Section 64 Income Tax rules prevent tax evasion through “clubbing of income.” Specifically, Section 64 prevents individuals from reducing their tax liability by transferring income or assets to family members, such as a spouse or minor children, while still indirectly enjoying the benefits

What is Section 64 Income Tax Clubbing?

Section 64 of the Income Tax Act contains clubbing of income rules to prevent taxpayers from illegally reducing their tax liability by transferring assets or income to family members.

If you transfer income to a close relative to reduce your taxes, the tax department will add (club) that income back to your taxable income.

Why Does Section 64 Exist?

Many taxpayers try to reduce taxes by:

- Gifting property/money to their spouse

- Investing in their child’s name

- Transferring assets to relatives

Section 64 stops this tax evasion loophole by “clubbing” such income with the original taxpayer’s earnings.

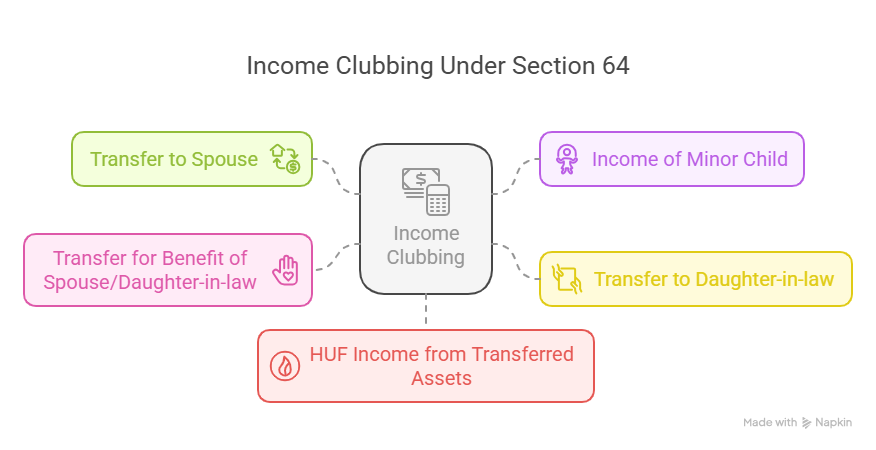

5 Scenarios Where the Income Tax Department Clubs Income

These Are the Main Cases Where Tax Authorities Club Income

1. Transfer of income to Spouse [Section 64 (1)(iv)]

Rule: The tax department adds any income (interest, rent, dividends) from assets you gift your spouse without payment to your taxable income.

Example:

- Mr. A gift ₹10 lakh to your wife → She invests it in FD → ₹50,000 interest earned

Tax Result:

- ₹50,000 is taxed in your hands, not hers.

2. Income of Minor Child [Section 64 (1A)]

Rule: The law clubs income earned by children below 18 (except from their own skills/labour) with the higher-earning parent’s income.

⚠ Exceptions:

- However, income from a child’s own talent—for example, acting or sports prizes—is exempt.

- Similarly, if the child qualifies as disabled under Section 80U, the income remains exempt.

Example:

- Your 15-year-old son has ₹20,000 FD interest → Added to your income.

- On the other hand, if he earns ₹10,000 from YouTube videos through his own efforts, the income is not clubbed.

Tax Benefit:

- You can deduct ₹1,500 per child (max 2 children) from clubbed income.

3. Transfer to Daughter-in-law [Section 64 (1)(vi)]

Rule: Assets gifted to son’s wife without payment → Income taxed in your hands.

Example:

- You gift a house to daughter-in-law → Rent income is your taxable income.

4. Transfer for the Benefit of Spouse or Daughter-in-law [Section 64 (1)(vii) & (viii)]

Rule: The Income Tax Department clubs income with you if you transfer assets to any third party (like a trust or friend) that ultimately benefits your spouse or daughter-in-law.

5. HUF Income from Transferred Assets [Section 64 (2)]

Rule: If you transfer personal assets to HUF (Hindu Undivided Family) without payment → HUF’s income from those assets is your income.

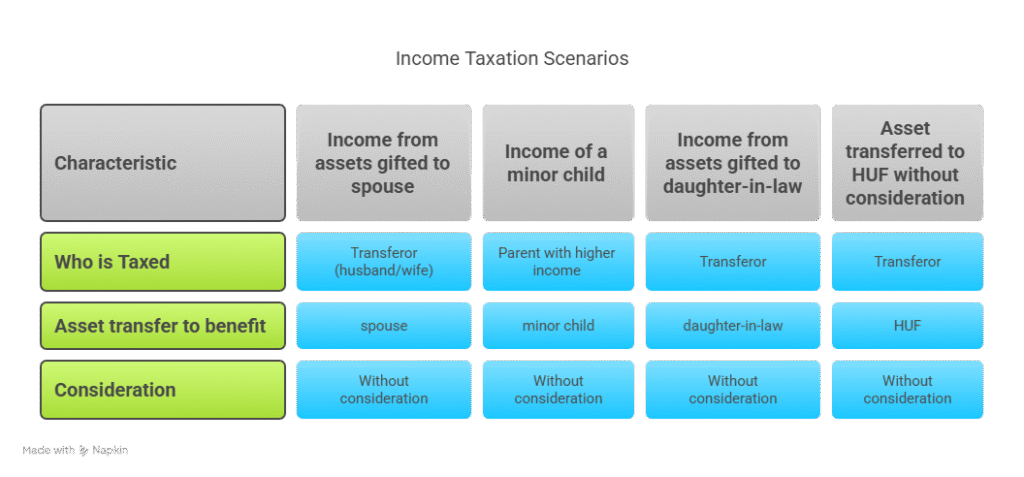

Summary Table

| Scenario | Who is Taxed |

| Income from assets gifted to spouse | Transferor (husband/wife) |

| Income of a minor child | Parent with higher income |

| Income from assets gifted to daughter-in-law | Transferor |

| Asset transfer to benefit spouse/daughter-in-law | Transferor |

| Asset transferred to HUF without consideration | Transferor |

Important Notes:

- Clubbing applies only when there is no adequate consideration (payment) for the transfer.

- It does not apply to income earned by relatives from their own efforts or business.

- Section 64 does not apply to adult children (i.e., children aged 18 or above).

Conclusion

Section 64 Income Tax provisions ensure fair taxation by and prevents individuals from using family members to sidestep tax laws. If you’re planning to transfer assets or income to relatives, make sure you Understand the clubbing rules to avoid unexpected tax liabilities.

FAQs

Clubbing of income means adding certain incomes (like spouse’s or minor child’s earnings) to the taxpayer’s income to prevent tax evasion through family transfers.

The tax authorities tax the transferor on income from assets gifted to a spouse without adequate payment.

Yes, a minor child’s income (except from personal skills/labor) is clubbed with the parent’s income (whichever is higher).

No, if you gift money/assets to your wife and she earns income (e.g., interest, rent), it will be clubbed with your income under Section 64.

No, Section 64 does not apply to adult children (aged 18+). Their income is taxed separately.

The tax authorities do not club income from a child’s own skills or talent (like acting or content creation). They only club passive income such as fixed deposit interest.

The law taxes the transferor on income from properties gifted to a daughter-in-law without fair payment.

Yes, parents can claim a deduction of ₹1,500 per child (max 2 children) from the clubbed income.

No, if the transfer is at fair market value (adequate consideration), clubbing does not apply.

1. Transfer assets for adequate consideration (e.g., sell at market price).

2. Invest in the child’s name only after they turn 18.

3. Use legal tax-saving options like joint investments with proper documentation