Two of the most critical perspectives are financial vs management accounting. While they might sound similar, they serve vastly different purposes. Welcome, business owners, entrepreneurs, and aspiring financial professionals! In the dynamic world of business, understanding your numbers is paramount to success. But did you know there are different ways to look at those numbers?

This comprehensive guide will explore the difference between financial accounting and management accounting. We’ll delve into their definitions, characteristics, key distinctions, and why your business needs both to thrive. So, grab a cup of coffee, and let’s demystify the world of accounting!

What is Financial Accounting?

Financial accounting is the process of recording, summarizing, and reporting a company’s business transactions through financial statements. Think of it as the official storyteller of your company’s financial history.

Definition and Purpose

The primary purpose of financial accounting is to provide accurate and consistent information to external stakeholders. These are individuals and entities outside your company who have an interest in its financial performance.

Key Characteristics of Financial Accounting

- External Users: The primary audience for financial accounting reports includes investors, creditors, lenders, government agencies (like the IRS), and the general public.

- Historical Data: Financial accounting is backward-looking. It focuses on transactions that have already occurred, providing a historical record of financial performance.

- GAAP/IFRS Compliance: To ensure consistency and comparability, financial accounting adheres to a strict set of rules and standards known as Generally Accepted Accounting Principles (GAAP) in the United States or International Financial Reporting Standards (IFRS) in many other countries.

- Objectivity and Verifiability: Financial accounting information must be objective and verifiable. This means that the data can be independently confirmed and is not based on personal opinions or speculation.

The Core Financial Statements

Financial accounting culminates in the preparation of several key financial statements:

- Balance Sheet: This statement provides a snapshot of a company’s financial position at a specific point in time, detailing its assets, liabilities, and owner’s equity. *

- Statement of Cash Flows: This statement shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing, and financing activities.

- Statement of Retained Earnings: This statement outlines the changes in retained earnings for a corporation over a specified period.

- Income Statement: Also known as the profit and loss (P&L) statement, it summarizes a company’s revenues, expenses, gains, and losses over a period, revealing its net income or loss.

What is Management Accounting?

Management accounting, also known as managerial accounting, is the process of identifying, measuring, analyzing, interpreting, and communicating financial information to managers for the pursuit of an organization’s goals. It’s the “insider’s view” of the company’s finances.

Definition and Purpose

The main goal of management accounting is to provide internal decision-makers with the information they need to make informed business decisions, plan for the future, and control operations.

Key Characteristics of Management Accounting

- Internal Users: Management accounting reports are created for and used by the company’s own management team, from department heads to the CEO.

- Future-Oriented: Unlike financial accounting, management accounting is forward-looking. It uses both historical and estimated data to help with planning and forecasting.

- No Fixed Rules: Management accounting is not bound by GAAP or IFRS. The reports can be customized to meet the specific needs of the managers.

- Subjectivity and Relevance: Management accounting information is often more subjective and emphasizes relevance and timeliness over precision.

Common Management Accounting Reports

Management accounting generates a wide variety of reports, including:

- Budget Reports: These reports compare actual results to budgeted amounts, helping managers to monitor and control spending.

- Variance Analysis Reports: These reports analyze the difference between actual and planned results, highlighting areas of strong or weak performance.

- Cost-Volume-Profit Analysis: This analysis helps managers understand the relationships between costs, volume, and profit, which is crucial for pricing decisions and sales strategies.

- Performance Reports: These reports can be tailored to specific departments, products, or employees to evaluate their performance against set goals.

The Key Differences: Financial vs Management Accounting

Now that we have a foundational understanding of both, let’s dive into the key difference between financial accounting and management accounting.

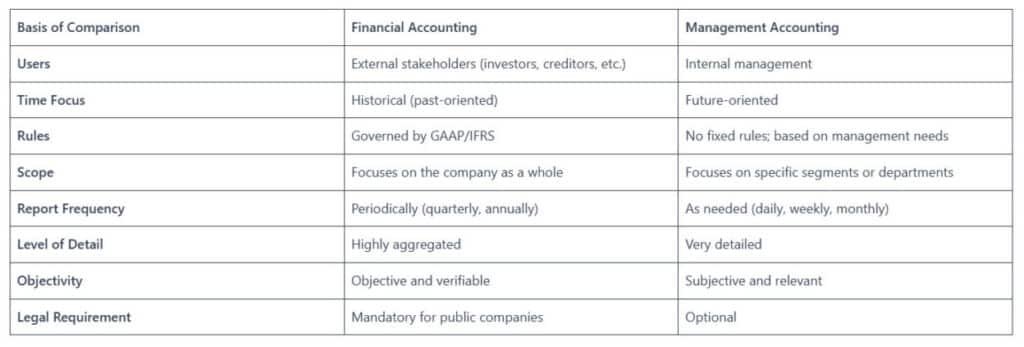

| Basis of Comparison | Financial Accounting | Management Accounting |

| Users | External stakeholders (investors, creditors, etc.) | Internal management |

| Time Focus | Historical (past-oriented) | Future-oriented |

| Rules | Governed by GAAP/IFRS | No fixed rules; based on management needs |

| Scope | Focuses on the company as a whole | Focuses on specific segments or departments |

| Report Frequency | Periodically (quarterly, annually) | As needed (daily, weekly, monthly) |

| Level of Detail | Highly aggregated | Very detailed |

| Objectivity | Objective and verifiable | Subjective and relevant |

| Legal Requirement | Mandatory for public companies | Optional |

Users of Information

As the table shows, this is the most significant difference between financial accounting and management accounting. Financial accounting provides a standardized view for those outside the company, while management accounting offers a customized perspective for those inside.

Time Focus

Financial accounting is like looking in the rearview mirror, while management accounting is like looking at the road ahead through the windshield. One tells you where you’ve been, and the other helps you decide where to go.

Rules and Regulations

The strict adherence to GAAP or IFRS in financial accounting ensures that all companies are speaking the same financial language. Management accounting, on the other hand, is like a private conversation within the company, so it can use its own shorthand and focus on what’s most important to the decision-makers.

Scope and Nature of Information

Financial accounting paints a broad picture of the entire organization’s financial health. Management accounting, however, can zoom in on a specific product line, a single department, or even an individual project to provide granular insights.

Similarities Between Financial and Management Accounting

Despite their many differences, it’s important to recognize that financial and management accounting are not entirely separate. They share some common ground:

- Shared Data Source: Both disciplines often draw from the same core financial data. The difference lies in how that data is analyzed and presented.

- Both deal with financial information: At their core, both are concerned with the financial aspects of the business.

- Goal of improving company performance: Ultimately, both financial and management accounting contribute to the overall goal of enhancing the company’s performance and value.

Why Both are Crucial for Business Success

A common misconception is that businesses need to choose between financial and management accounting. The truth is, a successful business needs both to thrive.

Financial Accounting for Investor Confidence

Financial accounting is your company’s face to the world. Accurate and transparent financial reporting builds trust with investors, lenders, and other stakeholders, which is essential for securing funding and maintaining a positive public image.

Management Accounting for Strategic Decisions

Management accounting is the engine that drives your business forward. It provides the insights you need to make smart, data-driven decisions that will lead to growth and profitability.

Career Paths in Financial and Management Accounting

The difference between financial accounting and management accounting also extends to the career paths available in each field.

Financial Accounting Careers

- Financial Accountant: Prepares financial statements and ensures compliance with regulations.

- Auditor: Independently examines a company’s financial statements to ensure their accuracy.

- Tax Accountant: Specializes in tax planning and compliance.

Management Accounting Careers

- Management Accountant: Works within a company to provide financial information and analysis to managers.

- Cost Accountant: Focuses on analyzing and controlling a company’s costs.

- Financial Analyst: Analyzes financial data to help with investment decisions and financial planning.

Conclusion

Understanding the difference between financial accounting and management accounting is not just for accountants; it’s essential for anyone involved in business. Financial accounting provides a clear and accurate picture of your company’s past performance, while management accounting gives you the tools to shape its future. By leveraging the strengths of both, you can build a more resilient, profitable, and successful business.

I hope this in-depth guide has clarified the difference between financial accounting and management accounting.

FAQs

Is one type of accounting more important than the other?

No, both are equally important for different reasons. Financial accounting is crucial for external reporting and compliance, while management accounting is vital for internal decision-making and strategic planning.

Can a small business benefit from management accounting?

Absolutely! Even small businesses can benefit from management accounting principles to make better decisions about pricing, budgeting, and resource allocation.

Do financial and management accountants use the same software?

Often, they use the same core accounting software, but they may use different modules or tools for their specific needs.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.