What is MAT and how to calculate it? MAT, or Minimum Alternate Tax, is a provision in India that requires businesses to pay a minimum amount of tax, even if they employ deductions and exclusions to reduce their taxable revenue to zero or a very small amount. This provision was enacted to discourage firms from dodging taxes despite making large profits.

Section 115JB ensures that companies pay a minimum amount of tax even if they use

deductions and exemptions to reduce their taxable income. This prevents companies from

paying little or no tax despite having high book profits.

Who Needs to Pay MAT?

All companies, including Indian and foreign companies with a presence in India, must pay

MAT if their regular tax is lower than the calculated MAT.

How is MAT Calculated?

A company must pay the higher of the following two amounts:

1. Normal Income Tax (Tax calculated as per regular income tax provisions).

2. MAT = 15% of “Book Profit” + Surcharge + Cess.

Book profit is calculated based on the company’s profit and loss account after making

adjustments as per the law.

Example Calculation of MAT

Let’s assume a company has the following details for the financial year 2024-25:

Book Profit: ₹10 Crore

Normal Tax Calculation: ₹1.5 Crore

Step 1: Calculate MAT

MAT = 15% of Book Profit + 4% Health & Education Cess

MAT = (₹10 Crore × 15%) + 4% of (₹1.5 Crore)

= ₹1.5 Crore + ₹0.06 Crore

= ₹1.56 Crore

Step 2: Compare with Normal Tax

Normal Tax: ₹1.5 Crore

MAT: ₹1.56 Crore

Since MAT (₹1.56 Crore) is higher than Normal Tax (₹1.5 Crore), the company must

pay ₹1.56 Crore as tax.

What Happens to the Extra Tax Paid Under MAT? (MAT Credit)

If a company pays more tax under MAT than normal tax, the extra tax is called MAT

Credit.

MAT Credit can be carried forward for 15 years and used when the company’s

normal tax is higher than MAT in the future.

Example of MAT Credit Usage

In the next financial year (2025-26), if:Normal Tax: ₹3 Crore

MAT: ₹2 Crore

Since normal tax is now higher than MAT, the company can use its MAT Credit of ₹0.06 Crore (₹1.56 Crore – ₹1.5 Crore from the previous year) to reduce its tax liability.

New Tax Payable = ₹3 Crore – ₹0.06 Crore = ₹2.94 Crore.

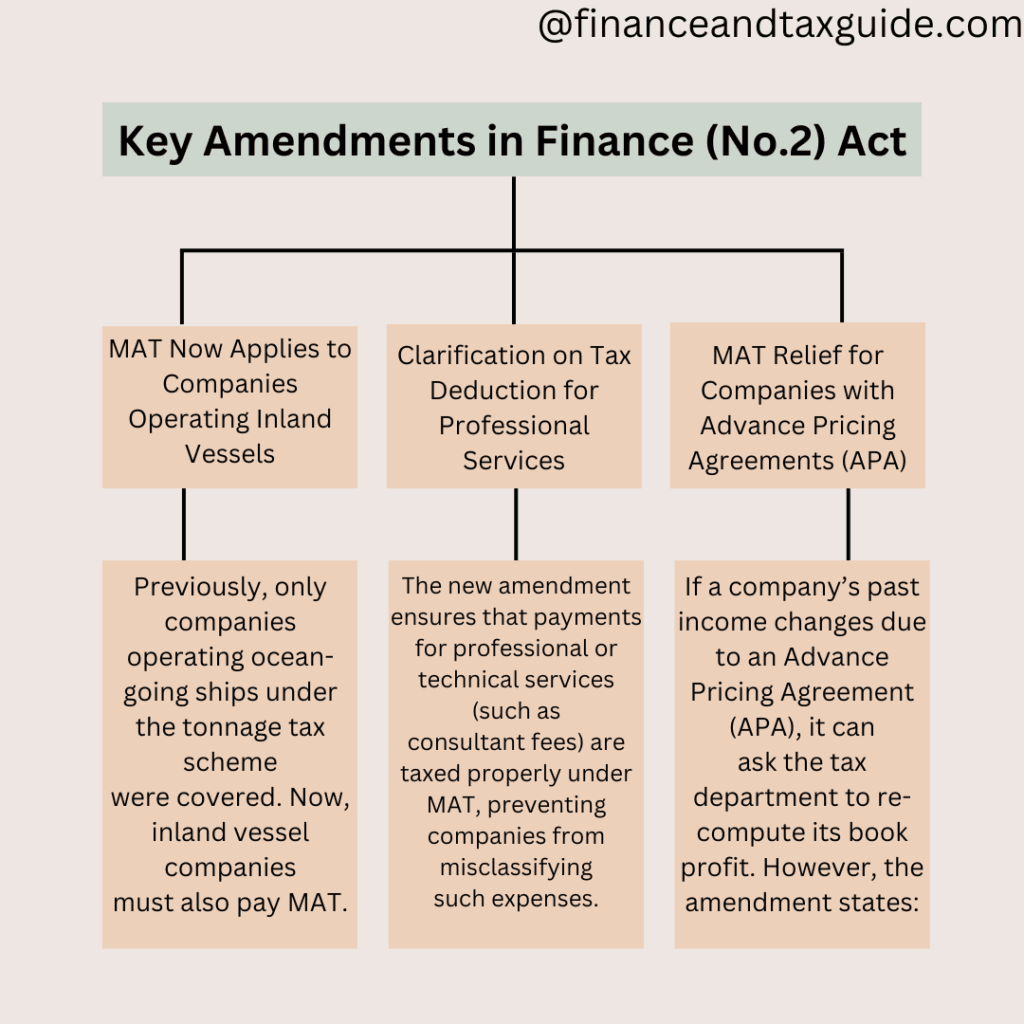

Key Amendments in Finance (No.2) Act, 2024

1. MAT Now Applies to Companies Operating Inland Vessels

Previously, only companies operating ocean-going ships under the tonnage tax scheme

were covered. Now, inland vessel companies (boats, ferries, barges used in rivers/lakes)

must also pay MAT.

2. Clarification on Tax Deduction for Professional Services

The new amendment ensures that payments for professional or technical services (such as

consultant fees) are taxed properly under MAT, preventing companies from misclassifying

such expenses.

3. MAT Relief for Companies with Advance Pricing Agreements (APA)

If a company’s past income changes due to an Advance Pricing Agreement (APA), it can

ask the tax department to re-compute its book profit. However, the amendment states:

If a company already used MAT credit, they cannot claim an adjustment.

No interest refund will be given if MAT tax is reduced due to re-computation.

Conclusion

Section 115JB ensures fair taxation by making companies pay a minimum tax of 18.5% of

book profit. The 2024 amendments clarify tax rules for shipping, professional services, and

past income adjustments. Companies should review these changes to plan their taxes

effectively.

How can i Claim MAT Credit

MAT credit doesn’t get used up in the year it’s paid; instead, it can be carried forward for up to 15 years.

In future years, if the company’s regular tax liability is more than MAT, it can use this credit to reduce the regular tax it has to pay.

Example:

Year 1: A company pays ₹1,00,000 as MAT, but its normal tax liability is only ₹50,000. So, it gets ₹50,000 as MAT credit.

Year 2: The company has to pay ₹2,00,000 as normal tax. It can use ₹1,00,000 of the MAT credit to reduce its tax liability, and the remaining ₹50,000 can be carried forward to the next year.

How to Claim:

The company reports the MAT credit in its tax return, and it can use it in future years when its regular tax is higher than MAT.

In short, MAT credit helps companies recover excess tax paid when their normal tax is lower, and they can use it to reduce future tax bills. However If you are going to adopt new tax regime u/s 115BAB, 115BAA of Income tax act,1961 earlier year’s Mat credit will be lapsed.