Central Goods and Services Tax : The CGST is one of the tax types which are a part of India’s new taxation system which came into existence after the implementation of Good and Services Tax (GST). Created to simplify the system of indirect taxation and to ensure greater compliance, CGST is charged by the Central Government on intra-state supplies of goods and/or services.

What is CGST?

CGST (Central Goods and Services Tax) is a part of India’s GST (Goods and Services Tax) system, introduced in 2017 to simplify indirect taxation. It is levied by the Central Government on intra-state (within the same state) transactions of goods and services.

Key Features of CGST

✅ Collected by the Central Government

✅ Applicable on supply of goods and services within a state

✅ Shared with SGST (State GST) in intra-state sales

✅ Replaced multiple central taxes like Excise Duty, Service Tax, etc.

🔹 Example: If a Mumbai-based company sells goods worth ₹10,000 to a customer in Mumbai, CGST and SGST will apply.

How Does CGST Work?

Under GST, transactions are taxed in two ways:

| Transaction Type | Tax Applicable | Government Share |

| Intra-State (Within State) | CGST + SGST | Central + State Govt. |

| Inter-State (Between States) | IGST | Central Govt. (shared with states) |

CGST Flow Example

- A Delhi manufacturer sells a product for ₹1,00,000 to a Delhi retailer.

- GST rate = 18% (9% CGST + 9% SGST).

- Total GST = ₹18,000 (₹9,000 CGST + ₹9,000 SGST).

- The Central Govt. gets ₹9,000 (CGST) and the Delhi Govt. gets ₹9,000 (SGST).

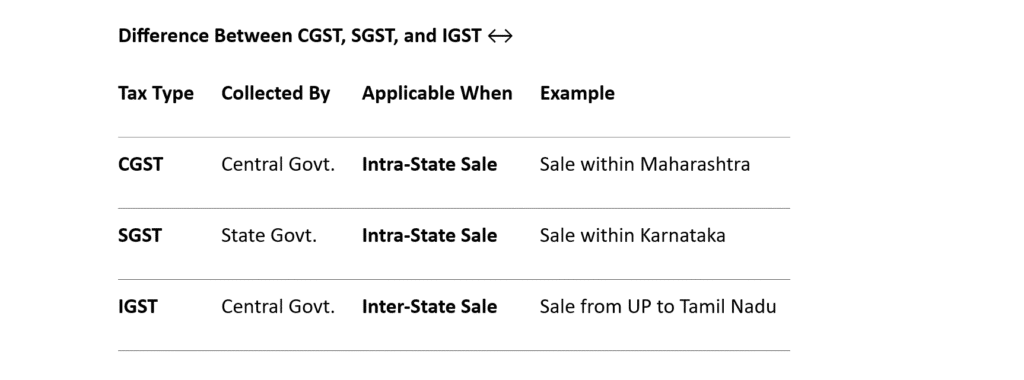

Difference Between CGST, SGST, and IGST

| Tax Type | Collected By | Applicable When | Example |

| CGST | Central Govt. | Intra-State Sale | Sale within Maharashtra |

| SGST | State Govt. | Intra-State Sale | Sale within Karnataka |

| IGST | Central Govt. | Intra-State Sale | Sale from UP to Tamil Nadu |

Example

Intra-State Sale (CGST + SGST)

- Product price: ₹50,000

- GST: 12% (6% CGST + 6% SGST)

- Total tax: ₹6,000 (₹3,000 CGST + ₹3,000 SGST)

Inter-State Sale (IGST)

- Product price: ₹50,000

- IGST: 12%

- Total tax: ₹6,000 (fully to Central Govt.)

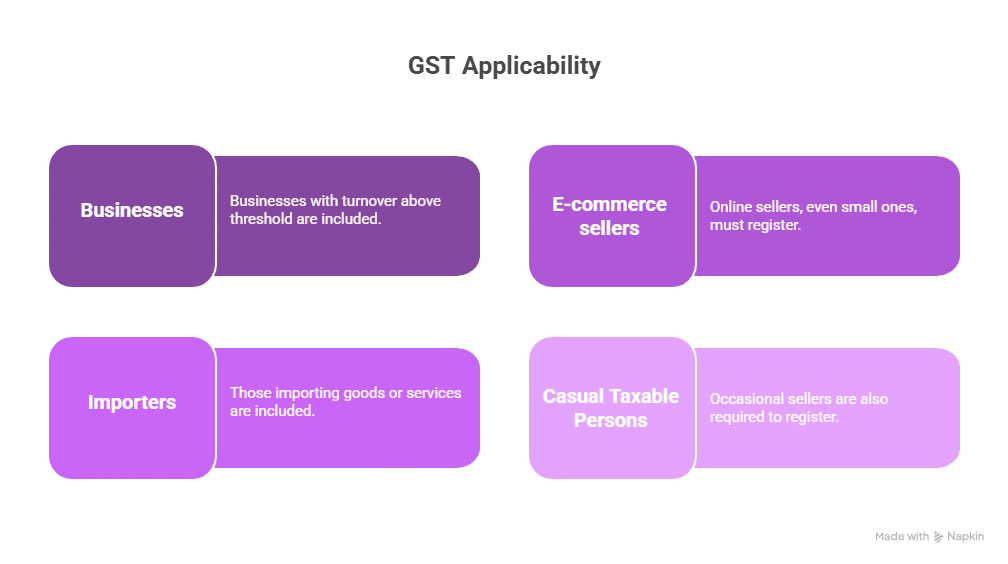

Who Needs to Pay CGST?

✅ Businesses with annual turnover above ₹40 lakhs (₹20 lakhs for some states)

✅ E-commerce sellers (even small sellers)

✅ Importers of goods/services

✅ Casual taxable persons (occasional sellers)

⚠️ Exemptions:

- Small businesses under Composition Scheme (lower tax, no ITC)

- Essential goods like fresh milk, fruits, education, healthcare

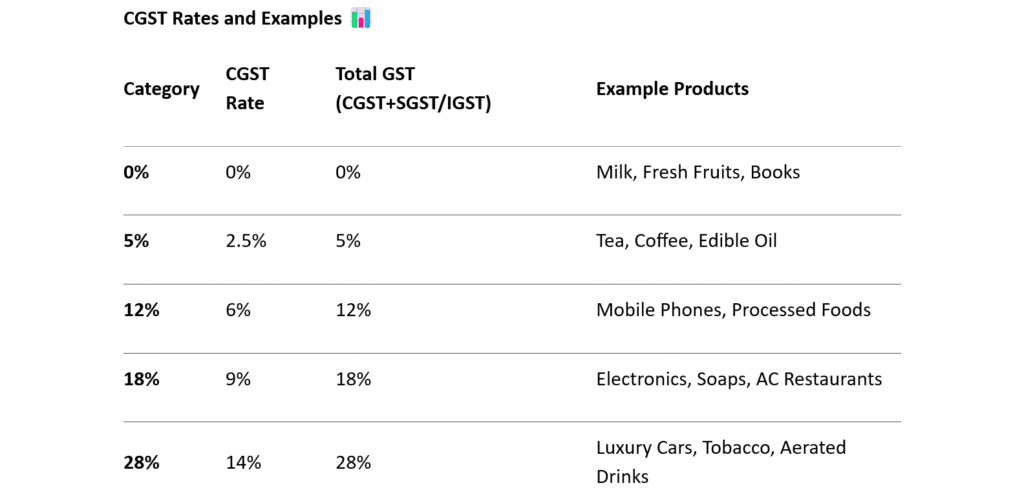

CGST Rates and Examples

| Category | CGST Rate | Total GST (CGST+SGST/IGST) | Example Products |

| 0% | 0% | 0% | Milk, Fresh Fruits, Books |

| 5% | 2.5% | 5% | Tea, Coffee, Edible Oil |

| 12% | 6% | 12% | Mobile Phones, Processed Foods |

| 18% | 9% | 18% | Electronics, Soaps, AC Restaurants |

| 28% | 14% | 28% | Luxury Cars, Tobacco, Aerated Drinks |

Example:

- Mobile Phone Price: ₹20,000

- GST: 12% (6% CGST + 6% SGST)

- Tax Amount: ₹2,400 (₹1,200 CGST + ₹1,200 SGST)

- Final Price: ₹22,400

How to Calculate CGST?

- Formula

text

CGST Amount = (Price × CGST Rate) / 100

Total GST = CGST + SGST (for intra-state)

CGST = (Value of Supply × CGST Rate)

Example Calculation:

- Product Price: ₹80,000

- GST Slab: 18% (9% CGST + 9% SGST)

- CGST: ₹7,200 (9% of ₹80,000)

- SGST: ₹7,200

- Total Tax: ₹14,400

- Final Invoice Amount: ₹94,400

Input Tax Credit (ITC) Under CGST

What is Input Tax Credit (ITC)?

Businesses can claim credit for taxes paid on purchases and reduce their tax liability.

Example:

- Business A buys raw materials for ₹1,00,000 + ₹18,000 GST (9% CGST + 9% SGST)

- Later, sells finished goods for ₹2,00,000 + ₹36,000 GST

- Tax Payable: ₹36,000 GST

- ITC Claimed: ₹18,000 (from purchase)

- Net Tax Paid: ₹18,000

Conditions for ITC:

- Must have a valid GST invoice

- Goods/services must be used for business

- Supplier must have filed GST returns

Filing CGST Returns

Businesses must file monthly/quarterly returns:

- GSTR-1: Outward supplies (sales)

- GSTR-3B: Summary return (tax payment)

- GSTR-9: Annual return

⚠️ Late Fees: ₹50/day (₹20 for nil returns)

Penalties for Non-Compliance ⚠️

| Offense | Penalty |

| Late GST filing | ₹50/day (Max ₹5,000) |

| Tax evasion | 100% of tax due |

| Fraudulent claims | Jail up to 5 years |

Benefits of CGST ✅

✔️ Removes cascading effect (tax on tax)

✔️ Uniform tax rates across India

✔️ Easier compliance with online filing

✔️ Boosts business transparency

Common Misconceptions About CGST

❌ “CGST is an additional tax” → No, it replaces old taxes.

❌ “Small businesses don’t need GST” → Required if turnover > ₹40 lakhs.

❌ “GST increases prices” → Actually reduces tax burden due to ITC.

Conclusion

CGST is a simplified, transparent tax system benefiting businesses and consumers. By understanding rates, ITC, and compliance, taxpayers can avoid penalties and maximize savings

FAQs

What is CGST full form?

CGST stands for Central Goods and Services Tax.

Who collects CGST?

It is collected by the Central Government.

Is CGST applicable on exports?

No, exports are zero-rated under GST.

What happens to CGST in case of inter-state transactions?

In such cases, IGST is levied instead of CGST and SGST.

Can CGST credit be used to pay SGST?

No, CGST credit can only be used for CGST and IGST.

Pro Tip:

Use GST calculators and consult a CA for complex transactions!

📢 Need Help with GST Filing? Contact a Finance and Tax Expert Today! 🚀

This guide simplifies CGST for beginners & businesses. Hope it helps! 👍 Contact Us

🔗 Share this page to spread tax awareness! 📢