Section 69C of the Income Tax Act of 1961 is an important anti-tax evasion provision that addresses unexplained expenditure. If you incur expenses that you cannot justify with legal income or financial records, the Income Tax Department may classify those expenses as presumed income and assess tax at the highest relevant rate. This part discourages unexplained transactions while encouraging financial transparency and compliance.

What is Section 69C?

Section 69C of the Income Tax Act, 1961, deals with “Unexplained Expenditure” – where a taxpayer incurs expenses but cannot explain the source of funds used.

- Objective: To tax money spent without a legitimate income source.

- Applicability: When expenses are disproportionate to declared income.

🔹 Example:

- Mr. X spends ₹20 lakhs on a wedding but shows only ₹5 lakhs income.

The IT Department can tax the ₹15 lakh unexplained expenditure under Section 69C.

When Does it Apply?

Section 69C applies if:

✅ Expenses are incurred but not recorded in books (if books are maintained).

✅ Taxpayer cannot explain the source of funds.

✅ Expenses exceed declared income.

⚠️ Exceptions:

- If the expense is from loans, gifts, or savings (with proof).

Objective of Section 69C

The section requires to:

- Discourage black money transactions.

- Promote transparency and accountability in financial transactions.

- To ensure equitable taxation, bring unreported income under tax.

Key Conditions for Taxability

For Section 69C to apply, the IT Department must establish:

- Existence of expenditure (weddings, travel, luxury purchases).

- No recording in books (if books are maintained).

- No satisfactory explanation of the fund source.

🔹 Example:

- A taxpayer spends ₹50 lakhs on foreign trips but shows only ₹10 lakhs income.

- The ₹40 lakh difference can be taxed under Section 69C.

Types of Expenses Covered

| Expense Type | Examples |

| Luxury Purchases | Cars, jewellery, designer clothes |

| Travel | Foreign trips, 5-star stays |

| Events | Weddings, parties |

Burden of Proof

| Party | Responsibility |

| IT Department | Must prove the expense exists and is unrecorded. |

| Taxpayer | Must show fund source (savings, loans, gifts). |

⚠️ If taxpayer fails to explain, the expense is taxed as income.

How to Avoid Falling Under Section 69C

- Keep accurate records on all financial transactions.

- Keep all bank statements, invoices, and receipts.

- Ensure that major purchases are supported by legal and stated income.

- Make sure your returns are accurate and include all necessary disclosures.

Tax Treatment & Penalties

- Tax Rate: Unexplained expenditure is taxed at normal slab rates (up to 30%).

- Penalty: Up to 100% of tax evaded (under Section 271(1)(c)).

🔹 Example:

- Unexplained expenses: ₹25 lakhs

- Tax @30%: ₹7.5 lakhs

- Penalty (if applied): Up to ₹7.5 lakhs

- Total liability: ₹15 lakhs

How to Avoid Section 69C Notices?

✔️ Maintain expense records (bills, bank statements).

✔️ Explain large expenses (e.g., wedding from savings).

Difference Between Section 69, 69A, 69B, 69C

| Section | Applies To |

| 69 | Unexplained investments |

| 69A | Unexplained money/jewellery |

| 69B | Undisclosed investments |

| 69C | Unexplained expenses |

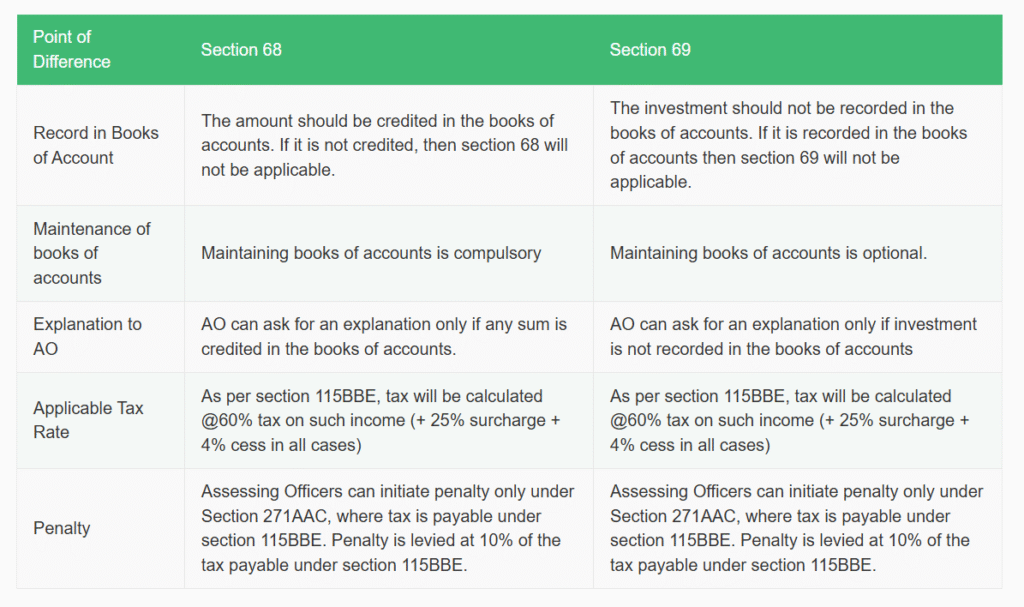

What is the Difference Between Section 68 and Section 69?

Case Laws & Examples

- CIT vs. Smt. P.K. Noorjahan (1999):

- Unexplained wedding expenses were taxed under Section 69C.

🔹 Example:

- A politician spends ₹2 crores on a rally but shows ₹20 lakhs income.

- If unexplained, ₹1.8 crores is taxable under Section 69C.

Conclusion

- Section 69C targets unexplained expenses without a legitimate income source.

- Taxpayers must justify large expenditures.

📌 Pro Tip: Keep loan agreements, gift deeds, and bank records for big expenses!

🔗 Need help? Consult a CA!

FAQs

What is the tax rate on unexplained expenditure under Section 69C?

Unexplained expenditure is taxed at the maximum marginal rate, currently 30% plus applicable cess and surcharge.

Can deductions be claimed against income added under Section 69C?

No. No deductions or set-offs are allowed against such income.

Who has the burden of proof under Section 69C?

The taxpayer must prove the source of the expenditure.

Is Section 69C applicable to cash transactions only?

No. It applies to all kinds of unexplained expenditures, not just cash.