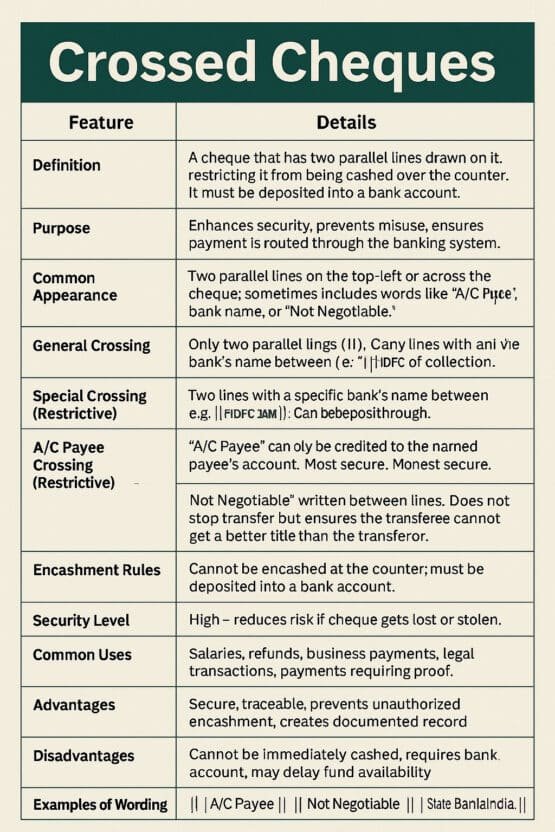

A crossed cheques is a cheque on which two parallel lines (or a crossing mark) are drawn across the face of the cheque usually on the top-left corner or across the cheque to indicate that it cannot be encashed over the counter. Instead, it must be deposited into a bank account. This makes the payment traceable and reduces the risk of theft or misuse.

Common visual forms:

- Two parallel lines

||on the top-left corner; or - Two diagonal lines forming an ‘X’; or

- The words “A/C Payee” or “Account Payee” between the lines (see types below).

Why crossed cheque?

- Prevents immediate encashment by anyone who holds the cheque.

- Ensures funds are credited only through the banking system to an account.

- Adds an extra layer of security against fraud and loss.

Types of crossed Cheques

General Crossing

- Marked with two parallel lines only (no bank name).

- Means the cheque must be deposited into an account at any bank; it does not limit the bank that can collect funds.

- Example mark:

||orCrossed.

Special Crossing

- Parallel lines plus the name of a specific bank written between them (e.g.,

|| HDFC Bank ||).

- Restricts collection to the named bank only — the cheque must be deposited/collected through that bank.

Account Payee Crossing (a restrictive form)

- Marked with the words “A/C Payee” or “Account Payee” between the lines, often combined with the payee’s name.

- The cheque can only be credited to the account of the named payee — even if it is presented through another bank. Highly secure.

Not Negotiable Crossing (optional phrase)

- If “Not Negotiable” is added, the cheque still transfers value but the transferee gets no better title than the transferor (i.e., protects against transfer of a stolen cheque).

Note: Local banking rules or laws may use slightly different terminology. Check your bank’s guidance if you operate in a jurisdiction with special rules.

Crossed Cheques Types – Table Format

| Feature | Details |

|---|---|

| Definition | A cheque that has two parallel lines drawn on it, restricting it from being cashed over the counter. It must be deposited into a bank account. |

| Purpose | Enhances security, prevents misuse, ensures payment is routed through the banking system. |

| Common Appearance | Two parallel lines on the top-left or across the cheque; sometimes includes words like “A/C Payee”, bank name, or “Not Negotiable.” |

| General Crossing | Only two parallel lines (e.g., ` |

| Special Crossing | Two lines with a specific bank’s name between them (e.g., ` |

| A/C Payee Crossing (Restrictive) | “A/C Payee” written between lines. Amount can only be credited to the named payee’s account. Most secure. |

| Not Negotiable Crossing | “Not Negotiable” written between lines. Does not stop transfer but ensures the transferee cannot get a better title than the transferor. |

| Encashment Rules | Cannot be encashed at the counter; must be deposited into a bank account. |

| Security Level | High — reduces risk if cheque gets lost or stolen. |

| Common Uses | Salaries, refunds, business payments, legal transactions, payments requiring proof. |

| Advantages | Secure, traceable, prevents unauthorized encashment, creates documented record. |

| Disadvantages | Cannot be immediately cashed, requires bank account, may delay fund availability. |

| Examples of Wording | ` |

| Bank Processing | Presented through clearing; deposited into the payee’s account only (or specific bank in case of special crossing). |

| Important Notes | Avoid conflicting instructions (e.g., “Pay Bearer” + crossing). Clear and neat crossing ensures smooth processing. |

How to cross a cheque (practical steps)

- Take the cheque you are issuing.

- Draw two parallel lines on the top-left corner or across the face (short, neat).

- Optionally write one of the restrictive phrases between the lines:

A/C PayeeorAccount Payeefor the strongest restriction, or- the name of a bank for a special crossing, or

Not Negotiablefor transfer-title protection.

- Sign the cheque as usual.

Example (simple):

[Payee: Mr. Rahul] Amount: ₹10,000

|| A/C Payee ||

Drawer’s signature

How banks handle a crossed cheque

- A crossed cheque cannot be cashed at the teller window.

- It must be deposited into a bank account. The collecting bank sends it through clearing to the drawee bank for payment.

- If specially crossed to a particular bank, the collecting bank must present it via that named bank or through established clearing channels.

- If the crossing is ambiguous, banks may return the cheque or request clarification.

Advantages

- Security: Reduces risk if cheque is lost or stolen (cannot be cashed immediately).

- Traceability: Funds flow through bank accounts, creating records.

- Proof of payment path: Good for business accounting and audit trails.

- Reduced misuse: Prevents third parties from encashing.

Disadvantages / limitations

- Requires the payee to have a bank account (or to deposit into one).

- Can delay immediate access to funds (compared to open/uncrossed cheque).

- If crossed incorrectly or unclearly, it may be returned or delayed.

Common use cases

- Salary payments, vendor payments, refunds, business transactions, legal settlements — any payment where traceability and security are desired.

Practical tips & best practices

- For safest transfer use “A/C Payee” crossing plus payee name.

- Keep crossings neat and unambiguous; avoid scribbles that might invalidate the crossing.

- If you want collection by a particular bank, write that bank’s full name in the crossing (special crossing).

- Never combine a crossing with contradictory instructions (e.g., “Pay Bearer” and crossing lines).

- If you are a payee and receive a crossed cheque, deposit it promptly to avoid it becoming stale (many banks treat cheques older than 3–6 months as stale).

- If a crossed cheque is lost or suspected stolen, contact your bank immediately to stop payment if possible.

Sample scenarios and wording

General crossed cheque (any bank deposit):

- Mark:

||

- Wording on cheque (optional):

Crossed

Account payee crossing (most restrictive):

- Mark:

|| A/C Payee ||

- Ensures only the named payee’s account receives funds.

Special crossing (specific bank):

- Mark:

|| State Bank of X ||

- Requires the cheque to be processed through that bank.

Not negotiable:

- Mark

|| Not Negotiable ||

- Protects subsequent transferees’ title.

FAQs

Can a crossed cheque be endorsed/assigned to someone else?

A general crossing does not prevent endorsement, but if the cheque is marked “A/C Payee” or “Not Negotiable,” endorsements or transfers have limited or no effect. Local law matters; check bank rules.

What if I receive a crossed cheque but have no bank account?

You generally need an account to deposit it. Traveler’s or cashier’s cheques may be exceptions; otherwise arrange deposit into a known account (yours or a trusted person’s) or ask the issuer for an alternative payment method.

Can the bank refuse to cash a crossed cheque?

Yes, by definition crossed cheques are not cashed at the counter. If crossing is ambiguous or violates bank rules, the bank may return it.

How long before a crossed cheque becomes stale?

Most jurisdictions use 3 months from issue date as a guide, but this varies — check bank policy. Present cheques promptly.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.