Section 80-IAC of the Income Tax Act, 1961 is a startup-friendly provision aimed at encouraging entrepreneurship and innovation in India. It offers a 100% income tax deduction on profits for eligible startups, giving them room to grow without the burden of tax in their early years.

What is Section 80-IAC?

Eligible startups can claim a 100% tax deduction on profits for any 3 consecutive assessment years out of the first 10 years from the year of incorporation.

This helps startups reinvest profits into business growth instead of paying taxes during the initial, crucial years.

Who Is Eligible Under Section 80-IAC?

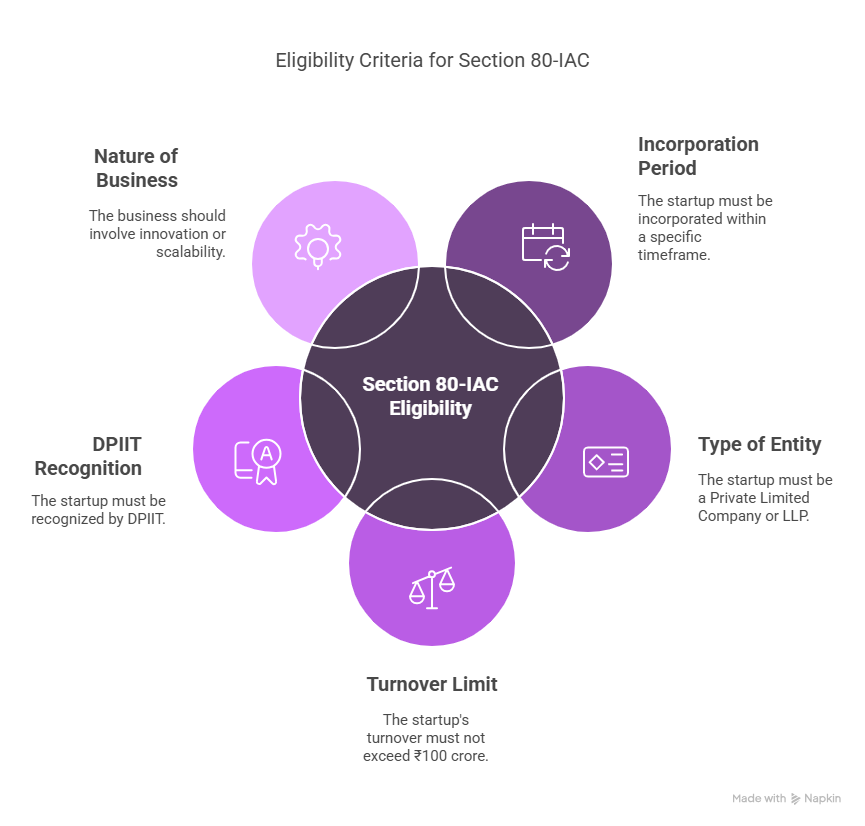

To claim this deduction, the startup must meet the following conditions:

- 📅 Incorporation Period: The startup must be incorporated on or after April 1, 2016 and before April 1, 2025.

- 💼 Type of Entity: It must be a Private Limited Company or a Limited Liability Partnership (LLP).

- 💰 Turnover Limit: The startup’s turnover must not exceed ₹100 crore in any financial year for which the deduction is claimed.

- 📜 DPIIT Recognition: The startup must be recognized as an “Eligible Startup” by the Department for Promotion of Industry and Internal Trade (DPIIT).

- 💡 Nature of Business: The business should involve innovation, development, deployment, or commercialization of new products, processes, or services.

Alternatively, it should be a scalable business model with high potential for employment generation or wealth creation.

How to Claim the 80-IAC Deduction

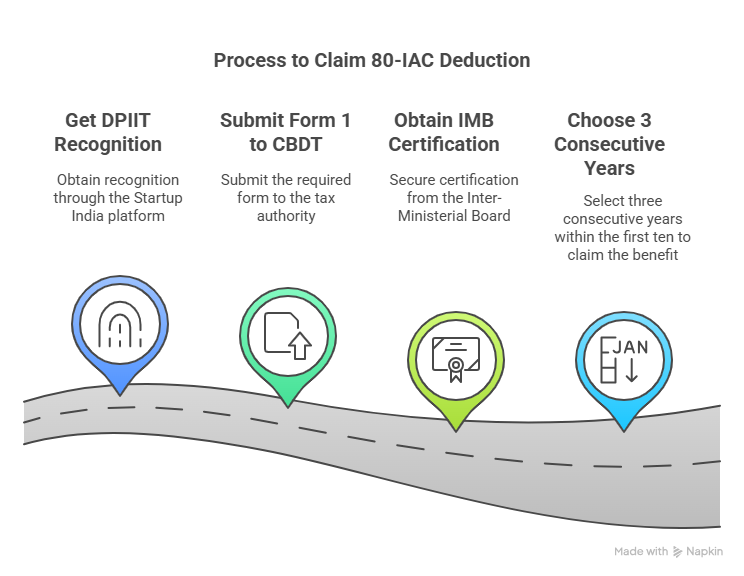

To avail of the tax benefit under Section 80-IAC, follow these steps:

- Get DPIIT Recognition via the Startup India platform.

- Submit Form 1 to the Central Board of Direct Taxes (CBDT).

- Obtain certification from the Inter-Ministerial Board (IMB).

- Choose any 3 consecutive years within the first 10 years to claim the benefit.

👉 Pro Tip: Startups often delay applying until they begin making profits. Choose your 3-year claim period wisely!

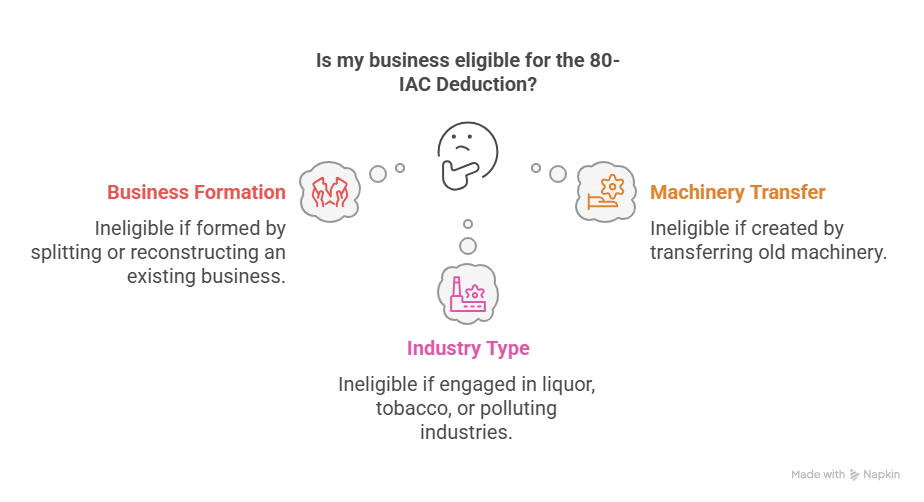

Certain businesses are not eligible for 80-IAC Deduction

- Businesses formed by splitting or reconstruction of an existing business

- Businesses created by transferring old plant and machinery

- Startups engaged in activities like liquor, tobacco, and polluting industries (as per government guidelines)

Additional Points to Note

- 🗓️ The startup can choose any 3 years (consecutive) out of the first 10 years to avail the tax benefit this allows flexibility depending on when the company becomes profitable.

- 🧾 Form 1 & Certification: Startups must file Form 1 with the Central Board of Direct Taxes (CBDT) and obtain certification from the Inter-Ministerial Board (IMB), along with DPIIT recognition.

Summary

| Criteria | Requirement |

| Applicable to | Private Limited Companies & LLPs |

| Incorporation Window | Between April 1, 2016 and March 31, 2025 |

| Turnover Limit | Up to ₹100 crore in any financial year |

| Tax Benefit | 100% deduction on profits for 3 years |

| Recognition Required | Yes – From DPIIT |

| Claim Period | Any 3 consecutive years out of first 10 years |

Conclusion

Section 80-IAC is a powerful incentive for early-stage startups to scale faster without the burden of income tax. If you’re a founder, make sure you check your eligibility and apply for DPIIT recognition to make the most of this benefit

FAQs

Can I claim 80-IAC if I’m already profitable?

Yes, you can choose any 3 consecutive profitable years within your first 10 years to claim the benefit.

Is DPIIT recognition mandatory?

Absolutely. Without it, you won’t qualify for the deduction under Section 80-IAC.

Can a startup formed in 2025 apply?

No. Only startups incorporated before April 1, 2025 are eligible.

Is this applicable to sole proprietors?

No. Only Private Limited Companies and LLPs are eligible.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.