India is currently the third-largest startup ecosystem in the world, home to over 100+ unicorns and thousands of soonicorns. However, the narrative has shifted. The “funding frenzy” of 2021 is over. We are now in the era of Sustainable Growth.

If you are reading this, you likely have an idea, an MVP, or early traction, and you are wondering how to fuel the engine. You’ve seen competitors raise millions, and you’ve read the headlines. But the gap between reading about funding and signing a term sheet is massive.

Your competitors might tell you what the stages are. This guide will tell you how to survive them. We will move beyond generic advice and look at the hard data: ticket sizes in INR, equity dilution percentages, and the exact metrics Indian VCs (Venture Capitalists) demand in 2025.

The Golden Rule of Funding:

Money is not the goal; it is the fuel. Raising capital does not mean you have succeeded; it means you have just signed up for a much harder job.

India’s startup landscape is evolving, and understanding the complexities of startup funding in India is crucial for aspiring entrepreneurs. As the market shifts towards Sustainable Growth, it is essential to explore various strategies for investment in startups in India, including how to effectively attract investors who are keen to invest in India startups. This roadmap provides a comprehensive overview of the funding of startups in India, detailing the stages of funding, valuation expectations, and the necessary preparations to successfully fund startups in India. By leveraging this information, entrepreneurs can position themselves for a successful start-up investment in India.

The Pre-Funding Phase: Building the Foundation

Before you even ask for a rupee, you must ensure your vessel is seaworthy. In India, many startups fail to raise simply because their legal or structural foundation is cracked.

Legal Structure Matters

Investors in India almost exclusively invest in Private Limited Companies (Pvt Ltd).

- Proprietorship/Partnership: Investors cannot take equity in these structures easily.

- LLP (Limited Liability Partnership): While possible, VCs prefer Pvt Ltd due to the ease of share transfer and ESOP (Employee Stock Ownership Plan) creation.

Action Item: If you are looking for serious VC money, incorporate as a Private Limited entity under the Companies Act, 2013.

Intellectual Property (IP)

Do you own your code? If you hired a freelancer to build your MVP without a contract assigning the IP to your company, the freelancer owns it. This will kill your funding round during Due Diligence (DD).

- Trademark: Protect your brand name.

- Copyright/Patents: Protect your tech.

The Co-Founder Agreement

This is the “Pre-Nup” of the startup world. What happens if one founder leaves? What is the vesting period?

- Standard Vesting: 4 years with a 1-year cliff. (Meaning, if a founder leaves before 12 months, they get 0% equity).

Stage 1: Bootstrapping & Pre-Seed (The Valley of Death)

Bootstrapping: The hustle

Bootstrapping means funding the business yourself. In India, 90% of startups begin here. You use savings, credit cards, or revenue from consulting gigs to fund the product.

Why Bootstrap?

- Control: You answer to no one.

- Equity: You keep 100%.

- Discipline: Spending your own money forces you to be frugal (called “Jugaad” in the best sense).

The Risks:

- Personal financial ruin.

- Slow growth compared to funded competitors.

Pre-Seed: The “Concept” Round

This is often called the “Friends, Family, and Fools” round. You have a prototype, but maybe no customers.

Key Metrics (India Context):

- Ticket Size: ₹10 Lakhs – ₹1 Crore ($15k – $120k).

- Valuation: ₹5 Cr – ₹15 Cr (Cap).

- Dilution: 5% – 10%.

- Runway Provided: 6 – 12 months.

Who Invests?

- Friends & Family: The easiest money, but the most emotionally risky. Treat this as professional debt/equity.

- Incubators/Accelerators:

- Examples: Y Combinator (Global), Sequoia Surge, T-Hub (Hyderabad), NSRCEL (IIM Bangalore).

- Value: They provide office space, mentorship, and a small check (e.g., $25k-$100k) for 5-7% equity.

- Micro-Angels: High Net-worth Individuals (HNIs) who write small checks (₹2L – ₹5L).

The Pitch Focus: At this stage, investors invest in YOU (the founder) and the Market Size. They know the product will change. They need to believe you are the person to solve this specific problem.

Stage 2: Seed Funding (Product-Market Fit)

This is the first “Institutional” round. You have moved past the idea phase. You have an MVP, and you have some early adopters using it. You need money to figure out “Product-Market Fit” (PMF).

What is Product-Market Fit?

It means being in a good market with a product that can satisfy that market.

- Sign: Users are disappointed if your product disappears.

- Metric: High retention rates, organic word-of-mouth.

The Metrics

- Ticket Size: ₹2 Crore – ₹15 Crore ($250k – $2M).

- Valuation: ₹20 Cr – ₹60 Cr.

- Dilution: 10% – 20%.

- Runway: 12 – 18 months.

The Investors

- Angel Networks: Groups of angels who syndicate deals.

- Examples: Indian Angel Network (IAN), Mumbai Angels, LetsVenture, AngelList India.

- Micro VCs: Small funds dedicated to early-stage.

- Examples: Blume Ventures, Kae Capital, Better Capital.

- Super Angels: Successful founders investing back (e.g., Kunal Shah, Binny Bansal).

Documentation Required

- Pitch Deck: 10-12 slides (Problem, Solution, Market, Team, Traction).

- Financial Model: A 1-2 year projection (though investors know it’s a guess).

- Cap Table: Who owns what currently.

Strategy to Win Seed Funding: Demonstrate a “unique insight.” Why is this problem unsolved? Why now? Do not just show growth; show engagement. 1,000 users who love you is better than 10,000 who downloaded and deleted.

Stage 3: Series A (The Engine of Growth)

This is the “Great Filter.” Many startups raise Seed, but few make it to Series A. In India, Series A is where you move from “figuring it out” to “scaling what works.”

The Shift in Mindset

- Seed: “Look at this cool product.”

- Series A: “Look at this money-making machine.”

Investors need to see Unit Economics. This means:

- CAC (Customer Acquisition Cost): How much does it cost to get a user? (e.g., ₹500).

- LTV (Lifetime Value): How much do they pay you over time? (e.g., ₹2,000).

- Ratio: An LTV:CAC ratio of 3:1 is the industry standard.

The Metrics

- Ticket Size: ₹20 Crore – ₹80 Crore ($3M – $10M).

- Valuation: ₹100 Cr – ₹400 Cr.

- Dilution: 15% – 25%.

- Runway: 18 – 24 months.

The Investors (The Big Boys)

These are Tier-1 Venture Capital firms.

- Examples: Peak XV (formerly Sequoia India), Accel, Lightspeed, Matrix Partners, Elevation Capital.

Due Diligence (DD)

At Series A, DD is brutal. They will audit:

- Tech: Is your code scalable? Is it secure?

- Legal: Are all compliances (GST, RoC filings) clean?

- Financial: Forensic audit of every rupee spent.

- Customer Calls: They will literally call your customers to ask if they like you.

Pro Tip: Start organizing your “Data Room” (a Google Drive folder with all legal/finance docs) 3 months before you fundraise.

Stage 4: Series B & C (Hyper-Scaling)

If Series A is about fueling the engine, Series B and C are about putting the pedal to the metal. You are likely generating significant revenue (₹10 Cr+ ARR – Annual Recurring Revenue).

Series B: Expansion

- Goal: Taking the proven model to new cities, new demographics, or adding adjacent product lines.

- Ticket Size: $15M – $50M.

- Risk: Execution risk. Can you manage a team of 200 people? Can you maintain culture?

Series C: Market Dominance

- Goal: Crushing competitors, international expansion, or acquiring smaller companies (M&A).

- Ticket Size: $50M – $100M+.

- Investors: Late-stage VCs (SoftBank, Tiger Global) and Private Equity (PE) firms beginning to take interest.

The “Down Round” Phenomenon

In the current economic climate (2024-2025), valuations have corrected. If you raised Series B at a $500M valuation but can only raise Series C at $400M, that is a Down Round.

- Consequence: Anti-dilution clauses kick in (see section 9), severely hurting the founders’ equity.

- Strategy: Focus on profitability over “growth at all costs” to avoid needing cash when the market is down.

Stage 5: Series D, Late Stage & IPO (The Exit)

This is the endgame. At this point, the startup is a “Unicorn” (Valuation > $1B) or a “Soonicorn.”

Pre-IPO / Series D+

Funding here is often about cleaning up the balance sheet before going public.

- Investors: Hedge Funds, Sovereign Wealth Funds (GIC, Temasek), Mutual Funds.

IPO (Initial Public Offering)

Going public in India involves listing on the BSE (Bombay Stock Exchange) or NSE (National Stock Exchange).

The Process:

- Hire Merchant Bankers: (e.g., Kotak, Morgan Stanley).

- DRHP Filing: Draft Red Herring Prospectus submitted to SEBI (Securities and Exchange Board of India).

- Roadshow: Pitching to institutional investors to build the “book.”

- Listing: The bell rings.

Pros of IPO:

- Massive capital influx.

- Liquidity for early investors and employees (ESOPs).

- Prestige and trust.

Cons of IPO:

- Public Scrutiny: Every quarter, you must report earnings. If you miss by 1%, your stock tanks.

- Compliance: Massive regulatory burden.

Alternative Exits:

- M&A (Merger & Acquisition): Selling to a giant (e.g., Walmart buying Flipkart). This is actually the most common exit, not an IPO.

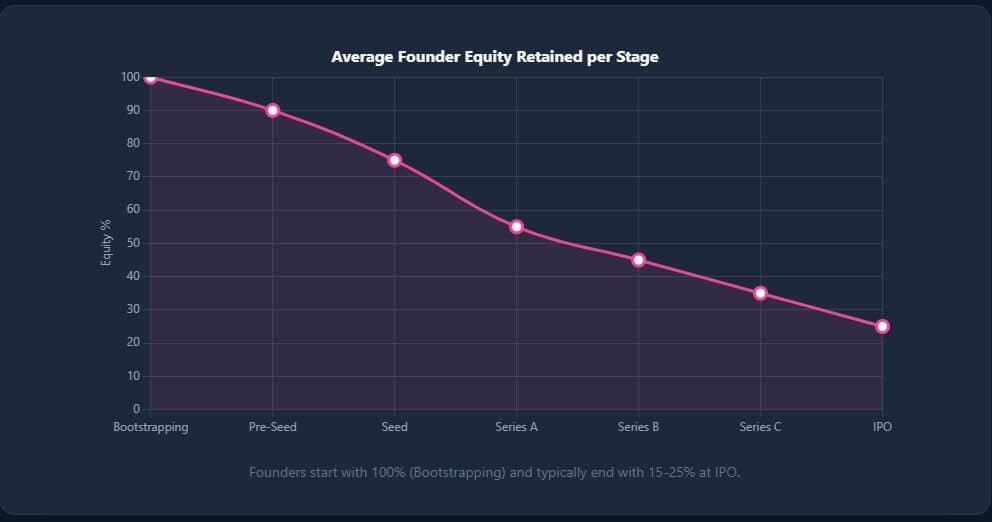

The Mathematics of Funding: Valuation & Dilution

This is where founders often get cheated. You must understand the math.

Pre-Money vs. Post-Money

- Pre-Money Valuation: What your company is worth before the cash hits the bank.

- Investment: The cash investors put in.

- Post-Money Valuation: Pre-Money + Investment.

Example:

- Investor offers ₹10 Cr for 20% equity.

- Post-Money: ₹10 Cr / 0.20 = ₹50 Cr.

- Pre-Money: ₹50 Cr – ₹10 Cr = ₹40 Cr.

Trap: If you agree to “₹40 Cr Valuation” without specifying “Pre-money,” the investor might treat it as “Post-money,” meaning you give up more equity than planned.

The Option Pool Shuffle

Investors will ask you to set aside an ESOP pool (usually 10-15%) for employees.

- The Trap: They will ask you to create this pool from the Pre-Money valuation. This means the dilution comes 100% from the Founders, not the new investors.

- The Fix: Negotiate to create the pool Post-Money (rarely accepted) or simply be aware that a “20% dilution” is actually “20% + 10% ESOP = 30% dilution.”

Decoding the Term Sheet: What VCs Actually Sign

A Term Sheet is a non-binding intent to invest. It contains the financial and governance terms.

Liquidation Preference (The Most Dangerous Clause)

This determines who gets paid first if the company is sold.

- 1x Non-Participating: (Standard/Good). The investor gets their money back OR their % of the company, whichever is higher.

- 2x Participating: (Bad). The investor gets 2x their money back FIRST, AND THEN they also split the remaining money based on equity. Avoid this at all costs.

Anti-Dilution

Protection for investors if you raise money later at a lower valuation (Down Round).

- Full Ratchet: (Deadly). The investor gets repriced as if they invested at the new low price. Founders get washed out.

- Weighted Average: (Standard). A mathematical formula that adjusts the price fairly.

Board Seats

Who controls the company?

- Seed: Usually no board seat, maybe an “Observer.”

- Series A: 1 Board seat for the lead investor.

- Control: Ensure Founders retain board control (e.g., 2 Founder seats vs 1 Investor seat).

Alternative Funding: Debt, Grants & RBF

Not all money costs equity. In India, alternative financing is booming.

Venture Debt

- What is it? A loan for startups. Unlike a bank loan, they don’t ask for collateral (property). They look at your VC backing.

- Players: Stride Ventures, Trifecta Capital, Alteria.

- Use Case: Buying inventory, funding working capital, extending runway between rounds.

- Cost: Interest rate (12-15%) + minimal equity warrants.

Revenue Based Financing (RBF)

- What is it? You get upfront cash in exchange for a % of your future monthly revenue until the loan is paid + a flat fee.

- Players: Klub, Recur.

- Perfect for: D2C brands with predictable sales but high inventory costs.

- Pros: 0% Equity Dilution.

Government Grants

- Startup India Seed Fund Scheme (SISFS): Grants up to ₹20 Lakhs for validation and ₹50 Lakhs for commercialization.

- NIDHI-PRAYAS: Grants for hardware startups.

Why Investors Say Red Flags

If you are getting rejected, check this list.

- Small Market: “This is a nice lifestyle business, but not a venture-scale business.” (VCs need 100x returns).

- Solo Founders: Statistically, solo founders fail more. VCs love a Hacker (Tech) + Hustler (Sales) duo.

- Cap Table Issues: If a dead co-founder or an uncle owns 30% of your company for doing nothing, VCs won’t invest.

- No “Moat”: If Google can build your product in a weekend, you are defenseless.

- Vanity Metrics: Focusing on “App Downloads” instead of “Daily Active Users.”

- Broken Unit Economics: Selling a ₹100 product that costs ₹150 to acquire.

- Tech Outsourcing: For a tech startup, the tech must be in-house.

- Lack of Focus: “We are doing B2B and B2C and also an API.” (Do one thing effectively).

- Dishonesty: Hiding bad data. Due diligence will find it, and you will be blacklisted.

- Not Knowing Your Numbers: If you stutter when asked about your Burn Rate or CAC, the meeting is over.

Conclusion – Startup funding in india

Funding is a staircase. You cannot jump from the ground floor to the penthouse. Each stage requires a different version of you as a founder.

- Pre-Seed: Be a Dreamer.

- Seed: Be a Builder.

- Series A: Be a Manager.

- Series B+: Be a Leader.

The Indian startup ecosystem is resilient. While the “easy money” is gone, there is more capital available for good businesses than ever before. Focus on building a business that can survive without funding, and you will find that funding becomes much easier to get.

Disclaimer: This guide is for educational purposes. Always consult with legal and financial professionals before signing investment documents.

FAQs

How long does it take to raise funding in India?

Seed: 3 to 6 months.

Series A: 6 to 9 months.

Always plan for 9 months of runway before you start pitching.

Do I need a CA (Chartered Accountant) to raise funds?

Yes. You need a CA for valuation certificates, company incorporation, and due diligence. Do not try to DIY your finances.

What is the difference between an Angel and a VC?

Angel: Invests their own money. Faster decisions. Emotional connection.

VC: Invests other people’s money (LPs). Slower, rigorous diligence, strictly metrics-driven.

How much equity should founders have at Series A?

Ideally, the founding team should still own 50-60% of the company after Series A. If you own less than 30% at Series A, you may lose motivation (and VCs know this).

Can I raise funding with just an idea?

In 2025? Rarely. Unless you are a second-time founder with a successful exit, you need an MVP and early traction.