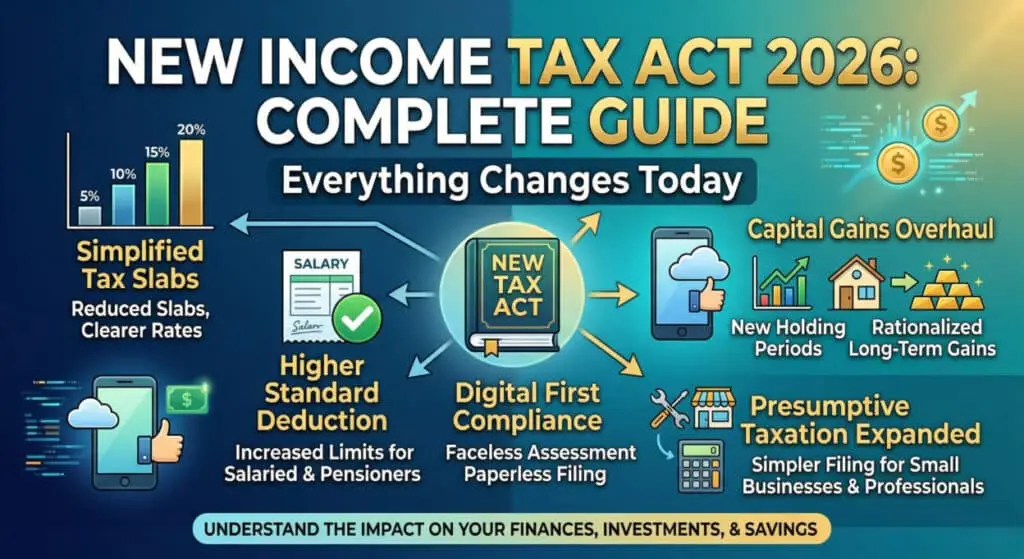

New Income Tax Act 2026: Complete Guide Everything Changes Today

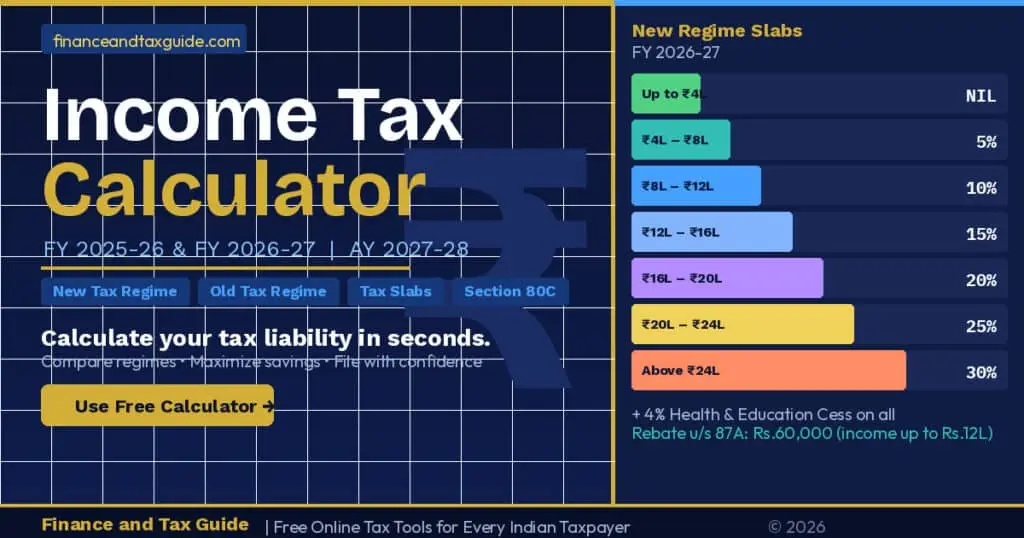

Today is the day India’s tax system officially steps into a new era. The New Income Tax Act 2026 has come into force from 1st March 2026, replacing the six-decade-old Income Tax Act of 1961. If you pay taxes, run a business, or simply earn a salary — this guide is your complete roadmap to understanding what has changed and what you must do next. Why Was the Old Income Tax Act Replaced? The Income Tax Act of 1961 was a monumental piece of legislation for its time, but over six decades it had grown into an unwieldy document of over 800 sections, thousands of sub-sections, and so many provisos that even seasoned chartered accountants needed to cross-reference multiple circulars just to file a routine return. The government’s stated goal with the New Income Tax Act 2026 was straightforward: simplify, modernise, and reduce litigation. The new Act has reportedly shrunk the overall text by nearly 60%, rewritten provisions in plain language, and eliminated redundant sections that were holdovers from an entirely different economic era. Key Fact: The New Income Tax Act 2026 officially becomes effective from 1st March 2026. All income earned from this date onward will be governed by the new Act, though transitional provisions exist for income already assessed under the old Act. What Are the Major Changes in the New Income Tax Act 2026? Here are the most impactful changes, explained in plain terms: 1. Simplified Language and Structure The new Act uses direct, modern English. Legal jargon like ‘notwithstanding anything contained in the foregoing provisions’ has been replaced with plain sentences that a college graduate can follow without a law degree. This alone is expected to reduce tax disputes significantly. 2. Consolidated Tax Regimes The old Act had two competing tax regimes. The new Act consolidates both into a cleaner structure while preserving the option to choose based on your financial situation. 3. Updated Income Tax Slabs for FY 2026-27 The slab structure has been revised to offer higher basic exemption and more progressive rates at the upper end. how to calculate income tax on salary under the new regime. Here is a snapshot of the new tax slabs: Income Range New Regime Rate Old Regime Rate Up to ₹3,00,000 Nil Nil ₹3,00,001 – ₹7,00,000 5% 5% ₹7,00,001 – ₹10,00,000 10% 20% ₹10,00,001 – ₹12,00,000 15% 30% ₹12,00,001 – ₹15,00,000 20% 30% Above ₹15,00,000 30% 30% 4. Changes to Deductions and Exemptions Section 80C (investments up to ₹1.5 lakh) remains largely intact but has been renumbered. HRA exemption rules have been simplified. Standard deduction for salaried individuals has been enhanced. 5. Digital-First Filing Infrastructure The new Act formally recognises e-filing as the primary mode of compliance. Stricter timelines and automatic processing triggers mean the department can act on discrepancies faster than before. What Stays the Same? Income is still classified into five heads: salary, house property, business/profession, capital gains, and other sources. TDS mechanisms continue to operate broadly as before. The concept of previous year and assessment year is retained. Important: The transition from the old Act to the new Act is not retroactive. Income earned in FY 2025-26 will still be assessed under the provisions of the Income Tax Act 1961. The new Act governs income from FY 2026-27 onwards. For how the New Income Tax Act affects your bookkeeping and TDS accounting, refer to our Complete Guide to Accounting in India 2026. What Should You Do Right Now? Step 1: Review Your Tax Regime Choice With the new slab structure in place, the math on whether the new or old regime saves you more may have shifted. Run the numbers or speak to your CA. Step 2: Check Your Investments Before 31st March If you have deductions pending under 80C, 80D, or NPS, the window closes on 31st March 2026. Step 3: Read the Dedicated Posts on This Site We are covering every aspect of the New Income Tax Act 2026 this month — slabs, deductions, compliance deadlines, and more. Final Thoughts The New Income Tax Act 2026 is, by most measures, a genuine improvement over the 1961 Act. It is cleaner, more readable, and better aligned with a digital economy. But like any major legislative shift, it comes with a learning curve. This website will be your guide through that curve. Bookmark this page, subscribe to our YouTube channel, and follow along as we break down every section of the new Act in plain language throughout March 2026.