Audits play a crucial role in ensuring transparency, compliance, and operational efficiency across organizations. Whether for regulatory requirements, fraud detection, or internal improvements, different types of audits serve distinct purposes.

In this comprehensive guide, we explore all major types of audits, their objectives, and why businesses rely on them.

20 Types of Audit

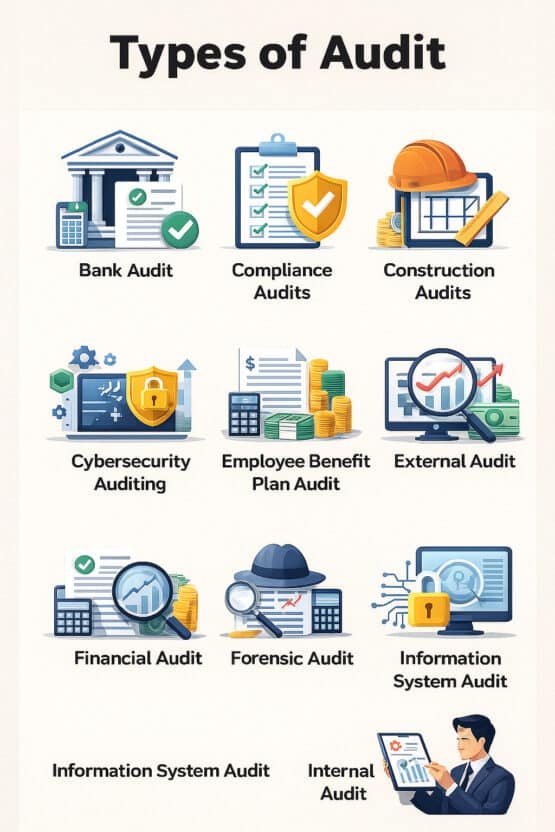

1. Bank Audit

A bank audit reviews a bank’s financial statements and operational processes to ensure compliance with regulatory bodies such as the Reserve Bank of India (RBI). It checks the accuracy of transactions, adherence to banking laws, and risk management practices.

2. Compliance Audits

Compliance audits assess whether an organization follows regulatory requirements, internal policies, and contractual obligations. They are essential in industries with strict governance standards such as healthcare, finance, and manufacturing.

3. Construction Audits

Construction audits examine contracts, project timelines, costs, and payments to ensure that construction projects are executed efficiently. They help detect fraud, overbilling, and inefficiency.

4. Cybersecurity Auditing

Cybersecurity audits evaluate an organization’s security posture. This includes vulnerability assessments, reviewing data protection mechanisms, and ensuring safeguards for sensitive information.

5. Employee Benefit Plan Audit

Required by law for large benefit plans, this audit ensures compliance with ERISA regulations and verifies that employee benefit plans are administered according to legal and plan requirements.

6. External Audit

An external audit is conducted by independent auditors who offer an unbiased opinion on a company’s financial statements. These audits boost credibility and reassure stakeholders of financial accuracy.

7. Financial Audit

This audit examines a company’s financial statements to ensure fairness and compliance with accounting standards. It evaluates records such as balance sheets, income statements, and cash flow statements.

8. Forensic Audit

A forensic audit investigates financial irregularities, including fraud, embezzlement, and other economic crimes. Findings often serve as evidence in court proceedings.

9. Information System Audit

This audit reviews internal controls related to computer systems, IT infrastructure, data integrity, and cybersecurity measures. It ensures the reliability of digital operations.

10. Information Technology Audit

An IT audit is broader than a system audit. It examines IT policies, data security, infrastructure, software controls, and alignment of IT systems with business goals.

11. Integrated Audit

Combining both internal and financial audits, integrated audits provide a holistic view of the accuracy of financial records and the effectiveness of control systems.

12. Internal Audit

Internal audits are conducted by a company’s own internal audit team. Their focus is on improving risk management, internal controls, and governance processes. They also help in identifying operational weaknesses.

13. Investigative Audit

Used to uncover misconduct or misappropriation, investigative audits are initiated when there is suspicion of fraud, legal violations, or disciplinary issues.

14. Operational Audits

Operational audits assess the efficiency and effectiveness of business operations. They highlight opportunities for cost savings, productivity improvements, and workflow enhancements.

15. Payroll Audit

A payroll audit verifies employee compensation, tax withholdings, attendance records, and benefits. It ensures compliance with labor laws and prevents payroll fraud.

16. Performance Audit

Performance audits evaluate whether departments, programs, or initiatives are functioning efficiently, effectively, and economically. The goal is to measure results against performance standards.

17. Special Audit

Special audits are mandated by regulatory authorities like SEBI or RBI when there are specific concerns or irregularities. These audits focus on issues not covered in routine audits.

18. Special Investigations

These involve deep investigations into potential criminal, fraudulent, or unethical behavior. They are often triggered by whistleblower reports or suspicious financial activity.

19. Statutory Audit

A statutory audit is required by law under acts such as the Companies Act or Income Tax Act. It ensures legal compliance and verifies the authenticity of financial statements.

20. Stock Audit

A stock audit involves verifying physical inventory against recorded numbers. It helps identify discrepancies, losses, theft, or accounting errors in inventory management.

21. Tax Audit

A tax audit evaluates compliance with tax laws (e.g., Section 44AB of the Income Tax Act) and verifies the correctness of income declared and deductions claimed. It ensures transparency and accurate tax reporting.

Compliance and Regulatory Audits

These audits focus on adherence to laws, regulations, policies, and contracts.

| Audit Type | Focus and Purpose |

| Bank Audit | Reviews a bank’s financials and operations for compliance with RBI regulations and accuracy. |

| Compliance Audits | Assesses whether an entity adheres to regulatory requirements, internal policies, or contractual obligations. |

| Statutory Audit | A mandatory audit required by law, such as under the Companies Act or Income Tax Act, ensuring financial statements comply with legal requirements. |

| Tax Audit | Examination under tax laws (like Section 44AB of the Income Tax Act in India) to verify the correctness of declared income. |

| Employee Benefit Plan Audit | Required by law for large benefit plans to ensure compliance with ERISA regulations and plan terms. |

Financial and Investigative Audits

These types of audits deal directly with an entity’s financial records and are often used to uncover fraud or malpractice.

| Audit Type | Focus and Purpose |

| External Audit | An independent audit by an outside firm to provide an unbiased opinion on financial statements. |

| Financial Audit | Examination of a company’s financial statements to ensure accuracy and compliance with accounting standards. |

| Forensic Audit | Investigates fraud, embezzlement, or other financial crimes with evidence suitable for court proceedings. |

| Investigative Audit | A special audit to uncover misconduct or misappropriation, often leading to disciplinary or legal action. |

| Special Investigations | Deep dives into suspected criminal or unethical behavior, often triggered by whistleblower reports or audit findings. |

Technology and Security Audits

In the digital age, these audits are vital for protecting data and ensuring systems are reliable.

| Audit Type | Focus and Purpose |

| Information System Audit | Reviews controls related to computer systems, data integrity, and IT infrastructure. |

| Information Technology Audit | A broader audit that includes information system security and also checks IT policies, infrastructure, and data security. |

| Cybersecurity Auditing | Assesses an organization’s security posture, including vulnerability management and protection of sensitive information. |

Internal, Operational, and Specific Audits

These categories cover audits performed internally for improvement, those focused on operational efficiency, and checks on specific areas like construction or payroll.

| Audit Type | Focus and Purpose |

| Internal Audit | Conducted by a company’s internal team to evaluate and improve risk management, control, and governance processes. |

| Integrated Audit | Combines financial and internal control audits to evaluate overall accuracy and control systems together. |

| Operational Audits | Evaluates the efficiency and effectiveness of business operations, often suggesting improvements. |

| Performance Audit | Assesses whether programs or departments are operating efficiently, effectively, and economically. |

| Construction Audits | Examines contracts, costs, and timelines for construction projects to prevent fraud or inefficiency. |

| Payroll Audit | Verifies accuracy in employee compensation, tax withholdings, benefits, and compliance with labor laws. |

| Stock Audit | Verifies physical inventory against records to ensure accuracy and prevent discrepancies. |

| Special Audit | Directed by a regulatory authority (like SEBI or RBI) for specific concerns or suspected irregularities. |

Why Are Audits Important?

Audits enhance:

- Financial accuracy

- Compliance with regulations

- Fraud detection and prevention

- Operational improvements

- Risk management

- Stakeholder trust

Across industries, audits drive accountability, efficiency, and long-term success.

Forensic Audit: The Financial Investigator

A Forensic Audit is much more than a standard financial check. It’s a specialized investigation into financial records to uncover evidence suitable for legal proceedings. Think of it as putting on a detective hat for financial accounts.

- Primary Goal: To investigate fraud, embezzlement, or other financial crimes and to provide evidence that can stand up in a court of law.

- When It’s Used:

- Suspected employee theft or asset misappropriation.

- Insurance claims and disputes.

- Shareholder or partner disputes.

- Calculating economic damages (e.g., in a breach of contract case).

- Key Focus Areas: Tracing the movement of funds, identifying sham transactions, quantifying financial loss, and gathering evidence of intent.

- Output: Unlike a traditional audit that yields an opinion on financial statements, a forensic audit produces a detailed report that serves as evidence, and the auditor may be called upon to be an expert witness in court.

Cybersecurity Auditing: Protecting the Digital Fortress

Cybersecurity Auditing assesses an organization’s systems and practices to ensure the protection of its digital assets and sensitive data. In an era of constant cyber threats, this audit is critical for maintaining business continuity and customer trust.

- Primary Goal: To assess an organization’s security posture, including vulnerability management and the protection of sensitive information.

- When It’s Used:

- To comply with data protection regulations (like GDPR or HIPAA).

- After a security breach or incident.

- Prior to implementing a major system change.

- As a regular check to ensure controls are effective.

- Key Focus Areas:

- Network Security: Firewalls, intrusion detection systems, and access controls.

- Data Protection: Encryption, backup, and recovery procedures.

- Vulnerability Management: Identifying and patching weaknesses in software and systems.

- Physical Security: Controls around data centers and server rooms.

- Output: A report detailing identified vulnerabilities, the risk associated with them, and specific, actionable recommendations for improvement to strengthen the organization’s defense against cyber threats.

Internal vs. External Audit: Two Sides of the Assurance Coin

The two fundamental categories of audit are Internal and External. While they both contribute to the overall governance and control of an organization, their objectives, focus, and reporting lines are distinctly different.

Here is a side-by-side comparison to highlight the differences and complementary nature of these two vital functions:

| Feature | Internal Audit | External Audit |

| Auditor | Typically employees of the organization (or outsourced staff). | An independent third-party firm (like a CPA or Chartered Accountant firm). |

| Primary Objective | To improve risk management, internal controls, and operational efficiency (value-add). | To provide an independent opinion on the fairness and accuracy of financial statements (assurance). |

| Stakeholder / Reporting | Reports to Senior Management and the Audit Committee (internal users). | Reports to Shareholders, Investors, Creditors, and Regulators (external users). |

| Scope of Work | Broad and flexible. Covers finance, operations, compliance, IT, performance, and risk management. | Narrow and specific. Primarily focuses on financial statements and related internal controls over financial reporting. |

| Mandatory Requirement | Optional/Discretionary but considered best practice for governance. | Mandatory for publicly traded companies and often required by statute (e.g., Companies Act). |

| Frequency | Continuous or periodic throughout the year, based on a risk-based plan. | Typically annual, tied to the fiscal year-end and regulatory deadlines. |

| Independence | Independent within the organization (reports to the Audit Committee to avoid undue influence from management). | Fully independent of the organization being audited to ensure objectivity and public trust. |

Conclusion

Understanding different types of audits helps organizations choose the right approach for governance and compliance. Each audit type has a distinct purpose, but together they ensure that businesses operate ethically, efficiently, and in accordance with laws.