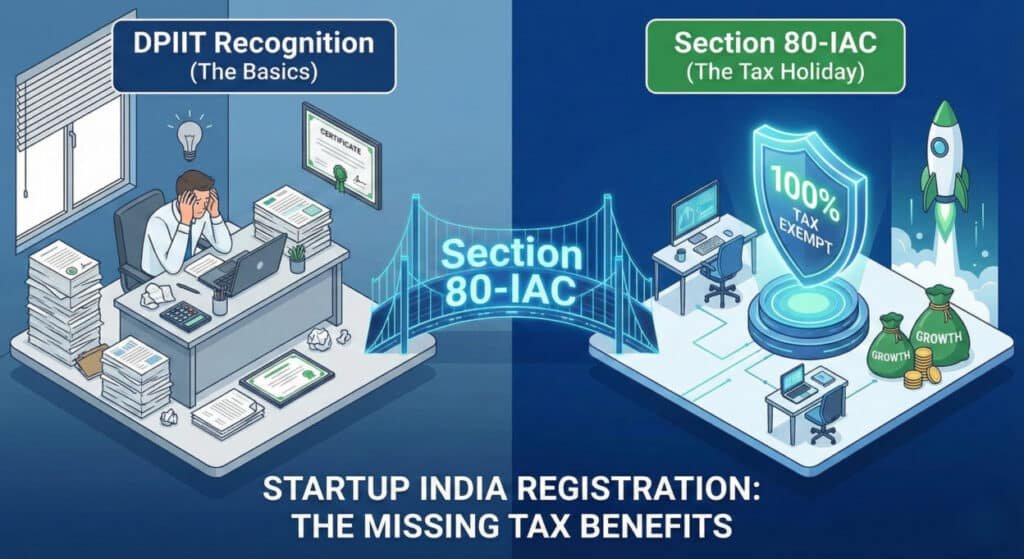

Startup India Registration: The Tax Benefits You Are Likely Missing (Section 80-IAC Updates)

Let’s be honest for a second: running a startup in India is an adrenaline sport. You are juggling product-market fit, hiring, fundraising, and customer acquisition. Somewhere at the bottom of that endless to-do list is “Tax Compliance.” Most founders I speak to comfortably tell me, “Oh, we are sorted. We did the Startup India registration last year.” But when I ask if they are claiming the Section 80-IAC 100% tax holiday, the room usually goes quiet. Here is the harsh reality: 99% of startups confuse “DPIIT Recognition” with “Tax Exemption.” They are not the same thing. By confusing the two, thousands of eligible Indian startups are leaving millions of rupees on the table—money that could have been reinvested into growth, hiring, or R&D. If you are a founder, a CFO, or just an exhausted entrepreneur trying to save money, this guide is for you. We are going to dismantle the confusion around Startup India Registration, dive deep into the mysterious Section 80-IAC, and look at the critical updates for 2024-2025 that you absolutely need to know. The Great Confusion: DPIIT Recognition vs. Section 80-IAC Before we get into the “how-to,” we need to fix the biggest misconception in the Indian startup ecosystem. When you register on the Startup India Portal and get that fancy certificate with a “DIPP” number, you have achieved DPIIT Recognition. This is a great first step. It opens doors to: But it does NOT give you the income tax holiday. To get the tax holiday (where you pay zero income tax for 3 years), you need to clear a second, much harder level: The Inter-Ministerial Board (IMB) Certification. Think of it like this: If you only have the first one, you are still paying taxes. What Exactly is Section 80-IAC? Section 80-IAC of the Income Tax Act, 1961, is arguably the most powerful fiscal incentive for Indian entrepreneurs. The Core Benefit It allows an “Eligible Startup” to avail of a 100% deduction of the profits and gains derived from the eligible business. This means if your startup makes a profit of ₹5 Crores, your taxable income is effectively treated as ZERO. The “3 out of 10” Rule You don’t have to take this exemption immediately. You can choose any 3 consecutive assessment years out of the first 10 years from your incorporation. Why is this strategic? Most startups bleed money in the first few years (Years 1-4). It makes no sense to claim a tax holiday when you have no profit to tax. You can “save” this benefit for Years 7, 8, and 9 when you (hopefully) hit hockey-stick growth and are generating substantial profits. Eligibility Criteria: Do You Qualify? The government doesn’t hand out tax holidays to just anyone. To apply for Section 80-IAC, you must meet a strict checklist. 1. Entity Type You must be a Private Limited Company or a Limited Liability Partnership (LLP). 2. Age of the Company Your startup must have been incorporated on or after April 1, 2016. 3. Turnover Limits Your annual turnover should not exceed ₹100 Crores in any financial year since incorporation. 4. The “Innovation” Factor (The Dealbreaker) This is where most applications get rejected. Your startup must be working towards: The IMB (Inter-Ministerial Board) reviews this subjectively. If you are just a digital marketing agency doing what 5,000 other agencies are doing, you will likely get DPIIT recognition, but you will be rejected for 80-IAC. You need to show differentiation. Recent Updates (2024-2025) You Must Know Tax laws in India are fluid. Here are the critical updates relevant to your Startup India Registration and tax planning. Update 1: The Incorporation Deadline Extension Originally, the sun was supposed to set on this scheme years ago. However, realizing the need to support the ecosystem, the government has extended the deadline. Update 2: The End of Angel Tax (Section 56(2)(viib)) For years, Section 80-IAC was discussed alongside the dreaded “Angel Tax.” Startups had to apply for a separate exemption to avoid being taxed on investment received above Fair Market Value. Step-by-Step Guide: How to Apply for Section 80-IAC Ready to save taxes? Here is the walkthrough. Do not skip steps. Phase 1: The DPIIT Recognition (The Prerequisite) If you haven’t done this yet, do it today. It takes 48-72 hours. Phase 2: The Section 80-IAC Application (The Hard Part) Once you have your DIPP number, the real game begins. Step 1: Access the Dashboard Log in to the Startup India portal. Navigate to “Services” > “Tax Exemption under Section 80-IAC”. Step 2: Fill Form 1 This is the statutory application form. It asks for: Step 3: The Video Pitch (Crucial) You must upload a video link. This isn’t a glamorous marketing commercial; it is a functional explanation of your business. Step 4: The Pitch Deck Upload a PDF pitch deck. This should look like a VC pitch deck but tailored for a government auditor. Focus heavily on: Step 5: Submission and Tracking Once submitted, your application goes to the Inter-Ministerial Board. Why Applications Get Rejected (And How to Avoid It) The acceptance rate for Section 80-IAC is notoriously low (historically under 5-10% of applicants). Why? 1. “Old Wine in a New Bottle” If you simply clone an existing business model (e.g., “Uber for X” or a standard E-commerce store) without any proprietary technology or unique process, the IMB will reject it. 2. Lack of Scalability Consultancies and service-based businesses often struggle here. If your revenue growth is linearly tied to hiring more people (i.e., you sell hours), it’s not considered “scalable” in the tech sense. 3. Regulatory Non-Compliance If you haven’t filed your ITRs or your MoA is generic, it’s an instant rejection. 4. Splitting or Reconstruction You cannot shut down an old company and open a new one just to get tax benefits. If the board suspects “splitting up” of an existing business, you are out. Other Tax Benefits You Might Be Missing While 80-IAC is the king, do not ignore the princes. Section 54 (Capital Gains