To help professionals and taxpayers save time, without jumping between multiple resources, I’ve put together on Key Changes in GSTR 9 for FY 2024-25, backed with important official insights and references for easy access.

What is GSTR-9?

GSTR-9 is the annual GST return that summarizes all outward supplies, inward supplies, ITC claimed, reversals, and tax paid for FY 2024-25. It consolidates all data filed in GSTR-1 and GSTR-3B during the financial year.

🔍 Quick Access Guides

Table 8C Guide – What to report in 8C

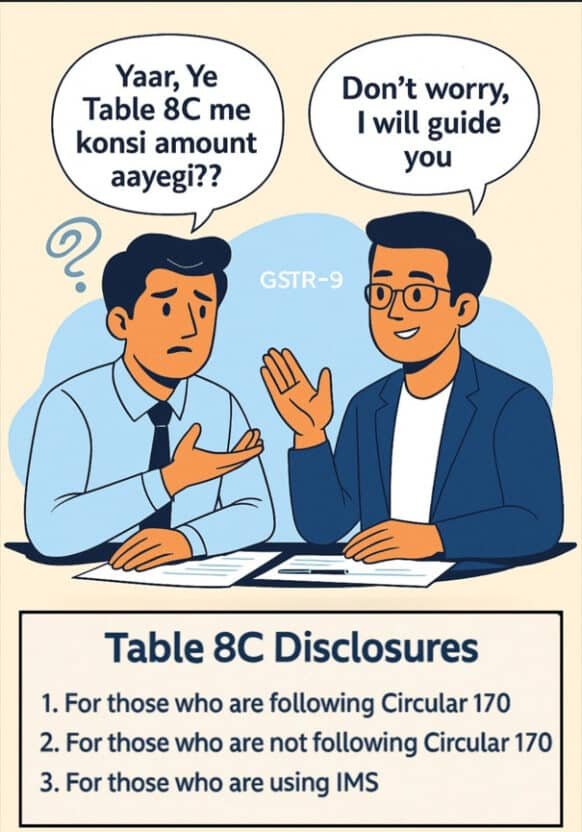

What to report in Table 8C of GSTR-9 for FY 2024-25?

So much confusion, right?

No worries, I have made the simplest guide for you.

We all know that Table 8C is one of the most sensitive tables in GSTR-9, and wrong reporting may lead to GST audit queries or even auto-generated notices.

First, understand the logic of Table 8C

Table 8C captures only the ITC of the current year (FY 24-25 invoices) that is availed in the next FY up to the specified period (i.e., Apr’25 to Oct’25).

Moreover, your Table 8C figure completely depends on how you reported ITC in your GSTR-3B.

Broadly, taxpayers follow three different ITC reporting practices (as I classify them):

1. Following Circular 170 (most common)

2. Not following Circular 170

3. Using Invoice Management System (IMS)

And for each method, the 8C reporting is different.

Let’s break it down.

1) If you are following Circular 170 in GSTR-3B (most common practice)

>What to report in Table 8C:

ITC of FY 24-25 that appears in 2B from Apr’25 to Oct’25, and is availed, or availed–reversed–reclaimed in Apr’25 to Oct’25.

Important Note:

Any ITC of FY 24-25 that had already appeared in 2B during Apr’24–Mar’25 must NOT be reported in 8C, even if you reclaimed it in FY 25-26. For that Table 13 is there.

2) If you are NOT following Circular 170 in GSTR-3B (rare taxpayers)

>What to report in Table 8C:

✔ ITC of FY 24-25 (2B period Apr’24–Mar’25) which you did not avail or reverse in FY 24-25, but availed directly in Apr’25 to Oct’25

PLUS

✔ ITC of FY 24-25 that appears in 2B of Apr’25 to Oct’25, and is availed in Apr’25 to Oct’25

3) If you are using IMS (very rare taxpayers)

>What to report in Table 8C:

✔ Invoices of FY 24-25 that appeared in 2B, were kept pending till Mar’25,and were accepted/availed in Apr’25 to Oct’25

PLUS

✔ ITC of FY 24-25 appeared in 2B of Apr’25 to Oct’25 and accepted/availed in the same period.

I hope this clears your confusion about Table 8C.

Feel free to reach out for any clarifications.

Till then, have a great and hassle-free tax season !!

Table 8D Guide – Reasons for Negative 8D

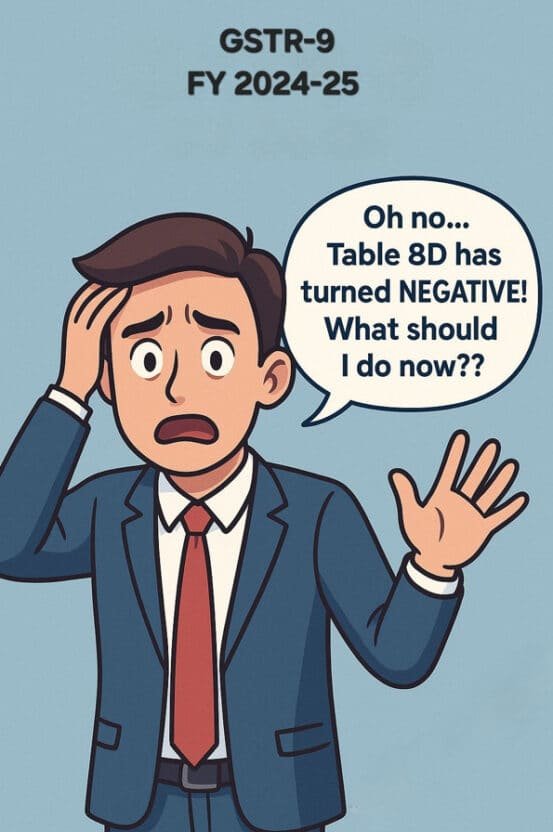

What if Table 8D turns Negative in GSTR-9 for FY 2024-25?

You may think, table 8D going negative isn’t new.

True. Until last year, a negative 8D was a fairly common occurrence.

However, with the recent amendments in Form GSTR-9 (from FY 2024-25 onward), a negative 8D is no longer just “routine” it can be critical from a reconciliation and audit standpoint.

Understanding Table 8D (In the context of FY 2024-25)

Let’s reiterate the basics:

Table 8D =

8A. ITC auto-populated from 2B

(MINUS)

8B. ITC claimed in current year (CY)

(MINUS)

8C. ITC that will be claimed in the next FY within the specified time limit (e.g., up to Oct’25).

In FY 2023-24 and earlier, taxpayers could validate a negative 8D with the help of Table 8C (Previous Year).

In other words, 8D could go negative only to the extent ITC available in PY Table 8C.

But this logic applies only up to FY 2023-24.

So, what has changed from FY 2024-25?

8A now reflects ITC pertaining only to FY 2024-25. 8B and 8C also represent only FY 2024-25 data

There is no reference of prior years in this section anymore

If all data in 8A, 8B, and 8C belongs to the same financial year, ideally, Table 8D should not turn negative at all.

That would be the ideal reconciliation practice.

But real life isn’t always ideal.

There are situations where 8D may still show a negative figure.

Let’s explore the major practical possibilities:

1️⃣ Incorrect CN reporting by the supplier

Since 8A is non-editable, any CN wrongly reported by the supplier and deemed accepted by the recipient can directly impact the 8D computation.

2️⃣ 3B ITC reporting approach adopted by the taxpayer

If you follow Circular 170, where only invoices and debit notes are availed and reversed, but credit notes are ignored in reconciliation, 8D may inadvertently turn negative.

3️⃣ Misclassification between Table 6A(1) and 6B

Errors during ITC mapping in these tables, even if unintentional may distort annual reconciliation output.

4️⃣ Incorrect figures reported in Table 8C

This is one of the most sensitive areas.

If wrongly disclosed, it can disrupt the 8D outcome.

(I’ve shared a detailed post on Table 8C for quick reference, see comment box.)

5️⃣ Excess ITC actually availed and utilized

If the taxpayer has genuinely availed excess credit, reversal must be done along with applicable interest via DRC-03.

If you’re facing a negative 8D, evaluate whether the above scenarios could be the underlying causes.

Also note that, the above possibilities are illustrative, not exhaustive.

Table 8D going negative should not be considered normal from FY 2024-25 onward.

Conduct a thorough self-review and verify your reconciliation independently.

Table 8A Update – What has changed

A must read for all those involved in preparing, reviewing or filing GSTR-9/9C.

The logic for auto-population of data in Table 8A has once again been changed.

During the PY, several tickets were raised regarding possible mismatch between Tables 8A and 8C for FY 2023-24 (At that time too, logic was changed).

In response, GSTN had also issued an advisory dt 9th Dec 2024 addressing this concern. However, the said advisory did not fully resolve the reconciliation concern.

To resolve that inconsistency, the logic of Table 8A has now been modified to align it with the exact wordings.

The following chronology provides a clear view of this matter.

Earlier Practice – Prior to 23-24

Table 8A was generated based on GSTR-2A, considering returns filed up to 30.09 / 30.11 of the following FY.

> For FY 2023-24

Logic was changed, GSTR-2B became the base instead of 2A, aligning with the amendment in Section 16, since ITC availment is now based on 2B.

Hence, 8A = GSTR-2B from April 2023 to March 2024 tax period.

Now For FY 2024-25 (New Change)

8A continues to be based on GSTR-2B, but the logic has shifted from “period” to “document date”.

Now, if document pertains to FY 2024-25 but appears in GSTR-2B from Apr’25 to Oct’25, it will still form part of 8A of 24-25 which earlier was not the case.

Fair enough, any change that brings the law and the portal in sync is a positive move. No objections here.

But the real challenge now lies with Table 8C. Every year new logic to be given to derive an amount for this table. (Even that practice too, differ from taxpayer to taxpayer)

Earlier (till FY 22-23) if the current year’s 8D went negative, it was easily justified through previous year’s 8C.

Now, with introduction of Table 6A1, this scenario won’t occur anymore.

So does this mean 6A1 of CY must now always equal 8C of PY?

Apparently yes but there’s more to it. I’ll cover those details in my upcoming posts.

But the bigger problem is, even departmental officers often differ in their interpretation of these logics.

Adding to this challenge, the system has also been issuing ASMT-10 / DRC-01 notices due to these year-on-year changes in logic.

If not addressed appropriately, such discrepancies may escalate into demand orders or litigation, leading to unnecessary cost, time, and compliance burden for genuine taxpayers.

Hope, this will be the final change in 8A logic.

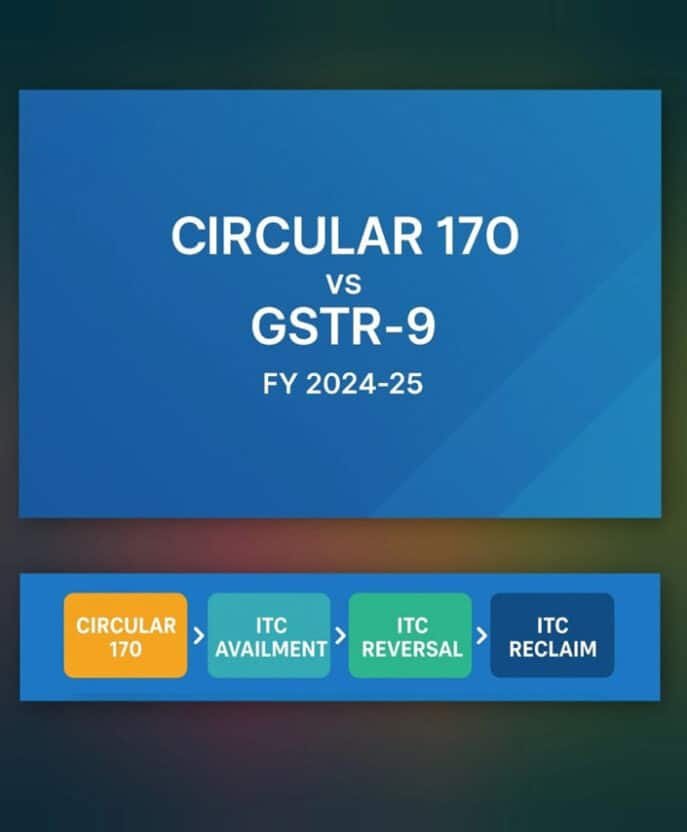

GSTR-9 vs Circular 170 – ITC reporting clarity

Since August 2022, the GSTR-3B reporting pattern especially for Table 4 (ITC section) has undergone a key change.

We all know that GST is a destination-based consumption tax, meaning the state where goods or services are consumed gets the GST revenue.

Understanding The IGST Flow

Mr. A (GJ) sells goods to Mr. B (MH).

As this is an inter-state transaction, IGST is levied. The tax first goes to the Centre, which then shares it with the State of consumption (MH in our case).

Sounds straightforward right.

But that’s not true coz consumption for IGST settlement is evidenced by the recipient declarations (i.e. ITC availed / reversals) in returns, so unavailed ITC affects settlement process of IGST.

If Rs.100 of IGST credit is generated in GSTR-2A/2B, but the taxpayer availed / reversed only 80, the remaining 20 stays unclaimed.

That unveiled ITC (20) causes a revenue mismatch and the Centre cannot share that portion with the State, as per the consumption-based mechanism.

To address this, Circular 170 mandated that taxpayers must

1. Avail all ITC reflected in GSTR-2B.

2. If eligible, claim it.

3. If ineligible, reverse it.

4. If not booked, transfer it to the Electronic Reclaimable Ledger.

This streamlined the ITC process and by now, most taxpayers are following it (hopefully).

Now the Key Question: GSTR-9 Disclosure for FY 2024-25 w.r.t. ITC availed and reversed temporarily on account of Circular 170 under Table 4B2.

Many taxpayers are confused about where to disclose such ITC in GSTR-9, since there’s no separate disclosure field for it yet.

Until FY 2023-24, such ITC was usually shown in Table 6M (Any other ITC).

But in FY 2024-25, Table 6M’s heading has changed, so that’s no longer applicable.

GSTN has released a set of FAQs on the recent GSTR-9 form changes, which also address this particular issue.

Below is the quick breakdown of the disclosure requirements for easy reference:

ITC Availment > Table 6B

ITC Reversal > Table 7H

ITC Reclaimed in next FY > Table 13

Exclusion > Do NOT include in Table 8C of current FY

Next Year Reporting > Table 6A1 of FY 2025-26

A much-needed clarification indeed bringing consistency in how Circular 170 related ITC is reported across returns.

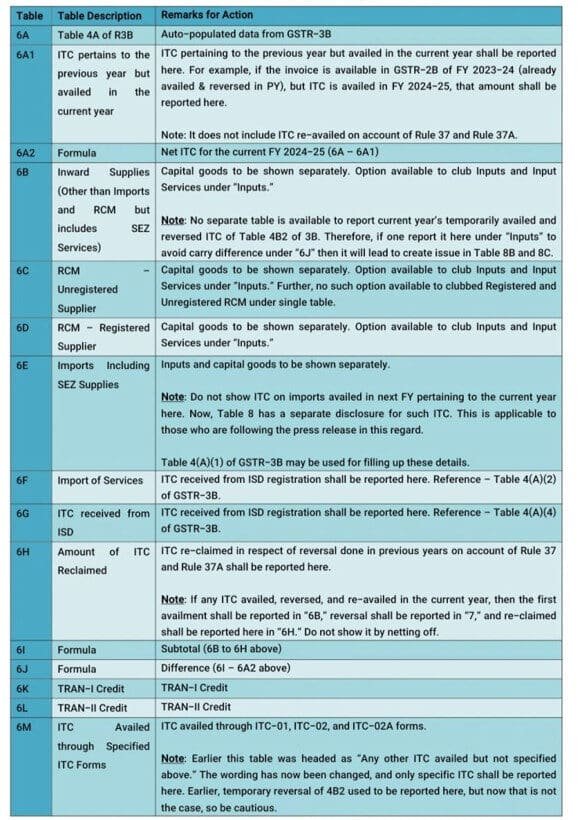

Table 6 Guide – How to report ITC

GST Annual Return – Quick Guide to Table 6A to 6M (FY 2024-25)

Filing GSTR-9 often raises questions around how to report various categories of Input Tax Credit across Tables 6A to 6M.

To simplify this, I’ve prepared a concise and practical table wise reference guide covering what needs to be reported basis latest rules and instructions.

Also, I’d love to hear your thoughts on the recent changes made in GSTR-9/9C and the challenges you’re facing, if any.

If you’d like to see more such detailed explanations, comment “Yes” along with the relevant table number below.

P.s. Please read 6F as “Import of Services” instead of “ITC received from ISD.”

Apologies for the clerical error. Thank you.

Table 7J differences on account of Table 6A1

The Hidden Complexity Behind the “Simplified” GSTR-9

There’s no doubt a lot of good changes have been made in the Annual Return to make it more transparent, easy, and user-friendly.

But there’s still one area that continues to trouble taxpayers and that is Table 7J.

Earlier, Table 7J used to represent “Net ITC Available for Utilization” during the FY, which perfectly matched with Table 4C of GSTR-3B.

However, in the latest version of GSTR-9, while significant changes have been made in Table 6, the formula for deriving Net ITC in Table 7J remains the same (i.e., 6O – 7I).

The problem is, previously, Gross ITC from Table 6O included all ITC availed in Table 4A, which after adjustments in Table 7, gave us the “Net ITC Available for Utilization” for the year and that was –

>easy to explain,

>easy to audit, and

>easy for officers to verify.

But now, the Gross ITC in Table 6O excludes 6A1 (ITC pertaining to PY but availed in current FY). And this has been done to make Table 8 reco more simpler.

This exclusion of 6A1 ITC in the formula means the Net ITC in Table 7J now shows a difference equal to 6A1, making cross-check with GSTR-3B bit difficult apparently.

And for taxpayers with turnover above ₹5 crore, this will further complicate GSTR-9C reconciliation, especially in Table 12 (ITC reconciliation with books).

It’s not too late, the MoF / GSTN can still issue an advisory or clarification to resolve this mismatch.

In my opinion, the simplest fix is to revise the formula for deriving “Net ITC Available for Utilization” in Table 7J (6A1+6O-7I), that alone would ease taxpayers lives significantly.

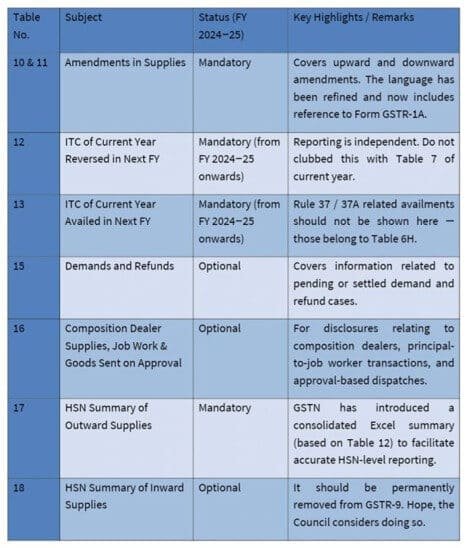

Table 10 to 18 Guide (Optional / Mandatory)

GST Annual Return – Quick Guide to Table 10 to 18 (FY 2024-25)

Continuing the series on GST Annual Return Table Updates, sharing key details on mandatory vs. optional tables in GSTR-9 for FY 2024–25 basis latest rules and instructions.

To make it easier, I’ve prepared a clear, table-wise summary (Table 10 to 18) along with practical notes for reporting.

Feel free to share your feedback or any practical challenges you’re facing with the new reporting structure.

Table 8C vs Table 13 – Key differences

Table 8C vs 13: One is 2B. Other is Big Boss.

Many professionals and taxpayers are confused about what to report in Table 8C and Table 13.

Yes, the wordings look similar “ITC of current FY availed in the next FY ” but their purpose, scope, and impact are entirely different.

Let’s simplify it.

Table 8C

It is part of Table 8 reconciliation, which is linked to GSTR-2B (Auto-populated ITC statement).

It deals only with B2B inward supplies under FCM (Forward Charge Mechanism).

It does NOT include any ITC category other than B2B-FCM, such as:

❌ Imports (IMPG)

❌ RCM (Reverse Charge)

❌ SEZ (Goods)

ITC availed in GSTR-3B of the next FY but pertaining to the current FY’s B2B-FCM invoices must be reported here.

In short, 8C exists only to complete 2B ITC reconciliation.

(Refer to my detailed post on 8C for reporting guidance.)

Table 13

This is a mandatory ITC disclosure from FY 2024-25, introduced to capture ITC-related adjustments in a wider sense.

Although the wording resembles 8C but its scope is much broader.

It includes ITC of the current FY claimed in the next FY across multiple categories, such as:

✅ B2B-FCM ITC claimed in NY (essentially 8C)

✅️ Availed & Reversed in CY but Claimed in NY (On account of Cir.170)

✅ Imports of goods (IMPG)

✅ ITC on RCM claimed in NY

❌️ Does not include ITC claimed on account of Rule 37 & 37A. That should be part of 6H.

Therefore, Table 13 will always be equal to or greater than Table 8C.

Taxpayers following Circular 170 (2B-linked reconciliation approach) will typically see Table 13 higher than Table 8C.

Simple Rule to Remember – Key Changes in GSTR 9 for FY 2024-25

8C = Only B2B-FCM ITC claimed next FY for reconciliation

Table 13 = All eligible ITC of current FY claimed next FY (incl. imports, RCM, etc.) (excl. Rule 37 and 37A)

I hope this clears the confusion around reporting.

More helpful and practical insights coming soon.

Until then, wishing you a smooth and productive tax season ahead !!

P.S. Do check out my other posts on GSTR-9 reporting and reconciliations.

Relevance of 4B2 (temporarily reversal) line items of 3B in GSTR-9

R9 Annual Return ITC Reporting Will Be Challenging This Year

Those who are not maintaining month-wise 4B(2) line items may find this year’s annual return significantly more difficult.

As we know, major changes have been made in Tables 6, 7 and 8 of GSTR-9 for FY 2024-25, especially in the ITC section.

One of the biggest changes is the introduction of Table 6A(1) along with a new logic for Table 8A auto-population.

The purpose of 6A(1) is to reduce the reconciliation issues taxpayers faced earlier in Table 8.

Under 6A(1), all ITC belonging to the PY must be reported here.

CY ITC must be separately classified under Tables 6B to 6H, depending on its nature.

Further, data reported in Table 6B will flow into Table 8B for matching with 8A.

Now, the new change in Table 8A is critical:

Only documents dated between 01.04.2024 and 31.03.2025 will appear in 8A, even if they auto-populate in GSTR-2B from Apr 2025 to Oct 2025.

This means taxpayers who do not maintain detailed 4B(2) reversal line items will have to identify FY 2023-24 invoices, remove them from 6B, and regroup them under 6A(1).

Even after this adjustment, differences may still arise in Table 7J, because 6A(1) is not included in the formula for 7J.

So, while Table 8 may become cleaner and reconcilable, the mismatch will shift to Table 7J and Table 12 of GSTR-9C.

Important FAQs published by the GSTN

GSTN has recently released a comprehensive set of FAQs on GSTR-9 and GSTR-9C for FY 2024-25, addressing several practical issues and ambiguities.

Below is a concise summary of the most important points for taxpayers and professionals:

Table 8A Revised Auto-population Logic

Now includes FY 2024-25 invoices appearing in GSTR-2B up to October 2025 and excludes prior FY (2023-24) records.

ITC Reporting Simplified (Tables 6A1, 6H, 8C, 13)

6A1 – ITC of FY 2023-24 claimed in FY 2024-25.

6H – ITC reclaimed under Rule 37/37A (considered ITC of the year of reclaim).

8C & 13 – For missed ITC of current FY claimed in next FY (up to the specified period).

Inclusion of GSTR-1A Amendments

Supplies added or amended through GSTR-1A will now be auto-populated in Tables 4 and 5 of GSTR-9.

>Temporarily reversed ITC in 24-25 under 4B2 of 3B shall be reported in 6B and Table 7H. Further re-availment of such ITC shall be reported in Table 13 only.

Table 17 (HSN Summary)

GSTN has introduced a download facility ‘Table 12 of GSTR-1/1A HSN Details’ for easy compilation of Table 17 of GSTR-9.

>Removal of 65% Concessional Rate Checkbox

This detailed FAQ release was truly the need of the hour, bringing much needed clarity and alignment between law and system logic.

Appreciation to GSTN for providing such comprehensive guidance at the right time.

GSTR-9 Applicability for FY 2024-25

The filing requirement for GSTR-9 (GST Annual Return) for the Financial Year 2024-25 is governed by the taxpayer’s Aggregate Annual Turnover (AATO). This section provides clarity on who must file and who is exempted.

Who MUST File GSTR-9 for FY 2024-25?

GSTR-9 is mandatory for every registered person under GST having a turnover above ₹2 crore in FY 2024-25, except those notified otherwise.

The following taxpayers are required to file:

- Regular taxpayers (including those who shifted to/from composition during the year)

- SEZ units & SEZ developers

- E-commerce operators (as long as not registered as TCS collectors)

- Businesses availing ITC and filing monthly/quarterly GSTR-1 & 3B

Turnover above ₹2 Crore: Mandatory filing of Form GSTR-9.

Turnover above ₹5 Crore: Mandatory filing of Form GSTR-9, along with the self-certified reconciliation statement, Form GSTR-9C.

Turnover Criteria for GSTR-9 Filing (FY 2024-25)

| Type of Return | Applicability (FY 2024-25) |

|---|---|

| GSTR-9 | Mandatory if turnover > ₹2 crore |

| GSTR-9C (Audit / Reconciliation Statement) | Mandatory if turnover > ₹5 crore |

Who is Exempted or Not Required to File?

Taxpayers with an aggregate annual turnover up to ₹2 Crore for FY 2024-25 are exempted from filing GSTR-9, as per relevant notifications issued by the CBIC. However, they may still file it voluntarily.

The following categories of taxpayers are exempt from filing:

- Composition taxpayers (CMP Scheme) – they file GSTR-9A (only if enabled by govt; otherwise exempt)

- TDS deductors (GSTR-7 filers)

- TCS collectors (GSTR-8 filers)

- Input Service Distributors (ISD)

- Non-resident taxable persons (NRTP)

- Casual taxable persons (CTP)

Note:

GOI has usually exempted composition taxpayers from GSTR-9A every year. If similar exemption is notified for FY 2024-25, CMP taxpayers will remain exempt.

Key Dates GSTR-9 for FY 2024-25

| Requirement | Due Date (FY 2024-25) |

| GSTR-9 Filing Last Date | December 31, 2025 (Unless extended by the Government) |

| GSTR-9C Filing Last Date | December 31, 2025 (For AATO > ₹5 Cr) |

| Last Date to claim ITC for FY 24-25 | Up to October 2025 return filing (or furnishing of return for September 2025, whichever is earlier) |

Penalties for Not Filing GSTR-9

If GSTR-9 is not filed within the due date:

- Late fee:

₹200 per day (₹100 CGST + ₹100 SGST) - Maximum late fee capped at:

0.50% of turnover (0.25% CGST + 0.25% SGST) - ITC mismatches may trigger DRC-01, ASMT-10 or audit notices.

Why GSTR-9 Applicability Matters More in FY 2024-25?

- Major changes in Tables 6, 7, 8

- Introduction of Table 6A(1)

- Modified logic for Table 8A

- Expanded reporting under Table 13

- Increased scrutiny and automated comparisons by GSTN

Because of these updates, non-filing or incorrect filing may easily trigger:

✔ automated mismatch notices

✔ audit queries

✔ blocked ITC

✔ demand orders

I hope this helps make your GSTR-9 journey smoother.

Also, if you have any questions or need clarification, drop a message, happy to help.

Let’s simplify compliance together !!

FAQs

What is GSTR-9 for FY 2024-25?

GSTR-9 is the annual GST return that summarizes all outward supplies, inward supplies, ITC claimed, reversals, and tax paid for FY 2024-25. It consolidates all data filed in GSTR-1 and GSTR-3B during the financial year.

Who is required to file GSTR-9 for FY 2024-25?

All regular taxpayers with aggregate turnover above ₹2 crore during FY 2024-25 must file GSTR-9. SEZ units and SEZ developers are also required to file it.

Who is exempt from filing GSTR-9 for FY 2024-25?

The following taxpayers are exempt:

Composition taxpayers (unless notified otherwise)

Input Service Distributors (ISD)

TDS deductors (GSTR-7 filers)

TCS collectors (GSTR-8 filers)

Casual taxable persons (CTP)

Non-resident taxable persons (NRTP)

What is the due date to file GSTR-9 for FY 2024-25?

The due date is 31st December 2025, unless extended by the government via notification.

What are the major changes in GSTR-9 for FY 2024-25?

Key changes include:

New Table 6A(1) for PY ITC

Revised auto-population logic for Table 8A

Expanded reporting requirements in Table 13

Table 6, 7, 8 restructuring for better ITC reconciliation

Inclusion of GSTR-1A amendments in Tables 4 & 5

What is reported in Table 8C of GSTR-9?

Table 8C reports ITC of the current financial year (FY 2024-25) that is availed in the next FY (April 2025 to October 2025) as per GSTR-2B reconciliation. Only B2B-FCM ITC is included.

What is reported in Table 13 of GSTR-9?

Table 13 includes all eligible ITC of the current year claimed in the next financial year, including imports, RCM ITC, B2B-FCM ITC, reclaim under Circular 170 (except Rule 37 & 37A).

Why does Table 8D show a negative figure?

For FY 2024-25, a negative Table 8D can occur due to:

Supplier’s incorrect credit note reporting

Errors in ITC reporting in GSTR-3B

Mistakes in Table 6B or 8C

Excess ITC availed

A negative 8D is no longer “normal”, and requires investigation.

Is GSTR-9C mandatory for FY 2024-25?

Yes. GSTR-9C (reconciliation statement) is mandatory if aggregate turnover exceeds ₹5 crore in FY 2024-25.

What happens if GSTR-9 is filed late?

Late filing attracts a late fee of ₹200 per day (₹100 CGST + ₹100 SGST), capped at 0.50% of turnover. Non-filing may also lead to notices such as ASMT-10, DRC-01, and ITC mismatches.

Can GSTR-9 be revised for FY 2024-25?

No. GSTR-9 cannot be revised once filed. Any correction must be made in subsequent returns or via DRC-03.

Is Table 6A(1) mandatory for FY 2024-25?

Yes. Table 6A(1) is mandatory and reports ITC of FY 2023-24 that is claimed in FY 2024-25.

What is the difference between Table 8C and Table 13 in GSTR-9?

Table 8C: Only B2B-FCM ITC of the current FY claimed in next FY (for 2B reconciliation).

Table 13: All eligible ITC of current FY claimed in next FY (imports, RCM, 170-related ITC, etc.).

Does GSTR-1A impact GSTR-9 for FY 2024-25?

Yes. Supplies added/modified via GSTR-1A will auto-populate in Tables 4 and 5 of GSTR-9.

What should I do if there is a mismatch in Table 8?

Recheck:

Supplier GSTR-1 / 2B entries

ITC availed vs reversed

Table 6B classification

Table 8C reporting

If differences persist, voluntary payment via DRC-03 may be required.