business, etc.) for the financial year (April 1, 2024, to March 31, 2025). This gives you your Gross Total Income.

Step 2: Determine Your Net Taxable Income Next, subtract any tax deductions you are eligible for. This step is where the Old and New Tax Regimes differ significantly.

- Old Regime: You can subtract deductions under Section 80C (for investments), 80D (for health insurance), 80G (for donations), and others.

- New Regime: Most major deductions, including Section 80C, are not available.

The figure you arrive at after deductions is your Net Taxable Income.

Step 3: Check Your Eligibility for the Rebate This is the final check. If your Net Taxable Income is within the specified limit for your regime, you qualify for the rebate.

How is the Rebate Applied? It’s Automatic! You don’t need to manually claim the rebate. When you file your Income Tax Return (ITR), the official tax portal is designed to automatically calculate and apply the Section 87A rebate for you, as long as your declared income meets the criteria.

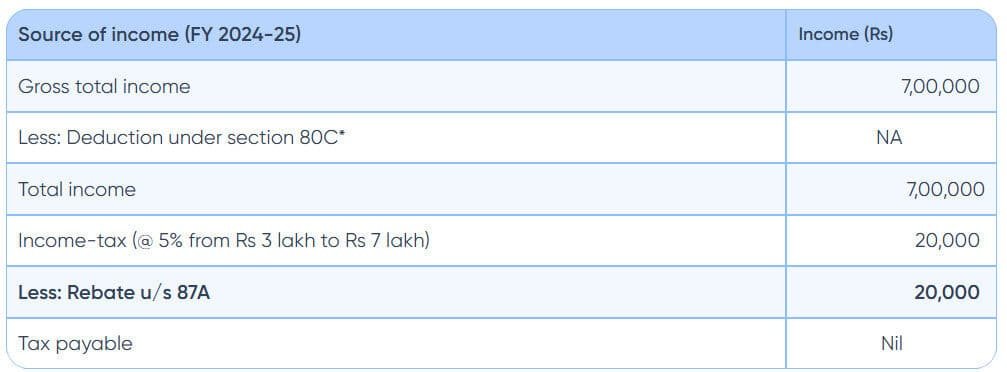

Examples for AY 2025-26

New Tax Regime

An individual’s income is ₹7,00,000. Since no deductions apply, their net taxable income is also ₹7,00,000.

| Source of income (FY 2024-25) | Income (Rs) |

| Gross total income | 700000 |

| Less: Deduction under section 80C* | NA |

| Total income | 700000 |

| Income-tax (@ 5% from Rs 3 lakh to Rs 7 lakh) | 20000 |

| Less: Rebate u/s 87A | 20000 |

| Tax payable | Nil |

the tax liability (₹20,000) is less than the maximum rebate (₹25,000), the entire tax is wiped out.

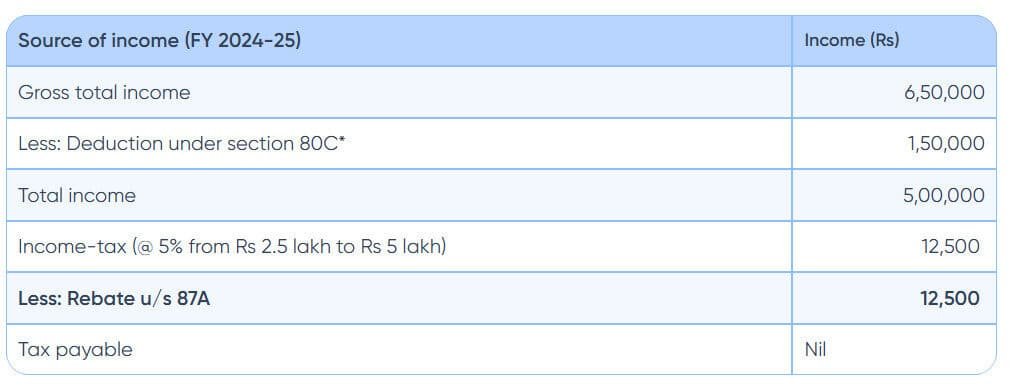

Old Tax Regime

An individual’s gross income is ₹6,50,000. They use deductions to lower their taxable income.

| Source of income (FY 2024-25) | Income (Rs) |

| Gross total income | 650000 |

| Less: Deduction under section 80C* | 150000 |

| Total income | 500000 |

| Income-tax (@ 5% from Rs 2.5 lakh to Rs 5 lakh) | 12500 |

| Less: Rebate u/s 87A | 12500 |

| Tax payable | Nil |

By using deductions, their net income falls to the ₹5 lakh threshold, making them eligible for the full rebate.

The Judiciary Steps In: Landmark ITAT Rulings

The dispute over the availability of the Section 87A rebate on STCG has been the subject of several legal battles, with the Income Tax Appellate Tribunal (ITAT) delivering some landmark rulings in favor of the taxpayers.

Analysis of Key ITAT Judgements

Two recent ITAT rulings, one by the Ahmedabad bench and another by the Bengaluru bench, have been particularly significant in settling this dispute.

The Ahmedabad ITAT Ruling

In a recent case, the Ahmedabad ITAT held that a resident individual opting for the new tax regime with a total income below the prescribed threshold is entitled to claim the rebate under Section 87A against the tax payable on STCG taxable under Section 111A. The tribunal’s reasoning was based on the following key observations:

- No Statutory Prohibition: The tribunal found no express statutory prohibition in either Section 87A or Section 111A that would deny the rebate on STCG.

- Clear Language of the Law: The ITAT emphasized that the language of Section 87A is clear and unambiguous. It allows for a rebate on the “income-tax payable on the total income”, without any distinction between tax on normal income and tax on income taxed at special rates.

- System-Generated Denial is Not Law: The tribunal also noted that the denial of the rebate by the Centralized Processing Centre (CPC) was system-generated and lacked a statutory basis. A system-driven denial cannot override a taxpayer’s statutory entitlement.

The Bengaluru ITAT Ruling

The Bengaluru ITAT, in another case, also ruled in favor of the taxpayer, allowing the claim of the Section 87A rebate in a revised income tax return. This ruling further reinforces the taxpayer’s right to claim the rebate on STCG. The key takeaways from this ruling are:

- Rebate is a Statutory Right: The tribunal held that the rebate under Section 87A is a statutory relief and cannot be denied on mere technical grounds.

- Genuine Error can be Rectified: The ITAT acknowledged that the failure to claim the rebate in the original return was a genuine error that could be rectified by filing a revised return.

The Precedential Value of ITAT Rulings

It is important to understand that the rulings of the ITAT are not the law of the land, but they hold significant precedential and persuasive value. They are binding on the tax authorities within the jurisdiction of the respective ITAT bench. These rulings provide a strong basis for taxpayers to claim the rebate on STCG and to challenge any denial by the tax department.

Practical Implications for Taxpayers

The favorable rulings from the ITAT have significant practical implications for taxpayers. Here’s what you need to know:

How to Claim the Rebate on STCG: A Step-by-Step Guide

If you are eligible for the tax rebate under Section 87A and have STCG income, you should claim the rebate in your income tax return.

Filing your Income Tax Return (ITR)

When filing your ITR, the tax filing utility should ideally calculate and apply the rebate automatically if you are eligible. However, there have been reports of the utility not allowing the rebate on STCG. In such a scenario, you may have to manually claim the rebate.

What to do if the department disputes your claim

If the tax department disputes your claim for the rebate on STCG, you can take the following steps:

- File a Rectification Request: If your return is processed and the rebate is denied, you can file a rectification request under Section 154 of the Income Tax Act, citing the favorable ITAT rulings.

- File an Appeal: If the rectification request is rejected, you can file an appeal with the Commissioner of Income Tax (Appeals) [CIT(A)].

- Further Appeal to ITAT: If the CIT(A) also rules against you, you can file a further appeal with the ITAT, which is likely to rule in your favor, given the existing precedents.

Potential Legislative Changes

It is important to note that the government has taken cognizance of this issue. In the Finance Act, 2025, an amendment has been made to Section 87A, which will restrict the availability of the rebate on incomes taxed at special rates, including STCG under Section 111A. This amendment will be effective from the Assessment Year 2026-27 (Financial Year 2025-26).

This means that for the assessment years prior to AY 2026-27, the ITAT rulings will hold strong ground, and taxpayers can continue to claim the rebate on STCG. However, from AY 2026-27 onwards, the rebate will not be available on STCG.

Conclusion

The dispute over the availability of the tax rebate under Section 87A on STCG has been a long-standing issue, causing confusion and hardship for many small taxpayers. The recent landmark rulings by the ITAT have provided much-needed clarity and have come as a major relief to taxpayers. The tribunal’s decisions have upheld the principle of literal interpretation of the law and have reinforced the taxpayer’s right to claim the rebate in the absence of any explicit prohibition in the statute.

While the government has now amended the law to restrict the rebate on STCG from AY 2026-27 onwards, the ITAT rulings remain relevant for the prior assessment years. Taxpayers who have been wrongly denied the rebate can take recourse to the legal remedies available to them and claim their rightful tax benefit. It is always advisable to consult with a tax professional to understand the nuances of the law and to ensure that you are claiming all the deductions and rebates that you are entitled to.

FAQs

Can I claim the rebate under Section 87A on STCG for AY 2024-25?

Yes, based on the recent ITAT rulings, you can claim the rebate under Section 87A on STCG for AY 2024-25, provided you meet the other eligibility conditions.

What should I do if the ITR utility does not allow me to claim the rebate on STCG?

If the ITR utility does not allow you to claim the rebate on STCG, you can try to file your return and then file a rectification request. Alternatively, you can seek professional help to explore other options for claiming the rebate.

Will the ITAT rulings apply to all taxpayers across India?

While the ITAT rulings have a strong persuasive value, they are binding only on the tax authorities within the jurisdiction of the respective ITAT bench. However, these rulings can be cited as precedents in other jurisdictions as well.

Is the rebate under Section 87A available on all types of capital gains?

No, the rebate under Section 87A is explicitly not available on long-term capital gains (LTCG) taxed under Section 112A. As per the recent ITAT rulings, it is available on STCG under Section 111A for assessment years prior to AY 2026-27.

What is the new rule regarding the rebate on STCG from AY 2026-27?

From AY 2026-27 onwards, the Finance Act, 2025 has amended Section 87A to restrict the availability of the rebate on incomes taxed at special rates, including STCG under Section 111A. Therefore, from AY 2026-27, you will not be able to claim the rebate on STCG.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.