There is a Misconception that GST is paid on the Selling price of the goods and services. Though this fact is true for all the end-recipients of goods or/and services. For a ‘GST registered person’, the story is entirely different.

Since, all the GST registered Persons can avail Input tax credit (ITC), because of which the GST payable by them largely boils down to the ‘profit’ or ‘mark-up’ component of the goods or/and services.

Fundamental concept of Input Tax Credit

Input Tax Credit (ITC) is a mechanism under the GST system that allows businesses to offset the tax they pay on purchases (inputs) against the tax they collect on sales (outputs). This ensures that GST is ultimately charged only on the value added at each stage of the supply chain.

How ITC Works

Let us understand with this the example, here –

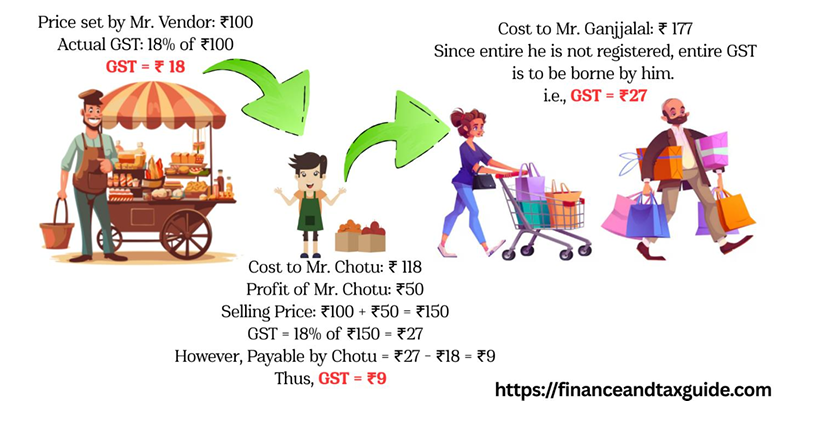

- Mr. Vendor is the original supplier, engaged in the business of B2B (Business to Business) transactions.

- Mr. Chotu is a retailer chain, who operates on a B2C (Business to Customer) transactions.

- Lastly, Mr. Ganjjalal is the end-recipient, who is the actual customer.

Mr. Vendor sets up his stall and prices the goods at ₹100. He charges 18% GST on this amount, making the total ₹118 for Mr. Chotu, who is purchasing the goods to resell. Because Mr. Chotu is registered under GST, the ₹18 he pays in tax to Mr. Vendor becomes his Input Tax Credit (ITC). Next, Mr. Chotu adds a ₹50 profit margin to the original base of ₹100, raising the new base price to ₹150. He then charges 18% GST (i.e., ₹27) on this ₹150 when selling to Mr. Ganjalal, the final consumer, bringing the total to ₹177.

Since Mr. Chotu already paid ₹18 in GST to Mr. Vendor and claimed it as ITC, his net tax liability to the government is only ₹9 (₹27 collected minus ₹18 of ITC). Mr. Ganjalal, who is not registered for GST, must bear the full ₹27 tax as part of his final purchase cost, illustrating how ITC ensures that only the value added at each stage is taxed and that the ultimate tax burden rests with the end consumer.

| Particulars | Mr. Vendor | Mr. Chotu | Mr. Ganjalal |

| Base Price | ₹ 100 | ₹100 (bought) + ₹50 (profit) = ₹150 | ₹150 (included in total) |

| GST Rate | 18% | 18% | — |

| GST Amount | ₹18 (on ₹100) | ₹27 (on ₹150) | ₹27 (included in total) |

| Total Price Paid | — | ₹118 (to Vendor) | ₹177 (to Chotu) |

| Input Tax Credit (ITC) | — | ₹18 (paid to Vendor) | None |

| Net GST Payable | ₹ 18 | ₹27 – ₹18 = ₹9 | None (consumer) |

Conditions for Claiming Input Tax Credit

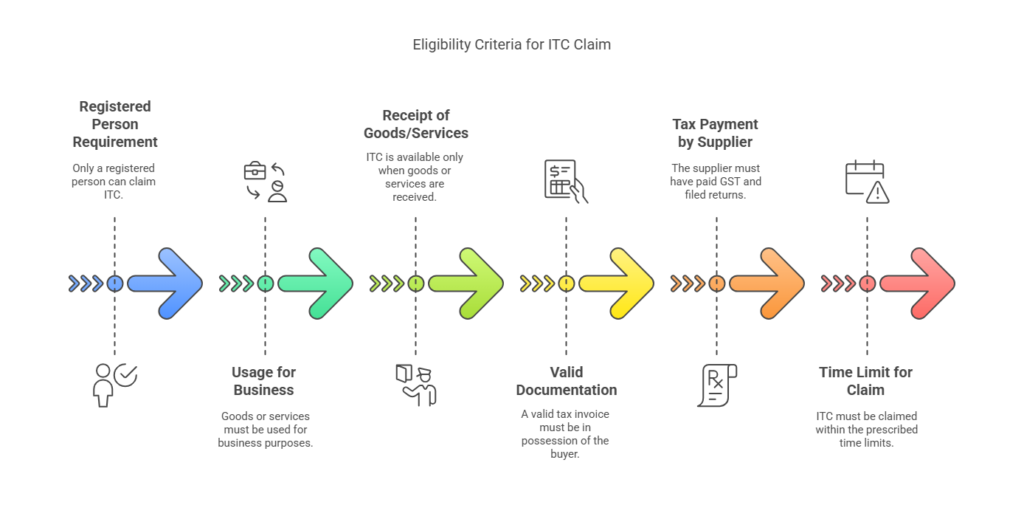

Section 16 of the CGST Act – Eligibility for ITC

- Registered Person Requirement

Only a registered person can claim ITC on inputs, input services, or capital goods used in the course or furtherance of business.

- Usage for Business

The goods or services must be used for business purposes and not for personal consumption.

- Receipt of Goods/Services

ITC is available only when the goods or services are actually received by the claimant.

- Valid Documentation

A valid tax invoice (or debit note) must be in the possession of the buyer. This invoice should detail the GST charged by the supplier.

- Tax Payment by Supplier

The supplier must have paid the GST to the government and must have filed the requisite returns, ensuring that the credit appears in the recipient’s electronic ledger.

- Time Limit for Claim

ITC must be claimed within the prescribed time limits—usually by the due date of the relevant return or before the claim for any refund is initiated.

Section 17 of the CGST Act – Apportionment of Credit

- Apportionment for Mixed Supplies

If goods or services are used partly for taxable supplies and partly for exempt supplies, the ITC must be apportioned accordingly. Full credit cannot be claimed if a part of the supply is exempt.

Section 18 of the CGST Act – Verification and Matching

- Matching of Invoice Details

For the ITC to be available, the details of the invoice provided by the supplier must match with those reported in the recipient’s GST returns.

- Conditions for Reversal

If discrepancies occur or if the supplier’s return is not filed, the ITC may need to be reversed.

Additional Conditions and Restrictions (as per GST Rules and Notifications)

- Restrictions on Certain Inputs

ITC is not available on certain goods or services like:

- Inputs used for personal consumption.

- Certain motor vehicles (with specific exceptions).

- Goods/services where ITC is specifically blocked by law.

- Proper Utilization of ITC

The claimed ITC must be utilized within a prescribed period, ensuring that it is not carried forward indefinitely.

- Documentation Beyond Invoices

Additional supporting documents (such as debit/credit notes and e-way bills) are required to substantiate the claim.

Chart Summary for Compliance for availing ITC

| Category | Conditions & Requirements |

| Eligibility (Sec.16) | Registered person only |

| Goods/services used for business | |

| Actual receipt of goods/services | |

| Documentation & Compliance | Valid tax invoice or debit note |

| E-way bill (if applicable) | |

| Time & Utilization | ITC must be claimed within the due date |

| ITC must be utilized within the prescribed period | |

| Supplier’s Filing & Payment | Supplier must file GST return |

| Tax must be paid to the government | |

| Apportionment (Sec.17) | ITC must be apportioned for mixed supplies |

| Full credit not allowed for exempt supplies | |

| Verification (Sec.18) | Invoice details must match with GST returns |

| ITC may be reversed if mismatch occurs | |

| Restrictions & Exclusions | No ITC on personal use or blocked goods/services |

| Certain motor vehicles, specific inputs excluded |

Written by – Haard Joshi