Cheques have long been a trusted method of financial transactions. Even in the era of digital payments, they remain important for business dealings, formal payments, and banking documentation. Understanding the different 13 types of cheques is essential to avoid payment issues, fraud risks, and bank rejections.

In this blog post, we explain all major types of cheques, along with their definitions and examples, exactly as shown in the table.

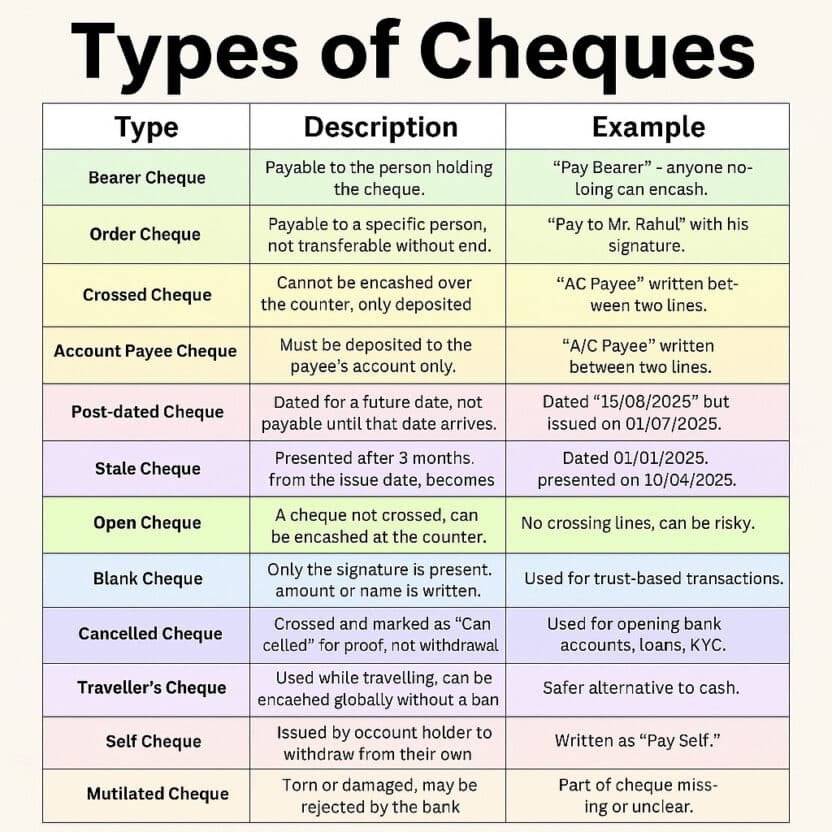

13 Types of Cheques

1. Bearer Cheque

A Bearer Cheque is payable to the person who presents (or “bears”) the cheque at the bank. No identification is required.

Example:

“Pay Bearer” – anyone holding the cheque can encash it.

Best For:

Quick payments; handing cash to someone without needing their name on the cheque.

Risk:

If lost or stolen, anyone can withdraw the money.

2. Order Cheque

An Order Cheque is payable to a specific person whose name is written on the cheque. It cannot be transferred without endorsement.

Example:

“Pay to Mr. Rahul” with the account holder’s signature.

Best For:

Secure payments where the payee should be identifiable.

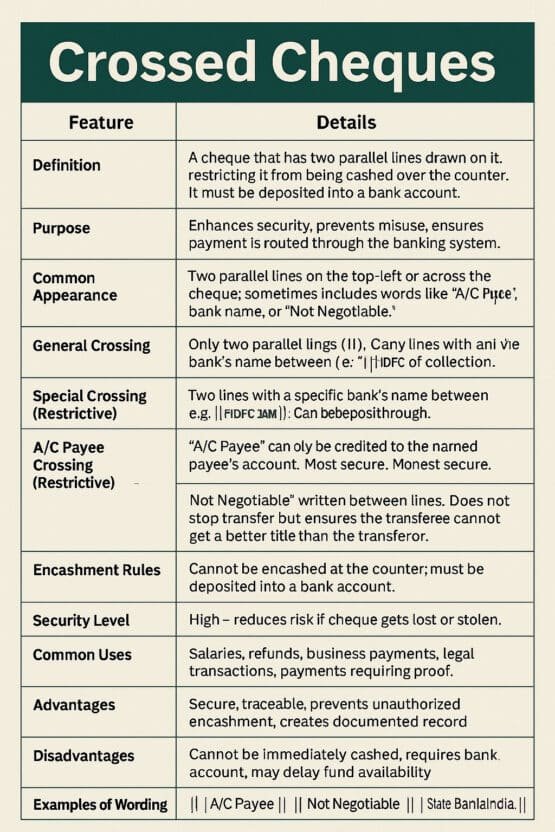

3. Crossed Cheque

A Crossed Cheque cannot be encashed over the counter. It must be deposited into a bank account.

How to Identify:

Two parallel lines on the top left corner.

Benefit:

Reduces the risk of misuse since the amount gets deposited directly.

4. Account Payee Cheque

An Account Payee Cheque is even more secure than a crossed cheque. The amount must be deposited only into the named payee’s bank account.

Example:

“A/C Payee” written between the two crossing lines.

Best For:

Salary payments, refunds, official transactions.

5. Post-Dated Cheque

A Post-Dated Cheque is written with a future date. It cannot be encashed or deposited until that date arrives.

Example:

Dated “15/08/2025” but issued on 01/07/2025.

Usage:

Loan installments, rent payments, scheduled payments.

6. Stale Cheque

A Stale Cheque is one that is presented after 3 months from the date of issue. Banks do not accept it.

Example:

Cheque dated 01/01/2025, presented on 10/04/2025.

7. Open Cheque

An Open Cheque (or uncrossed cheque) can be encashed at the counter. It includes the drawer’s signature both on the front and on the back if endorsed.

Risks:

If lost, anyone can withdraw the funds.

8. Blank Cheque

A Blank Cheque has only the signature of the issuer—no name, no amount.

Usage:

Trusted relationships such as business partners or family, though risky.

9. Cancelled Cheque

A Cancelled Cheque has the word “Cancelled” written across it. It cannot be used to withdraw money.

Used For:

KYC processes, loan applications, mutual funds, salary documentation.

10. Traveller’s Cheque

Traveller’s Cheques are used while travelling and can be encashed globally without a bank account.

Benefit:

Safer than carrying cash; replaceable if lost.

11. Self Cheque

A Self Cheque is issued when the account holder wants to withdraw money from their own account.

Example:

Written as “Pay Self.”

Usage:

Personal cash withdrawals.

12. Mutilated Cheque

A Mutilated Cheque is torn or damaged. If crucial details are missing or unclear, the bank may reject it.

Solution:

The issuer may need to confirm or reissue the cheque.

13. Gift Cheque

A Gift Cheque is given for gifting purposes and usually has a decorative design.

Usage:

Special occasions such as birthdays, weddings, or celebrations.

Table Format

| Type | Description | Example |

|---|---|---|

| Bearer Cheque | Payable to the person holding the cheque. | “Pay Bearer” – anyone holding can encash. |

| Order Cheque | Payable to a specific person, not transferable without endorsement. | “Pay to Mr. Rahul” with his signature. |

| Crossed Cheque | Cannot be encashed over the counter, only deposited into a bank account. | Two parallel lines on top left corner. |

| Account Payee Cheque | Must be deposited to the payee’s account only. | “A/C Payee” written between two lines. |

| Post-dated Cheque | Dated for a future date; not payable until that date arrives. | Dated “15/08/2025” but issued on 01/07/2025. |

| Stale Cheque | Presented after 3 months from the issue date; becomes invalid. | Dated 01/01/2025, presented on 10/04/2025. |

| Open Cheque | Not crossed; can be encashed at the counter. | No crossing lines; riskier. |

| Blank Cheque | Only the signature is present; amount and name not filled. | Used for trust-based transactions. |

| Cancelled Cheque | Marked “Cancelled”; used for proof, not for withdrawal. | Used for opening accounts, loans, KYC. |

| Traveller’s Cheque | Used while travelling; can be encashed globally without a bank account. | Safer alternative to cash. |

| Self Cheque | Issued by account holder to withdraw from their own account. | Written as “Pay Self.” |

| Mutilated Cheque | Torn or damaged; may be rejected by the bank. | Part of cheque missing or unclear. |

| Gift Cheque | Issued for gifting purposes; often decorative. | Issued by banks for celebrations. |

Conclusion

Cheques may seem old-fashioned, but they remain essential for formal, business, and banking transactions. Understanding the different types of cheques—such as bearer, order, crossed, post-dated, cancelled, and more—helps ensure safe and smooth financial dealings.