Book Profit is the adjusted net profit of a company, calculated based on its Profit & Loss

Account as per the Companies Act, 2013, with specific additions and deductions under

Section 115JB.

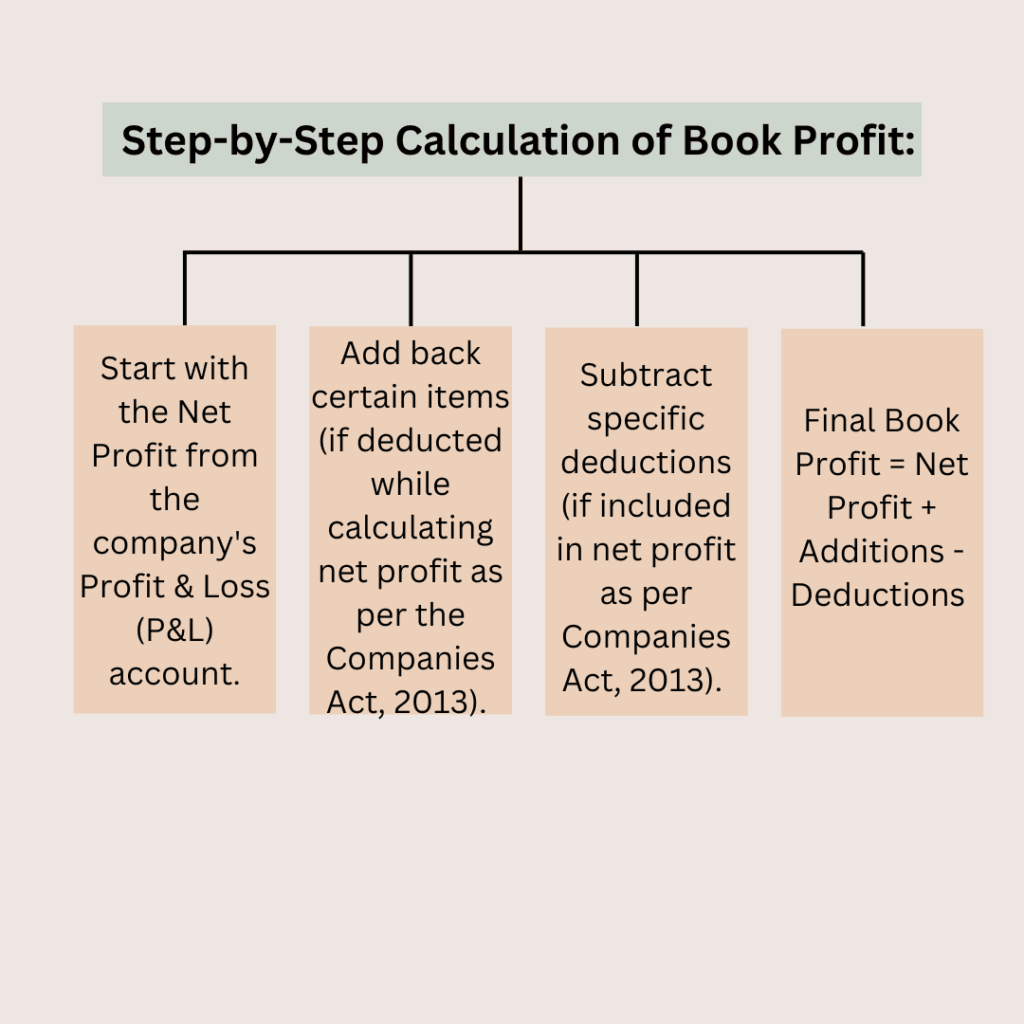

Step-by-Step Calculation of Book Profit:

- Start with the Net Profit from the company’s Profit & Loss (P&L) account.

- Add back certain items (if deducted while calculating net profit as per the Companies Act, 2013).

- Subtract specific deductions (if included in net profit as per Companies Act, 2013).

- Final Book Profit = Net Profit + Additions – Deductions

Detailed Additions and Deductions for Book Profit Calculation

A) Add Back to Net Profit (If Already Deducted)

The following amounts must be added back to the net profit:

- Income Tax Paid or Payable (including MAT itself).

- Dividends Paid or Proposed by the company.

- Amounts transferred to any Reserve/Fund (except Depreciation Reserve).

- Provisions for Losses of Subsidiary Companies.

- Deferred Tax and Other Provisions.

- Depreciation (if charged to P&L Account but needs re-computation).

- Expenditure related to Exempt Income (like agricultural income).

- Amounts of revaluation reserve adjustments (if credited to P&L account).

B) Deduct from Net Profit (If Already Included)

The following amounts must be subtracted from the net profit:

- Income Exempt from Tax (like agricultural income, dividend from foreign

subsidiaries, etc.). - Amount Withdrawn from Reserves, if credited to P&L.

- Depreciation as per Income Tax Act (instead of Companies Act depreciation).

- Long-Term Capital Gains (if not taxable under normal provisions).

- Income from Life Insurance Business.

- Share of Profit from Partnership Firm (if already included in P&L).

Example of Book Profit Calculation

Let’s assume a company’s Profit & Loss Account shows the following details for the financial

year:

- Net Profit before tax: ₹10 Crore

- Additions:

- Income Tax Paid = ₹50 Lakh

- Transfer to General Reserve = ₹1 Crore

- Depreciation as per Companies Act = ₹2 Crore

- Deductions:

- Dividend from a foreign subsidiary (Exempt Income) = ₹1.5 Crore

- Depreciation as per Income Tax Act = ₹1.8 Crore

Step 1: Add Back Items

- Net Profit: ₹10 Crore

- Add ₹50 Lakh (Income Tax Paid)

- Add ₹1 Crore (Reserve Transfer)

- Add ₹2 Crore (Companies Act Depreciation)

- Total after Additions = ₹13.5 Crore

Step 2: Deduct Eligible Items

- ₹13.5 Crore

- Deduct ₹1.5 Crore (Exempt Dividend Income)

- Deduct ₹1.8 Crore (Depreciation as per Income Tax Act)

- Final Book Profit = ₹10.2 Crore

Final MAT Calculation Based on Book Profit

Now, applying MAT @15% on ₹10.2 Crore:

- MAT = 15% of ₹10.2 Crore = ₹1.53 Crore

- 4% Health & Education Cess = ₹0.0612 Crore

- Total MAT Payable = ₹1.5912 Crore

Conclusion about Book Profit

Book Profit Calculation is crucial for MAT computation under Section 115JB. By following

these steps and the addition and deduction rules, companies can correctly compute their

MAT liability and optimize their tax planning for the relevant assessment year.

Pingback: Quick Overview of Section 115JB - Finance And Tax Guide

Thanks for your comment! 😊

Section 115JB makes sure companies pay at least a minimum amount of tax based on their book profit, which is the profit shown in their financial statements. Some adjustments are made according to the tax rules, but the main idea is that even if a company shows low taxable income, it still pays tax if it has high book profits.

Just to clarify, book profit is different from regular income. Regular income is what’s calculated after deductions and exemptions. When deciding how much tax to pay, the company compares the tax calculated on regular income vs. book profit. It must pay the higher amount.

So, Section 115JB ensures that companies with big book profits don’t avoid paying taxes, even if their regular income is low.

Hope this clears things up! Let us know if you have more questions! 🤔