Form No 121 is a declaration form prescribed under Rule 211 of the Income Tax Rules. It is filed under Section 393(6) to receive certain specified incomes – such as provident fund payouts, insurance commission, rent, mutual fund units, FD interest, life insurance proceeds, and dividends – without deduction of tax (TDS). It is the new-era equivalent of the older Form 15G/15H, now applicable under the Income Tax Bill 2025 framework.

What Is Form No 121 in Income Tax?

Form No 121 is a statutory declaration form prescribed under Rule 211 of the Income Tax Rules, operative under Section 393(6) of the new Income Tax Code (Income Tax Bill 2025). It is officially titled:

“Declaration under section 393(6) for receipt of certain incomes without deduction of tax”

In plain terms, Form No. 121 is the document you submit to the person or institution paying you a specified income – your bank, insurance company, mutual fund, employer, or any other payer – to declare that your estimated total income for the tax year is nil or below the taxable threshold, and therefore, no TDS (Tax Deducted at Source) should be deducted from that income.

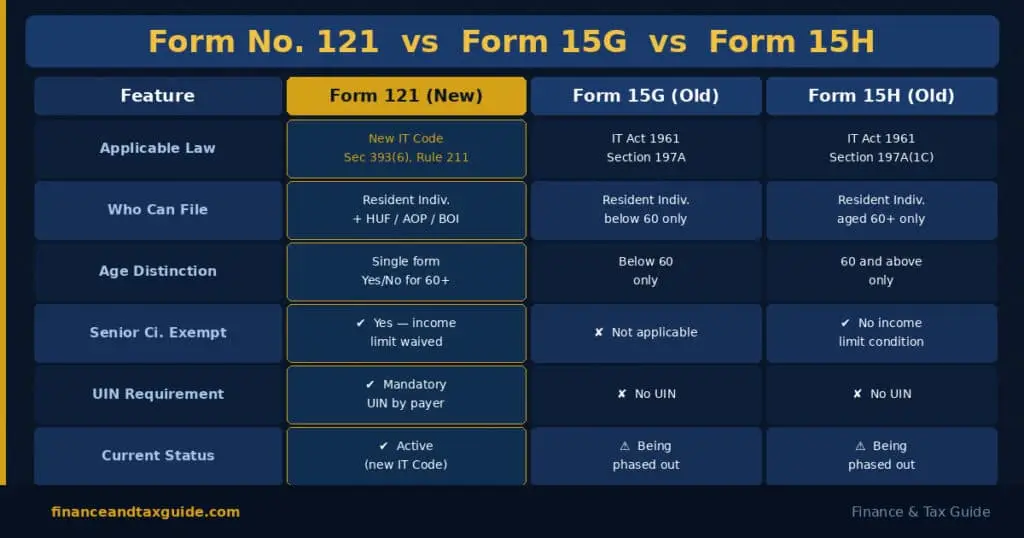

This form is the successor to the old Form 15G and Form 15H under the restructured Income Tax Bill 2025. While Form 15G was for individuals below 60 years and Form 15H was for senior citizens aged 60 and above, Form No. 121 consolidates both into a single unified declaration form with a specific built-in Yes/No condition for those aged 60 or more.

Why Does Form No. 121 Matter?

When you earn income from fixed deposits, provident fund withdrawals, insurance maturity proceeds, dividends, or mutual fund income, the payer is legally required to deduct TDS before paying you. If your total income for the year is below the taxable limit, this TDS deduction reduces your in-hand money unnecessarily and you have to wait months to claim it back as a refund after filing your ITR.

Form No. 121 solves this problem. By submitting it, you declare in advance that your total income is below the taxable threshold (resulting in nil tax), and the payer is legally permitted to release your full amount without cutting any TDS.

Who Should File Form No 121?

As per the form’s Notes and Section 393(6), Form No. 121 can be filed by:

Category 1 – Resident Individual (Section 393(6), Table Sl. No. 1):

A resident individual whose estimated total income for the tax year including the income for which the declaration is made will result in nil tax liability.

- For individuals below 60 years: Your income from the specified sources must not exceed the basic exemption limit (currently ₹2,50,000 under the old regime / ₹3,00,000 under the new regime), AND your total estimated income must result in nil tax.

- For individuals aged 60 years or more at any time during the tax year: The condition that income must not exceed the basic exemption limit does not apply as per the form itself (Field 5(a) and Note 11). As long as total estimated tax is nil (after deductions and rebates), they can file Form No. 121.

Category 2 – Any Other Person (Section 393(6), Table Sl. No. 2):

Any person who is NOT a company, NOT a firm, and NOT a resident individual covered under Sl. No. 1 such as a Hindu Undivided Family (HUF), Association of Persons (AOP), or Body of Individuals (BOI) can also file Form No. 121.

You CANNOT file Form No. 121 if:

- You are a company or firm

- You are a non-resident (NRI)

- Your estimated total income after deductions results in a tax liability (other than nil)

- Your income from specified sources alone exceeds the basic exemption limit AND you are below 60 years of age

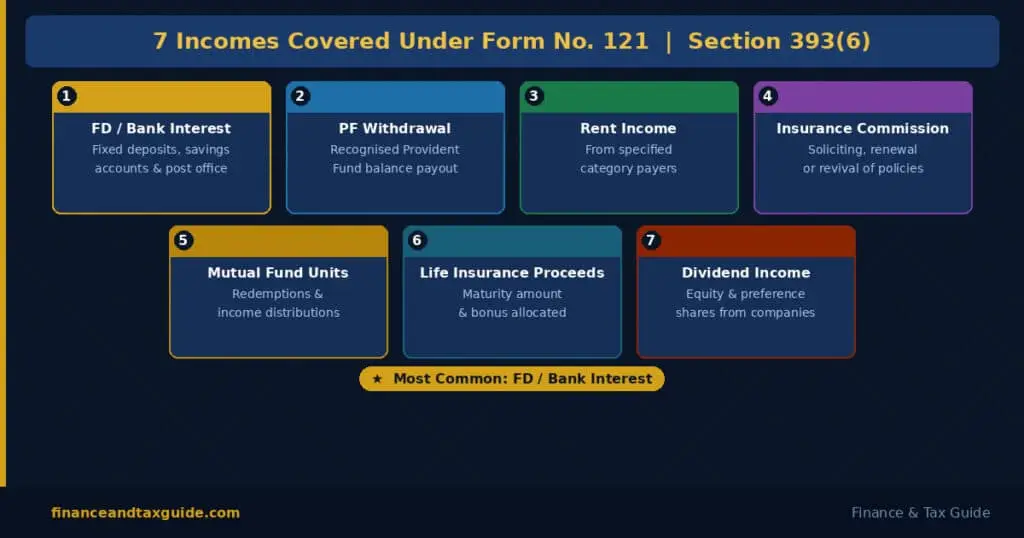

Incomes Covered Under Form No. 121

Form No. 121 applies specifically to the following types of income listed in Note 5 of the form (under Section 393(6)):

| Sl. | Nature of Income | Common Real-Life Situation |

|---|---|---|

| (a) | Payment of accumulated balance due to an employee from a Recognised Provident Fund | PF withdrawal before completing 5 years of service |

| (b) | Insurance commission for soliciting or procuring insurance business including continuance, renewal, or revival of policies | Insurance agents earning commission income |

| (c) | Rent from a specified person | Rental income paid by certain specified category payers |

| (d) | Income from (i) units of a mutual fund, (ii) units from the Administrator of a specified undertaking, or (iii) units from a specified company | Mutual fund redemptions or income distributions |

| (e) | Interest on securities, or interest other than interest on securities by a banking company / co-operative society / post office deposits under notified schemes, or by a specified person | FD interest, savings interest from banks, cooperative banks, post offices |

| (f) | Payment in respect of life insurance policy including bonus allocated on such policy | Life insurance maturity proceeds |

| (g) | Dividend (including dividend on preference shares) declared by a domestic company | Dividend income from equity or preference shares |

Most Common Use Case: The vast majority of Form No. 121 filings are for FD interest income from banks (category (e) above) by individuals and senior citizens with income below the taxable threshold who want their bank to pay full interest without TDS deduction.

Form No 121 vs Form 15G vs Form 15H – Key Differences

| Feature | Form No. 121 (New) | Form 15G (Old) | Form 15H (Old) |

|---|---|---|---|

| Applicable Law | New Income Tax Code, Section 393(6), Rule 211 | Income Tax Act 1961, Section 197A | Income Tax Act 1961, Section 197A(1C) |

| Who Can File | Resident individuals + certain non-individual entities | Resident individuals below 60 | Resident individuals aged 60+ |

| Age Distinction | Single form with a Yes/No field for age 60+ | Below 60 only | 60 and above only |

| Tax Liability Condition | Total estimated tax must be nil | Total estimated tax must be nil | Tax on estimated income must be nil |

| Income Limit for Below-60 | Income from specified sources must not exceed basic exemption limit | Same condition | Not applicable |

| Senior Citizen Exception | Yes, income limit condition does not apply for age 60+ | Not applicable | No income limit condition |

| Unique Identification Number | Yes, mandatory; payer must allot UIN and report in quarterly TDS statement | No | No |

| Quarterly TDS Reporting | Mandatory for payer | Payer files separate statement | Payer files separate statement |

| Current Status | Applicable under new Income Tax Code | Being phased out | Being phased out |

How to Download Form No 121 PDF

Method 1: Official Income Tax India Website

- Visit incometax.gov.in

- Click on “Forms/Downloads” in the top navigation bar

- Select “Income Tax Forms”

- Search for “Form No. 121” or “Form 121”

- Click the PDF icon to download

- Save the 3-page PDF to your device

Method 2: From Your Bank’s Branch or Website

Banks that are required to accept this form provide it for customers:

- At the branch counter – ask the deposits or customer service desk

- Bank’s official website – under “Forms / Downloads” or “Customer Service”

- Net banking portal – under TDS / Tax / FD management sections

Major banks providing it: SBI, HDFC Bank, ICICI Bank, PNB, Bank of Baroda, Canara Bank, Axis Bank, Kotak Mahindra Bank

Method 3: From Your Employer (for PF Withdrawals)

If you are filing Form No. 121 in connection with a provident fund payout, your HR department or the PF trust administrator will provide the form.

Method 4: From Mutual Fund or Insurance Companies

For mutual fund income or life insurance payouts, the AMC or insurance company provides the form typically available on their customer portals or at their offices.

Always download from official sources. The form format is prescribed under Rule 211 an outdated or unofficial version may not be accepted by the payer.

Step-by-Step Guide to Fill Form No 121

Form No 121 has two distinct parts:

- Part A – Filled and signed by you (the declarant)

- Part B – Filled and signed by the payer (bank, company, or institution)

PART A – Declaration by the Declarant

STEP 1 – Field 1: Your Full Name

Enter your complete full name first, middle, and last name without any abbreviations.

| ✅ Correct | ❌ Incorrect |

|---|---|

| RAJESH KUMAR SHARMA | R.K. Sharma |

| PRIYA SURESH AGARWAL | Priya Agarwal |

| MOHAMMED IQBAL HUSSAIN | M.I. Hussain |

As per Note 1 of the form: “In case of individual, the first, middle and last name shall be provided in full without any abbreviations.”

This is one of the most commonly made errors. The payer’s system cross-checks the name against PAN records an abbreviated name can cause a mismatch and result in the form being rejected.

STEP 2 – Field 2: Your Full Address

As per Note 2, your address must include all of the following 8 components:

- Country / Region

- Flat / Door / Building number

- Road / Street / Block / Sector

- PIN / ZIP Code

- Post Office

- Area / Locality

- District

- State

Sample address entry:

Flat No. 304, Shree Apartments,

MG Road, Sector 12,

PIN: 395001,

Post Office: Surat Main,

Area: Athwalines,

District: Surat,

State: Gujarat,

Country: IndiaMissing any component especially the PIN code, District, or State is a common error. Fill all 8 components without fail.

STEP 3 – Field 3: Permanent Account Number (PAN)

Enter your 10-character PAN exactly as it appears on your PAN card.

Example: ABCRS1234P

Tips:

- PAN is alphanumeric – 5 letters, 4 digits, 1 letter

- Cross-check every character before submitting

- An incorrect PAN makes the form invalid; the payer will be obligated to deduct TDS regardless of the declaration

STEP 4 – Field 4: Status

As per Note 3, select your status:

- Individual – if you are a resident individual declaring under Section 393(6), Table Sl. No. 1

- Other person (not a company/firm) – HUF, AOP, BOI, etc., declaring under Section 393(6), Table Sl. No. 2

Most individual taxpayers: select Individual

STEP 5 – Field 5: Residential Status

Select one of the following (as per Note 4):

- Resident – you live in India and meet the residency conditions under the Income Tax Code

- Non-resident – you do not meet residency conditions (note: non-residents cannot file Form No. 121)

- Resident but not ordinarily resident (RNOR) – specific category for returning NRIs

For most taxpayers in India: Resident

STEP 6 – Field 5(a): Are You Aged 60 or More?

This is a Yes / No answer. It has a significant legal impact:

| Your Age | Answer | Impact |

|---|---|---|

| 60 years or above at ANY time during the tax year | Yes | The income limit condition (that income from specified sources must not exceed basic exemption) does NOT apply to you |

| Below 60 throughout the year | No | Income from specified sources must not exceed the basic exemption limit |

This is the built-in replacement for the old Form 15H (senior citizen) vs Form 15G (below 60) distinction.

STEP 7 – Field 6: Email ID

Enter your active email address. The payer may use this for sending confirmation, UIN, or other communication.

Example: rajesh.sharma2025@gmail.com

STEP 8 – Field 7: Contact Number

Enter your country code and mobile number.

| Sub-field | What to Enter |

|---|---|

| Country Code | +91 (for India) |

| Number | Your 10-digit mobile number |

STEP 9 – Field 8: Tax Year

Enter the tax year for which you are making this declaration.

Under the new Income Tax Code, “Tax Year” = the financial year (April 1 to March 31).

For current filings: 2025–26

STEP 10 – Field 9: Nature of Income

Select or write the specific type of income from the 7 categories in Note 5 of the form:

| Your Income | What to Write in Field 9 |

|---|---|

| FD interest at a bank | Interest other than interest on securities by a banking company [Section 393(6), Note 5(e)] |

| PF withdrawal | Payment of accumulated balance from a recognised provident fund [Note 5(a)] |

| Insurance commission | Insurance commission for soliciting/procuring insurance business [Note 5(b)] |

| Mutual fund income | Income in respect of units of a mutual fund [Note 5(d)] |

| Life insurance maturity | Payment in respect of life insurance policy [Note 5(f)] |

| Dividend from shares | Dividend declared by a domestic company [Note 5(g)] |

| Rent from specified person | Rent from a specified person [Note 5(c)] |

Be specific. Write the exact nature of income rather than a generic term like “interest income.”

STEP 11 – Field 10: Estimated Income for This Declaration

Enter the estimated amount in ₹ of the specific income (declared in Field 9) that you expect to receive from this particular payer during the tax year.

Example:

- FD of ₹5,00,000 at 7% p.a. → estimated FD interest = ₹35,000

- Enter: 35000

All amounts are in Indian Rupees (₹) as per Note 14 of the form.

STEP 12 – Fields 11(a) and 11(b): Earlier Form No. 121 Filings This Year

This is one of the most important and most often incorrectly filled sections.

If you have already submitted Form No. 121 to any other payer earlier in the same tax year (e.g., you have FDs at multiple banks and already submitted a Form No. 121 to Bank A), you must disclose that here.

Field 11(a): Total number of Form No. 121 filed with other payers earlier in this tax year

Field 11(b): Aggregate amount of income declared in all those earlier Form No. 121s

If this is your FIRST Form No. 121 for this tax year:

- Field 11(a): 0

- Field 11(b): Nil / 0

Why this matters: The payer adds Field 10 + Field 11(b) to get your aggregate income. If the total pushes your income above the taxable limit, the payer is legally required to reject your declaration and deduct TDS. Hiding earlier filings constitutes a false declaration under Section 482.

STEP 13 – Field 12: Aggregate Income for Declaration (Tax Year)

Formula: Field 12 = Field 10 + Field 11(b)

This is typically auto-calculated in digital forms.

Example:

- Field 10 (this bank’s FD interest): ₹35,000

- Field 11(b) (declared in earlier forms): ₹20,000

- Field 12 = ₹55,000

STEP 14 – Field 13: Estimated Total Income of the Tax Year

This is your estimated gross total income from ALL sources for the entire tax year including the amount in Field 12. Use our free Income Tax Calculator to verify your tax liability before filing Form No. 121.

As per Notes 7 and 10:

- Include income from salary, business, house property, capital gains, and other sources

- Deduct allowable deductions under Chapter VIII (equivalent of Chapter VI-A)

- Set off losses under “Income from House Property”

- Apply rebate under Section 156

The resulting estimated total income, after these adjustments, must result in a nil tax liability for this declaration to be legally valid.

Example Calculation:

| Income / Deduction | Amount |

|---|---|

| FD Interest (Field 12) | ₹55,000 |

| Dividend income | ₹10,000 |

| Total Income | ₹65,000 |

| Less: Deductions (Chapter VIII) | ₹(0) |

| Estimated Total Income (Field 13) | ₹65,000 |

| Tax on ₹65,000 (well below ₹2,50,000) | Nil ✓ |

STEP 15 – Field 14: ITR Filed for Previous Two Tax Years

Fill in your ITR filing details for the last two tax years:

| Sl. No. | Tax Year | Acknowledgement Number | Return Income (₹) |

|---|---|---|---|

| 1. | 2023–24 | 123456789012345 | 62,000 |

| 2. | 2022–23 | 987654321098765 | 58,500 |

If you did not file an ITR in a particular year because your income was below the filing threshold, write: “Not filed – income below taxable limit” or If you have not filed your ITR yet, see our step-by-step guide to filing ITR for FY 2025-26.

This section helps the payer assess the consistency and credibility of your declaration.

STEP 16 – Declaration and Signature

Read the declaration fully before signing. By signing, you certify:

(i) All information is correct, complete, and truly stated.

(ii) The income referred to in the form is not includible in any other person’s total income under Sections 96 to 99 (income clubbing provisions e.g., you cannot file this form for income that would be clubbed with your spouse’s or minor child’s income).

(iii) Tax on your estimated total income (Field 13), including the income in Field 12, will be nil for the tax year.

(iv) The income in Field 12 does not exceed the maximum amount not chargeable to tax (i.e., the basic exemption limit). This clause does not apply to resident individuals aged 60 or more.

(v) If the declaration is found to be false, you will be liable to prosecution/penalty under the Act (Section 482 – criminal prosecution).

Fill in:

- Place: City where you are signing (e.g., Surat)

- Date: DD/MM/YYYY (e.g., 01/04/2025)

- Signature: Your full signature (not initials)

- Name: Print your name below the signature

As per Note 12: “Before signing the verification, the declarant should satisfy himself that the information furnished in the declaration is true, correct and complete in all respects.”

PART B – Verification by the Person Responsible for Paying Income {#part-b}

Part B is completed by the PAYER – the bank, insurance company, mutual fund, or other institution paying your income. You do not fill Part B yourself. However, understanding what it contains helps you ensure the process is completed correctly.

Section 1 of Part B: Payer’s Details

| Field | What the Payer Fills |

|---|---|

| 1. Name | Full name of the bank / institution |

| 2. Address | Complete address (all 8 components per Note 2) |

| 3. TAN | Tax Deduction and Collection Account Number (10 characters) |

| 4. PAN | Payer’s PAN (10 characters) |

| 5. Email ID | Official payer email |

| 6. Contact Number | Country code + phone |

| 7. Tax Year | 2025–26 |

Section 2 of Part B: Declarant Details as Received

The payer re-records your details and adds critical new fields:

| Field | Content |

|---|---|

| 8. Name of Declarant | Your name (from Part A, Field 1) |

| 9. PAN | Your PAN (from Part A, Field 3) |

| 10. Unique Identification Number (UIN) | Assigned by the payer – a unique tracking number for this specific declaration |

| 11. Date of Birth | Your date of birth (DD/MM/YYYY) |

| 12. Address | Your address (from Part A, Field 2) |

| 13. Email ID | Your email (from Part A, Field 6) |

| 14. Contact Number | Your contact (from Part A, Field 7) |

| 15. Estimated Income (this declaration) | From Part A, Field 10 |

| 16. Estimated Total Income | From Part A, Field 13 |

| 17. Aggregate Income (tax year) | From Part A, Field 12 |

| 18. Date Declaration Received | Date payer received your signed Part A |

The UIN (Field 10 of Part B) is a key new feature in Form No. 121. As per Note 8 of the form: “The person responsible for paying income shall allot a unique identification number to all Form No. 121 received by him during a quarter of the tax year and report the same in TDS statement furnished for the same quarter.” This creates a complete, traceable, government-visible audit trail for every Form No. 121 submitted in India.

Part B Declaration / Certification

The authorised person at the payer signs:

“I (name of authorized person) having Permanent Account Number ……… hereby certify that the information pertaining to the declarant(s) above has been duly furnished.”

They enter: Signature, Name, Place, Date.

Form No. 121 Filled Sample Explained Field by Field

Scenario: Ms. Priya Suresh Agarwal, a 58-year-old homemaker in Surat, holds a Fixed Deposit of ₹5,00,000 with SBI earning 7% p.a. interest = ₹35,000 per year. She has no other income. She wants to avoid TDS on this FD interest.

Filled Part A Sample

| Field | Priya’s Entry |

|---|---|

| 1. Name | PRIYA SURESH AGARWAL |

| 2. Address | Flat No. 12, Shri Nagar Apartments, Ring Road, Surat, PIN: 395002, Post Office: Surat Main, Area: Adajan, District: Surat, State: Gujarat, Country: India |

| 3. PAN | ABTPA5678Q |

| 4. Status | Individual |

| 5. Residential Status | Resident |

| 5(a). Age 60 or more? | No |

| 6. Email ID | priyaagarwal.srt@gmail.com |

| 7. Contact Number | +91 98765 43210 |

| 8. Tax Year | 2025–26 |

| 9. Nature of Income | Interest other than interest on securities by a banking company [Section 393(6), Note 5(e)] |

| 10. Estimated Income | ₹35,000 |

| 11(a). Earlier forms filed | 0 |

| 11(b). Earlier aggregate income | Nil |

| 12. Aggregate income (tax year) | ₹35,000 |

| 13. Estimated Total Income | ₹35,000 (no other income; well below ₹2,50,000 basic exemption; tax = Nil) |

| 14. ITR – Year 1 | 2023–24, Ack No. 234567890123456, Income ₹32,000 |

| 14. ITR – Year 2 | 2022–23, Ack No. 345678901234567, Income ₹28,000 |

| Place | Surat |

| Date | 01/04/2025 |

| Signature | [Full signature of Priya Agarwal] |

Filled Part B – Sample

| Field | SBI Entry |

|---|---|

| 1. Name | Bank , Branch, |

| 3. TAN | SRTB01234A |

| 4. PAN | AAAAS1234B |

| 10. UIN | SBI/ADJ/2526/Q1/00145 |

| 11. Date of Birth | 15/06/1967 |

| 18. Date of Receipt | 01/04/2025 |

Form No. 121 for SBI, HDFC Bank & PNB

Form No. 121

SBI is one of the most common institutions where customers file Form No. 121 to prevent TDS on FD interest.

Process at SBI:

- Visit your SBI home branch (the branch where the FD is held) or log in to onlinesbi.sbi

- Download Form No. 121 from SBI’s website or collect a printed copy at the branch counter

- Fill Part A completely with all 14 fields and sign the declaration

- Submit to the branch the designated officer completes Part B, assigns the UIN, and notes the date of receipt

- The bank updates your FD account status to release full interest without TDS deduction

- Submit a fresh Form No. 121 every April the form is valid for one tax year only

For SBI net banking users: Log in → My Accounts → Fixed Deposits → Tax Declaration / Form Submission → Submit Form 121 online

Important for SBI FD holders: If you hold FDs at multiple SBI branches, you must submit a separate Form No. 121 at each branch where the FD is held. Each branch processes declarations independently. Disclose earlier filings in Field 11 of each subsequent form.

Form No. 121 at HDFC Bank

Process at HDFC Bank:

- Log in to netbanking.hdfcbank.com or visit your HDFC Bank home branch

- Navigate to: Accounts → Fixed Deposits / Investments → Tax Exemption → Form 121

- Fill and submit the form online (pre-filled fields will appear for existing customers) or collect a physical form at the branch

- HDFC Bank processes the form, assigns a UIN, and updates the TDS flag on your FD

- You receive a confirmation via registered email or SMS

HDFC Bank’s net banking portal allows fully digital submission for existing customers. Check the TDS / Tax section under your account management dashboard.

Form No. 121 at PNB (Punjab National Bank)

Process at PNB:

- Visit your PNB home branch or log in to ibanking.pnb.bank.in

- Request Form No. 121 at the deposits or customer service counter, or download from PNB’s forms section online

- Fill Part A with all required details

- Submit to the branch manager or deposits officer

- The branch completes Part B, assigns the UIN, and updates your FD account

- Retain the stamped acknowledgement copy for your records

PNB customers with FDs at multiple branches must visit each branch individually and update Field 11 of each form to disclose prior filings.

Important Notes from the Form

The official Form No. 121 contains 14 Notes. Here are the most critical ones explained in plain language:

Note 1 (Full Name): Always write full name first, middle, and last without abbreviations.

Note 2 (Full Address): Address must include all 8 components: country, flat/door/building, road/street, PIN code, post office, area/locality, district, and state.

Note 3 (Status): The form is for resident individuals (Sl. No. 1) or other persons who are not a company, firm, or such individual (Sl. No. 2).

Note 5 (Nature of Income): Only the 7 specific income types listed (a) through (g) are eligible. Other income types are not covered by Form No. 121.

Note 8 (UIN – Unique Identification Number): “The person responsible for paying income shall allot a unique identification number to all Form No. 121 received by him during a quarter of the tax year and report the same in TDS statement furnished for the same quarter.” Every Form No. 121 is now tracked in government TDS records by UIN.

Note 9 (Acceptance by Payer): “The person responsible for paying income shall accept the declaration where the tax on declarant’s estimated total income will be nil.” If all conditions are met, the payer has no discretion to refuse.

Note 10 (Estimated Total Income Calculation): Total income is calculated after deductions under Chapter VIII, set-off of house property losses, and rebate under Section 156.

Note 11 (When Payer Must Reject): For declarants below 60, the payer must reject the form if the income from specified sources exceeds the basic exemption limit.

Note 12 (Penalty for False Declaration): A false declaration is liable for prosecution under Section 482 of the new Income Tax Code.

Note 13 (Pre-Filled Fields): Some fields may be pre-filled in digital systems always verify pre-filled data before submitting.

Note 14 (Currency): All amounts are in Indian Rupees (₹) unless otherwise stated.

Common Mistakes to Avoid

Mistake 1: Abbreviated Name in Field 1 The form explicitly requires full names without abbreviations. R.K. Sharma instead of Rajesh Kumar Sharma can trigger rejection.

Mistake 2: Incomplete Address in Field 2 Missing the PIN code, Post Office, District, or State is extremely common. All 8 address components are mandatory.

Mistake 3: Not Disclosing Earlier Filings in Field 11 If you have already filed Form No. 121 with another bank or institution earlier in the same tax year, you must disclose it. Omitting this is a false declaration under Section 482.

Mistake 4: Incorrect or Generic Nature of Income in Field 9 Writing “interest income” is too generic. Specify the exact sub-category from Note 5 (a) through (g).

Mistake 5: Overstating Deductions to Bring Tax to Nil Inflating deductions in Field 13 so that the tax appears to be nil, when it actually isn’t, constitutes a punishable offence.

Mistake 6: Not Filing a Fresh Form Each Year Form No. 121 is valid for one tax year only. Many people assume the bank will carry forward last year’s form automatically they will not. Submit a fresh form every April.

Mistake 7: Submitting at the Wrong Branch For bank FDs, submit Form No. 121 at the specific branch where your FD is held. Submitting at a different branch even of the same bank does not protect your FD from TDS.

Mistake 8: Confusing Form No. 121 with the Employer Investment Declaration Form Form No. 121 is for preventing TDS on non-salary incomes like FD interest, dividends, insurance payouts. It is not the same as the annual investment declaration (Form 12BB) submitted to your employer for salary TDS.

Mistake 9: Ignoring the UIN After submitting, the payer assigns a UIN. Keep a record of this UIN it is the reference number in the government’s TDS tracking system for your declaration.

Mistake 10: Filing When Not Eligible If your estimated total income exceeds the basic exemption limit AND you are below 60, or if your income from specified sources alone exceeds the basic exemption limit, you are not eligible to file. Filing anyway is a false declaration.

Frequently Asked Questions (FAQs)

What is Form No 121 in income tax?

Form No. 121 is a declaration form under Rule 211, filed under Section 393(6) of the new Income Tax Code. It is submitted to a payer (bank, company, institution) to declare that your estimated total income is below the taxable limit, so that specified incomes. like FD interest, dividends, PF withdrawals, mutual fund income, insurance proceeds can be received without TDS deduction.

Is Form No. 121 the new Form 15G?

Yes, essentially. Form No. 121 under the new Income Tax Code serves the same purpose as the old Form 15G (for below-60 individuals) and Form 15H (for senior citizens aged 60+) under the Income Tax Act 1961. It consolidates both into a single form, with a Yes/No field for age 60+. As the new Income Tax Code replaces the old Act, Form No. 121 replaces Form 15G and 15H.

How to fill Form No. 121 income tax?

Fill Part A: enter your full name (no abbreviations), full address (8 components), PAN, status, residential status, age condition, email, contact, tax year, nature of income (from Note 5 categories), estimated income, prior filings disclosure (Field 11), aggregate income, estimated total income, and last 2 years’ ITR details. Read the declaration, sign, and submit to the payer. The payer completes Part B.

How to download Form No. 121 income tax PDF?

Download from the official Income Tax India website (incometax.gov.in) under Forms/Downloads → Income Tax Forms. Banks like SBI, HDFC Bank, and PNB also provide it on their websites and at branch counters.

What incomes are covered under Form No. 121?

Seven categories: (a) PF accumulated balance, (b) insurance commission, (c) rent from specified persons, (d) mutual fund / specified undertaking units income, (e) FD/bank/post office interest, (f) life insurance policy proceeds, (g) dividends from domestic companies.

Can I file Form No. 121 for FD interest at SBI?

Yes. FD interest is covered under category (e) of Section 393(6). If your estimated total income is nil after deductions, you file Form No. 121 with the SBI branch holding your FD. The bank cannot deduct TDS once a valid declaration is on record.

What is the Unique Identification Number (UIN) in Form No. 121?

As per Note 8, every payer must assign a UIN to each Form No. 121 received during a quarter and report it in their quarterly TDS statement. This creates a traceable audit trail in the government’s TDS system a major difference from the old Form 15G/15H.

What happens if I make a false declaration in Form No. 121?

Filing false information in Form No. 121 is a criminal offence under u003cstrongu003eSection 482u003c/strongu003e of the new Income Tax Code, liable to prosecution and penalty.

Can I file Form No. 121 with multiple banks in the same year?

Yes, but you must disclose each prior filing in Field 11 of every subsequent Form No. 121. The aggregate income from all declarations combined must still result in nil tax for all the declarations to remain valid.

Is Form No. 121 applicable for NRIs?

No. Form No. 121 is only for u003cstrongu003eresident individualsu003c/strongu003e and eligible resident non-individual entities. Non-residents have separate provisions.

What is Form No. 121 for SBI or HDFC Bank?

Both banks are required to accept Form No. 121 from eligible customers to prevent TDS on FD interest income. You submit Part A to your home branch; the bank fills Part B, assigns a UIN, and adjusts your account to release interest without TDS. Submit fresh every financial year in April.

What is Form 121 income tax word format?

The official Form No. 121 is published by the Income Tax Department in PDF format. For an editable Word format (.docx), check the official Income Tax India website or request it from your bank or employer. Some institutions provide it in editable PDF or Word format for convenience.

Final Pre-Submission Checklist for Form No. 121

Before submitting your Form No. 121, verify every point:

Part A – Personal Details:

- Name written in FULL first, middle, last no abbreviations

- Address includes all 8 required components (country, flat, road, PIN, post office, area, district, state)

- PAN number entered correctly (10 characters, alphanumeric)

- Status correctly selected (Individual / Other)

- Residential status = Resident

- Age 60+ answered correctly (Yes / No)

- Tax year = 2025–26

Part A – Income Details:

- Nature of income correctly identified from Note 5 categories (a) to (g)

- Estimated income (Field 10) is realistic and accurate

- All earlier Form No. 121 filings disclosed in Fields 11(a) and 11(b)

- Field 12 correctly equals Field 10 + Field 11(b)

- Estimated total income (Field 13) includes ALL sources of income

- Tax on estimated total income (Field 13) = Nil after all deductions and rebates

- Previous 2 years’ ITR details filled in Field 14

Declaration:

- Declaration read fully and understood

- Form signed with full signature (not initials)

- Place and Date filled in

- Name printed below signature

Submission:

- Submitting to the correct branch / payer (where the income originates)

- Retaining a copy of the signed declaration for your records

- Noting down the UIN provided by the payer after submission

Conclusion

Form No. 121 is a legally significant document that protects your in-hand income from unnecessary TDS deductions. For anyone whose total income is below the taxable threshold whether a homemaker with only FD interest, a retired individual living off dividends, an insurance agent with modest commission, or an employee expecting a PF payout submitting Form No. 121 correctly at the start of every tax year is essential financial hygiene.

Under the new Income Tax Code, Form No. 121 consolidates the old Form 15G and Form 15H into one unified form, adds stronger accountability through the Unique Identification Number (UIN) system, and mandates quarterly reporting by payers making the declaration process more transparent and trackable than ever before.

Key takeaways:

- Form No. 121 is filed under Section 393(6), prescribed under Rule 211

- It covers 7 specific income types FD interest, PF payouts, dividends, mutual fund income, insurance proceeds, insurance commission, and rent

- It has two parts: Part A by you (declarant), Part B by the payer

- It replaces Form 15G and Form 15H under the new Income Tax Code

- Valid for one tax year only submit fresh every April

- A false declaration attracts criminal prosecution under Section 482

- Always keep a record of the UIN assigned by the payer

For personalised advice on whether you qualify to file Form No. 121 for your specific income situation, consult a qualified Chartered Accountant or tax professional.

Need help with TDS, ITR filing, or income tax compliance? Our expert team at Finance and Tax Guide is here to help.

This article is for general informational purposes based on the official Form No. 121 as prescribed under Rule 211 and Section 393(6) of the new Income Tax Code (Income Tax Bill 2025). Always refer to the official Income Tax India website (incometax.gov.in) for the latest version of the form and applicable rules before filing.

He founded Finance and Tax Guide to simplify complex tax and accounting topics for Indian small businesses, entrepreneurs, and individual taxpayers.

His expertise includes:

• GST Registration and Return Filing

• Income Tax Return (ITR) Filing

• TDS and TCS Compliance

• Business Bookkeeping

• Financial Accounting

• Tax Planning for Small Businesses

Every article published on Finance and Tax Guideis based on practical accounting experience and current Indian tax laws to provide accurate,

easy-to-understand financial guidance.