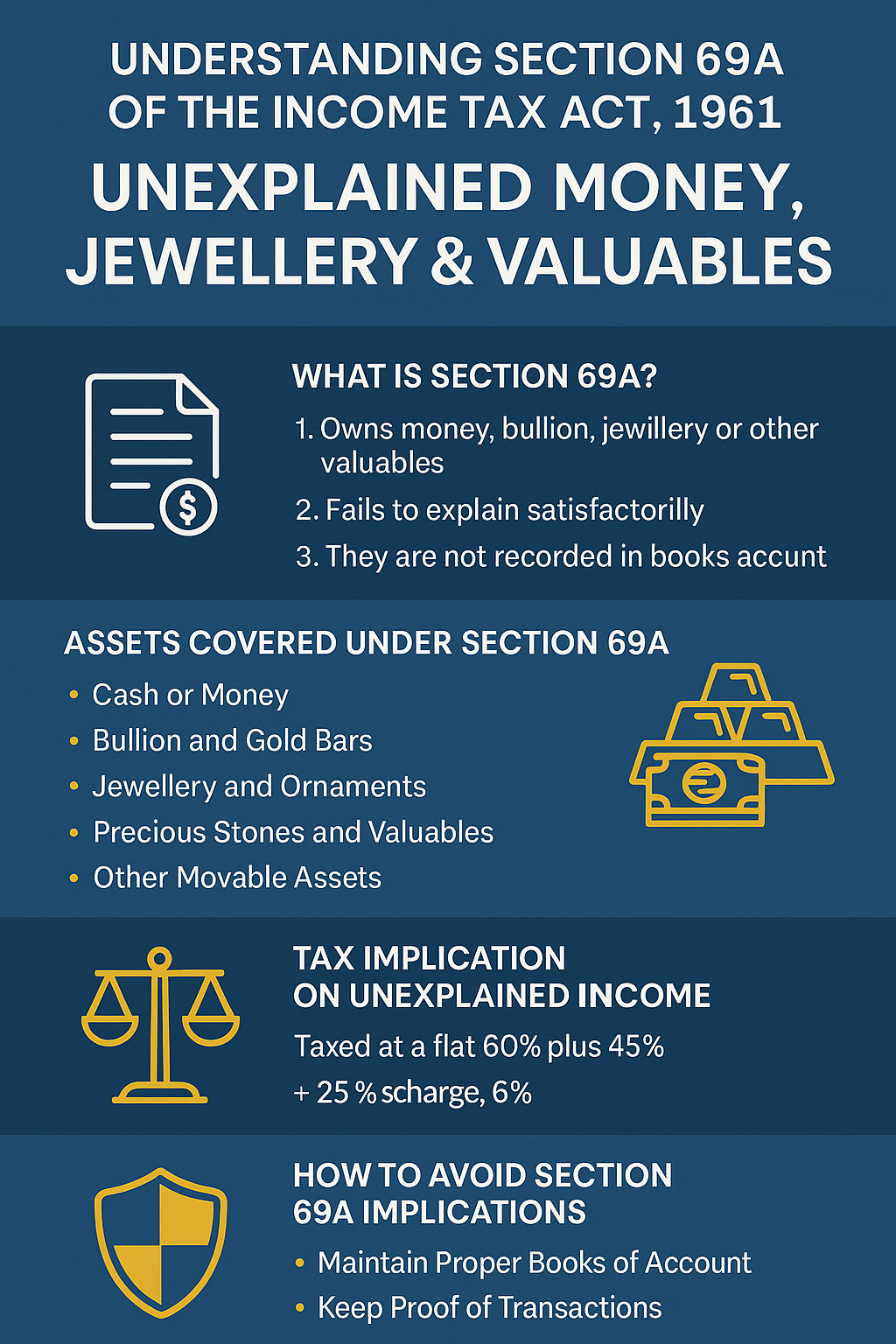

When the Income Tax Department identifies unexplained money such as money, bullion, or jewels that a person fails to explain properly, Section 69A of the Income Tax Act of 1961 is invoked. This provision aims to provide taxpayers with greater transparency and accountability for high-value unexplained assets. If these valuables are not recorded in the books of accounts and lack a reliable source, they may be considered unexplained income and taxed accordingly.

What is Section 69A?

Section 69A of the Income Tax Act, 1961, deals with “Unexplained Money, Jewellery, or Other Valuables” found in the possession of a taxpayer that are not recorded in books of accounts (if maintained) and for which no satisfactory explanation is provided.

- Objective: To tax undisclosed assets like cash, gold, diamonds, or any high-value items.

- Applicability: When such assets are discovered during income tax raids, surveys, or scrutiny.

🔹 Example:

- During a search, ₹50 lakhs in cash is found in Mr. X’s locker, but he has no proof of its source.

- The IT Department can treat this as unexplained money and tax it under Section 69A.

When Does Section 69A Apply?

Section 69A applies if:

✅ Money, jewellery, or valuables are found in possession (cash, gold, diamonds, etc.).

✅ No recording in books (if books are maintained).

✅ Taxpayer fails to explain the source (or explanation is unsatisfactory).

⚠️ Exceptions:

- If the asset is inherited or received as a gift (with proper documentation).

- If the taxpayer provides valid proof (bank withdrawals, sale deeds, etc.).

Key Conditions for Taxability

For an amount to be taxed under Section 69A, the IT Department must establish:

- Physical possession of money/jewellery/valuables.

- No recording in books (if books are maintained).

- No satisfactory explanation of the source.

🔹 Example:

- A taxpayer has 10 kg gold but no purchase bills or income proof.

- The IT Department can treat this as unexplained investment and tax it under Section 69A.

Types of Assets Covered

Section 69A applies to the following:

- Cash or Money

- Bullion and Gold Bars

- Jewellery and Ornaments

- Precious Stones and Valuables

- Other Movable Assets

| Asset Type | Examples |

| Cash | Unexplained money in bank or physical cash |

| Jewellery | Gold, diamonds, platinum, silver |

| Other Valuables | Paintings, antiques, luxury watches |

⚠️ Note: Even demonetized cash found during raids can be taxed under Section 69A if unexplained.

Burden of Proof

| Party | Responsibility |

| IT Department | Must prove the asset exists and is unrecorded. |

| Taxpayer | Must provide a valid source (sale, inheritance, gift, etc.). |

⚠️ If the taxpayer fails to explain, the value is added to income and taxed.

Tax Treatment & Penalties

- Tax Rate: Unexplained assets are taxed at normal slab rates (up to 30%).

- Penalty: Up to 100% of tax evaded (under Section 271(1)(c)).

- Interest: 12% p.a. under Section 234A/B.

🔹 Example:

- Unexplained jewellery worth ₹20 lakhs found.

- Tax @30%: ₹6 lakhs

- Penalty (if applied): Up to ₹6 lakhs

Total liability: ₹12 lakhs

How to Avoid Section 69A Notices?

✔️ Maintain proper records of high-value purchases.

✔️ Declare all assets in ITR.

✔️ Keep proof (bills, bank statements, gift deeds).

✔️ Explain large cash deposits (if from savings, sale of assets, etc.).

Difference Between Section 69, 69A, 69B, 69C

| Section | Applies To |

| 69 | Unexplained investments (property, shares) |

| 69A | Unexplained money, jewellery, valuables |

| 69B | Undisclosed investments (value higher than recorded) |

| 69C | Unexplained expenses (no source of funds) |

Case Laws & Examples

- CIT vs. K. Chinnathamban (2003):

- Mere possession of jewellery without bills does not always attract Section 69A if a reasonable explanation is given.

- Poonamchand vs. ITO (2018):

- Cash found during a raid was taxed under Section 69A as the taxpayer failed to explain the source.

🔹 Example:

- A businessman has ₹1 crore in cash but shows only ₹10 lakhs income.

- If he cannot explain, ₹90 lakhs is taxable under Section 69A.

Conclusion

- Section 69A targets unexplained cash, gold, and valuables to curb black money.

- Taxpayers must maintain proof of high-value assets.

- Legal advice is recommended if facing a Section 69A notice.

📌 Pro Tip: Always keep purchase bills, gift deeds, and bank records for high-value assets!

🔗 Need help with tax notices? Consult a Us!

FAQs

Is agricultural income considered a valid explanation?

Only if supported by valid documents like land records and crop sale receipts.

Are gifts taxable under Section 69A?

If not properly documented, high-value gifts may be treated as unexplained income.

Can jewellery received during marriage be taxed?

Generally exempt if reasonable and supported by gift deeds or family tradition evidence.

Can penalty be avoided if the taxpayer voluntarily declares the asset later?

No. Once found in search/survey, it’s taxable under special provisions.