When builders or developers sell real estate at a price lower than the market (stamp duty) value, the Income Tax Act doesn’t stay silent. That’s where Section 43CA steps in.

This section ensures that businesses dealing in real estate can’t understate their sales to avoid taxes.

📘 What is Section 43CA of the Income Tax Act?

Section 43CA applies when a person sells land or building (or both) held as stock-in-trade, and the actual sale consideration is less than the Stamp Duty Value (SDV).

In such cases, the SDV is deemed to be the actual sale value, and the profit is calculated accordingly — increasing the taxable business income.

📌 This provision is applicable to developers, builders, property dealers, and anyone selling real estate not as an investment, but as part of their business.

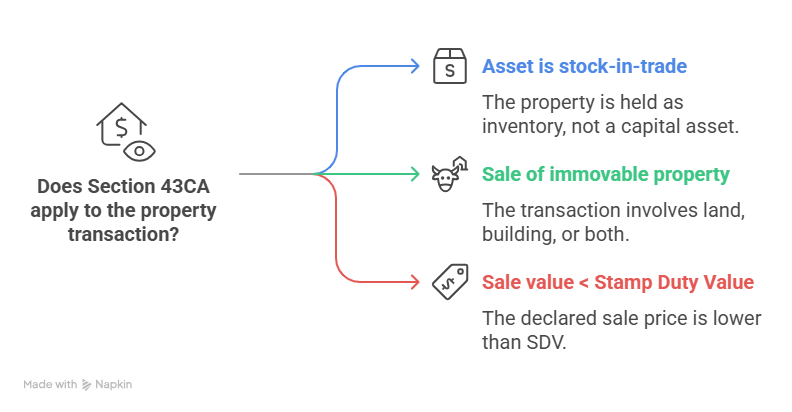

🏗️ Key Conditions for Section 43CA to Apply:

| Condition | Explanation |

| Asset is stock-in-trade | The land/building is part of the business inventory, not a capital asset. |

| Sale of immovable property | Property transferred must be land, building, or both. |

| Sale value < Stamp Duty Value | Declared sale consideration is less than SDV on the date of agreement or registration. |

📆 Date of Agreement vs. Date of Registration

If part of the payment is received by cheque, bank transfer, or digital mode on or before the agreement date, the SDV as on the date of the agreement is considered, not registration date.

This helps sellers avoid tax consequences due to valuation hikes between agreement and registration.

📉 Safe Harbour Provision – Tolerance Limit

To provide relief in cases where the SDV is marginally higher than the actual sale price, a 10% variation is allowed.

| If SDV is… | Taxable value |

| Up to 110% of actual consideration | Actual sale value |

| More than 110% of actual consideration | Stamp Duty Value |

🧮 Example

Sale Price: ₹80,00,000

SDV: ₹85,00,000 (6.25% higher)

✅ Since difference < 10%, actual price is accepted.

But if SDV was ₹90,00,000 → Difference = 12.5% → SDV becomes deemed sale value.

📊 Real-Life Example

A builder sells a flat to a customer:

- Declared Sale Price: ₹50 lakh

- Stamp Duty Value: ₹60 lakh

- Difference: ₹10 lakh → 20%

- ✅ As this is beyond the 10% limit, the sale is deemed at ₹60 lakh.

Business income will be calculated on ₹60 lakh, not ₹50 lakh.

⚖️ Option to Refer to Valuation Officer

If the seller believes that the SDV is higher than the fair market value, they can request the Assessing Officer (AO) to refer the matter to a Valuation Officer (DVO).

If the DVO’s valuation is lower than the SDV, the DVO’s value is accepted.

🧾 Differences from Section 50C

| Feature | Section 43CA | Section 50C |

| Applies to | Builders/developers | Individuals/investors |

| Nature of Asset | Stock-in-trade | Capital asset |

| Income Head | Business income | Capital gains |

Final Thoughts on Section 43CA

Section 43CA ensures that real estate businesses report fair profits, even if they sell below market value. Builders offering steep discounts must check whether they’re still within the 10% safe harbour — or risk paying tax on a higher deemed sale value.

FAQs

Does Section 43CA apply to residential property sold by individuals?

No. It applies only to builders, developers, and businesses selling property as stock-in-trade.

What happens if the stamp duty value increases after the agreement?

If part-payment was received on/before the agreement via banking channels, the agreement date value is considered, avoiding future SDV hikes.

Can a builder challenge a high SDV?

Yes. They can request the Assessing Officer for DVO valuation.

What is the current safe harbor limit?

10% variation between actual sale price and SDV is allowed.