Sub-category 2: Checking Eligibility for GST Registration

| Normal Category States/UT who opted for a new limit of Rs.40 lakh | Normal Category States who choose status quo | Special Category States/UT who opted for new limit of Rs.40 lakh | Special Category States/UT who opted for new limit of Rs.20 lakh |

| Kerala, Chhattisgarh, Jharkhand, Delhi, Bihar, Maharashtra, Andhra Pradesh, Gujarat, Haryana, Goa, Punjab, Uttar Pradesh, Himachal Pradesh, Karnataka, Madhya Pradesh, Odisha, Rajasthan, Tamil Nadu, West Bengal, Lakshadweep, Dadra and Nagar Haveli and Daman and Diu, Andaman and Nicobar Islands and Chandigarh | Telangana | Jammu and Kashmir, Ladakh and Assam | Puducherry, Meghalaya, Mizoram, Tripura, Manipur, Sikkim, Nagaland, Arunachal Pradesh and Uttarakhand |

GST Registration

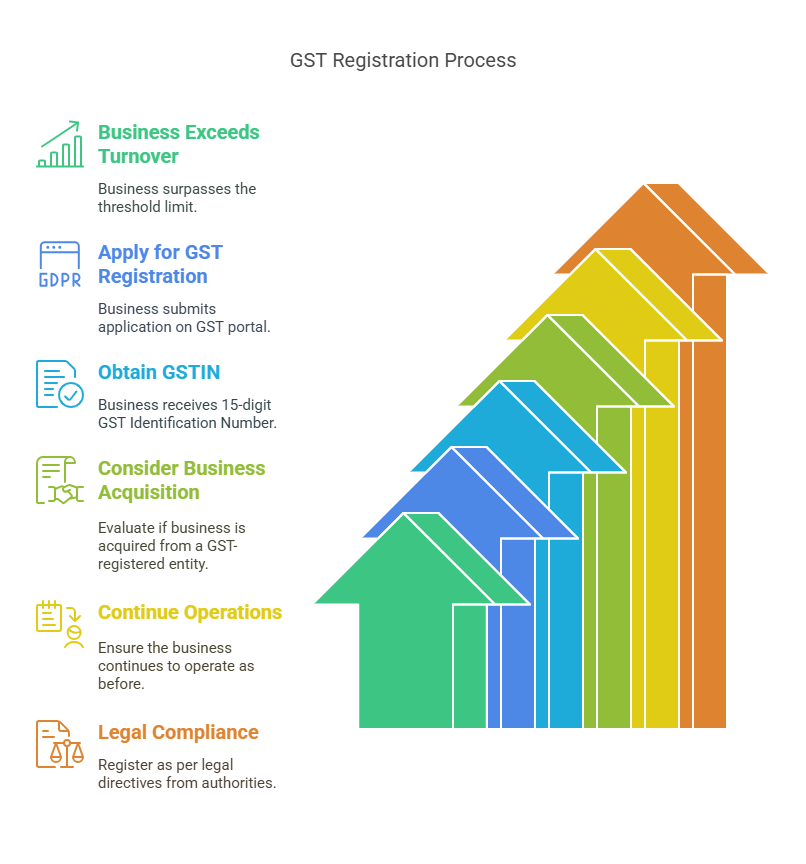

GST Registration Process :

Once the Business exceeds the turnover in a state, it is liable to mandatorily register itself at the GST portal and obtain a GST Registration Number, after applying for the Registration, the Business will obtain a 15 Digit Number Called “Goods and Services Tax Identification Number” otherwise referred as GSTIN.

For the purpose of computation of such Turnover, following criteria are set

- The turnover of the entity exceeds the thresh hold limit as the case as per the aforesaid (provided) table

- The business is acquired (bought, amalgamated, transferred etc.) from a person who is registered under the GST Law or who was liable to be registered under the GST Law. Further the business is carried forward in going concern (meaning it will continue to operate the same as before).

- In a case of transfer pursuant to sanction of a scheme or an arrangement for amalgamation or demerger pursuant to an order of a High Court, Tribunal or otherwise, the transferee shall be liable to be registered from the date upon which ROC issues Incorporation Certificate.

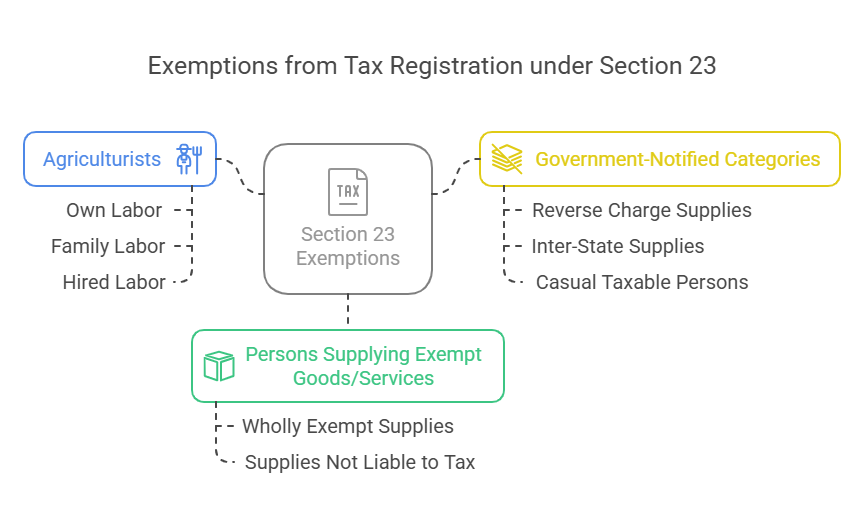

who are Free from GST Registration:

Section 23 Provisions for persons not liable for registration i

- Person engaged exclusively in the business of supplying goods and /or services not liable to tax/wholly exempt from tax

- An agriculturist to the extent of supply of produce out of cultivation of land is also not liable to registration. The term agriculturist has been defined under section 2(7) as an individual/Hindu Undivided Family (HUF) who undertakes cultivation of land

a. by own labour, or

b. by the labour of family, or

c. by servants on wages payable in cash or kind or by hired labour under personal supervision or the personal supervision of any member of the family. - Specified category of persons notified by the Government that are exempted from obtaining registration:

a. Persons making only reverse charge supplies

b. Persons making inter-State supplies of taxable services up to ₹20 lakh However, the aggregate value of such supplies, computed on an India basis, should not exceed an amount of ₹10 lakh in case of Special Category States of Mizoram, Tripura, Manipur and Nagaland

c. Persons making inter-State taxable supplies of notified handicraft goods and notified products up to ₹20 lakh [₹10 lakh in case of Special Category States of Mizoram, Tripura, Manipur and Nagaland] in a Financial Year.

d. Casual Taxable Persons making inter-State taxable supplies of notified handicraft goods and notified products up to ₹20 lakh [₹10 lakh in case of Special Category States of Mizoram, Tripura, Manipur and Nagaland] in a FY.

However such persons (in points c and d) have to obtain a PAN and have generated

an e-way bill.