Understanding the Tax Audit Criteria AY 2025-26 is paramount during the crucial tax season, a period of meticulous planning, careful calculations, and strict adherence to deadlines for businesses and professionals alike. One of the most critical aspects of this season is the tax audit, a thorough examination of a taxpayer’s financial records to ensure they comply with tax laws.

For the Assessment Year (AY) 2025-26, it is essential for every taxpayer to be aware of the criteria that necessitate a tax audit. This comprehensive guide will serve as a ready reckoner, helping you navigate the complexities of the Income Tax Act with ease and confidence.

Introduction to Tax Audit and its Importance

What is a Tax Audit?

A tax audit is an independent audit of the books of accounts of a taxpayer by a practicing Chartered Accountant. The primary objective of a tax audit is to ensure that the taxpayer has maintained proper books of account and that the financial statements reflect a true and fair view of their financial position. The audit report is then submitted to the Income Tax Department in the prescribed format.

Why is a Tax Audit Important?

A tax audit serves several important purposes:

- Ensures Accuracy: It ensures that the financial statements are accurate and reliable.

- Promotes Compliance: It promotes compliance with the tax laws and regulations.

- Detects Errors and Frauds: It helps in the detection of errors and frauds in the books of account.

- Facilitates Assessment: It facilitates the assessment of taxes by the Income Tax Department.

- Avoids Penalties: It helps in avoiding penalties and legal complications that may arise due to non-compliance.

Who can conduct a Tax Audit?

A tax audit can only be conducted by a practicing Chartered Accountant who holds a valid certificate of practice from the Institute of Chartered Accountants of India (ICAI).

Understanding the Legal Framework: Section 44AB of the Income Tax Act, 1961

The requirement for a tax audit is governed by Section 44AB of the Income Tax Act, 1961. This section specifies the conditions under which a taxpayer is required to get their accounts audited.

The Objective of Section 44AB

The main objective of Section 44AB is to ensure that the books of account and other records of the taxpayer are properly maintained and that they reflect the true income of the taxpayer. It also helps in preventing tax evasion and avoidance.

Key Provisions of Section 44AB for AY 2025-26

For AY 2025-26, Section 44AB mandates a tax audit for the following categories of taxpayers:

- Businesses: If the total sales, turnover, or gross receipts from the business exceed a certain threshold.

- Professionals: If the gross receipts from the profession exceed a certain threshold.

- Taxpayers under Presumptive Taxation Schemes: If they claim their income to be lower than the deemed profits and gains under the presumptive taxation schemes and their total income exceeds the basic exemption limit.

Tax Audit Criteria for Businesses for AY 2025-26

The General Turnover Limit

For businesses, the general turnover limit for a tax audit is ₹1 crore. If the total sales, turnover, or gross receipts of a business exceed ₹1 crore in the financial year 2024-25 (relevant to AY 2025-26), then a tax audit is mandatory.

What is included in “Turnover”?

The term “turnover” is not defined in the Income Tax Act. However, it is generally understood to mean the aggregate amount for which sales are effected or services are rendered by an enterprise. It includes excise duty, but excludes GST.

The Enhanced Turnover Limit for Digital Transactions

To promote digital transactions, the government has provided a relaxation in the turnover limit for businesses that conduct most of their transactions through digital modes. The turnover limit for a tax audit is increased to ₹10 crore if the following conditions are met:

The 95% Digital Transaction Rule Explained

The enhanced limit of ₹10 crore is applicable only if:

Key Considerations for Tax Audit Criteria AY 2025-26

- The aggregate of all receipts in cash during the previous year does not exceed 5% of the total receipts; AND

- The aggregate of all payments in cash during the previous year does not exceed 5% of the total payments.

If a business fails to meet even one of these conditions, the general turnover limit of ₹1 crore will be applicable.

What are considered “Digital Transactions”?

Digital transactions include payments or receipts made through:

- Account payee cheque

- Account payee bank draft

- Electronic Clearing System (ECS) through a bank account

- Credit card

- Debit card

- Net banking

- IMPS (Immediate Payment Service)

- UPI (Unified Payments Interface)

- RTGS (Real Time Gross Settlement)

- NEFT (National Electronic Funds Transfer)

- BHIM (Bharat Interface for Money) Aadhar Pay

Tax Audit for Businesses under Presumptive Taxation (Section 44AD)

Understanding Section 44AD

Section 44AD of the Income Tax Act provides a presumptive taxation scheme for small businesses. Under this scheme, eligible businesses can declare their income at a prescribed rate of their turnover, without having to maintain detailed books of account. The prescribed rates are:

- 8% of the total turnover or gross receipts.

- 6% of the total turnover or gross receipts, in respect of the amount received through digital modes.

The turnover limit for opting for the presumptive taxation scheme under Section 44AD is ₹2 crore. This has been increased to ₹3 crore from FY 2023-24, provided the cash receipts do not exceed 5% of the total turnover.

When does a business under Section 44AD need a Tax Audit?

A tax audit is mandatory for a business that has opted for the presumptive taxation scheme under Section 44AD, if:

- The business claims its profits and gains to be lower than the deemed profits (8% or 6% of the turnover); AND

- The total income of the business exceeds the basic exemption limit.

The “5-Year Rule” under Section 44AD

If a business opts for the presumptive taxation scheme under Section 44AD and in any of the subsequent five assessment years, it opts out of the scheme, then it will not be eligible to opt for the scheme for the next five assessment years. In such a case, the business will have to maintain books of account and get them audited if its total income exceeds the basic exemption limit.

Tax Audit Criteria for Professionals for AY 2025-26

The Gross Receipts Limit for Professionals

For professionals, the gross receipts limit for a tax audit is ₹50 lakh. If the gross receipts of a professional exceed ₹50 lakh in the financial year 2024-25, then a tax audit is mandatory.

Tax Audit for Professionals under Presumptive Taxation (Section 44ADA)

Understanding Section 44ADA

Section 44ADA of the Income Tax Act provides a presumptive taxation scheme for specified professionals. Under this scheme, eligible professionals can declare 50% of their gross receipts as their income. The gross receipts limit for opting for the presumptive taxation scheme under Section 44ADA is ₹50 lakh. This has been increased to ₹75 lakh from FY 2023-24, provided the cash receipts do not exceed 5% of the total gross receipts.

When does a professional under Section 44ADA need a Tax Audit?

A tax audit is mandatory for a professional who has opted for the presumptive taxation scheme under Section 44ADA, if:

- The professional claims their profits and gains to be lower than the deemed profits (50% of the gross receipts); AND

- The total income of the professional exceeds the basic exemption limit.

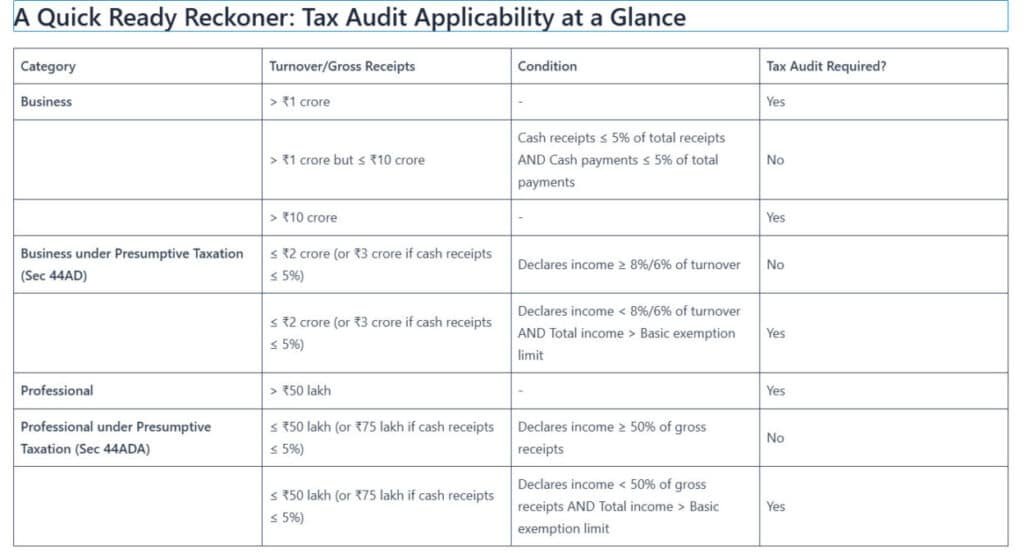

A Quick Ready Reckoner: Tax Audit Applicability at a Glance

| Category | Turnover/Gross Receipts | Condition | Tax Audit Required? |

| Business | > ₹1 crore | – | Yes |

| > ₹1 crore but ≤ ₹10 crore | Cash receipts ≤ 5% of total receipts AND Cash payments ≤ 5% of total payments | No | |

| > ₹10 crore | – | Yes | |

| Business under Presumptive Taxation (Sec 44AD) | ≤ ₹2 crore (or ₹3 crore if cash receipts ≤ 5%) | Declares income ≥ 8%/6% of turnover | No |

| ≤ ₹2 crore (or ₹3 crore if cash receipts ≤ 5%) | Declares income < 8%/6% of turnover AND Total income > Basic exemption limit | Yes | |

| Professional | > ₹50 lakh | – | Yes |

| Professional under Presumptive Taxation (Sec 44ADA) | ≤ ₹50 lakh (or ₹75 lakh if cash receipts ≤ 5%) | Declares income ≥ 50% of gross receipts | No |

| ≤ ₹50 lakh (or ₹75 lakh if cash receipts ≤ 5%) | Declares income < 50% of gross receipts AND Total income > Basic exemption limit | Yes |

Due Date for Filing Tax Audit Report for AY 2025-26

The Original Due Date

The original due date for filing the tax audit report for AY 2025-26 was September 30, 2025.

The Extended Due Date

The Central Board of Direct Taxes (CBDT) has extended the due date for filing the tax audit report for AY 2025-26 to October 31, 2025. This extension has been provided to give relief to taxpayers and tax professionals who were facing difficulties in meeting the deadline due to various reasons, including floods and other natural calamities in several parts of the country.

Consequences of Not Complying with Tax Audit Provisions

Non-compliance with the tax audit provisions can lead to serious consequences.

Penalty for Non-filing or Late Filing of Tax Audit Report (Section 271B)

If a taxpayer fails to get their accounts audited or fails to file the tax audit report by the due date, a penalty can be levied under Section 271B of the Income Tax Act. The penalty will be the lower of the following:

- 0.5% of the total sales, turnover, or gross receipts.

- ₹1,50,000.

However, no penalty will be levied if the taxpayer can prove that there was a reasonable cause for the failure.

Other Consequences of Non-compliance

Apart from the penalty under Section 271B, non-compliance with the tax audit provisions can also lead to:

- Best Judgment Assessment: The Assessing Officer may make a best judgment assessment of the taxpayer’s income.

- Disallowance of certain expenses: Certain expenses may be disallowed if the books of account are not audited.

- Difficulty in getting loans: Banks and financial institutions may be reluctant to grant loans to businesses that have not got their accounts audited.

Conclusion

The tax audit is a critical compliance requirement for businesses and professionals. It is essential to be aware of the criteria for tax audit for AY 2025-26 to avoid penalties and other legal complications. This ready reckoner provides a comprehensive overview of the tax audit provisions, including the turnover limits, the presumptive taxation schemes, the due date for filing the audit report, and the consequences of non-compliance. By understanding and complying with these provisions, you can ensure a smooth and hassle-free tax season. It is always advisable to consult with a qualified Chartered Accountant to ensure that you are in full compliance with the tax laws.

FAQs

I am a salaried individual with a side business. Do I need a tax audit?

Yes, if your turnover from the side business exceeds the prescribed limits, you will have to get your accounts audited. Your salary income will be considered for calculating your total income.

I have incurred a loss in my business. Do I still need a tax audit?

Yes, a tax audit is mandatory if your turnover exceeds the prescribed limits, even if you have incurred a loss.

Can I revise my tax audit report?

Yes, a tax audit report can be revised if there is a genuine mistake or omission. However, it cannot be revised to conceal any income or to claim any fraudulent deduction.

What are the forms for tax audit report?

The tax audit report is to be filed in Form No. 3CA/3CB and 3CD. Form 3CA is for taxpayers whose accounts are required to be audited under any other law, while Form 3CB is for other taxpayers. Form 3CD is a statement of particulars that is to be filed along with the audit report.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.