Ultimate Tips for Filing ITR Before 15th June – Pros, Cons & Deadlines You Must Know

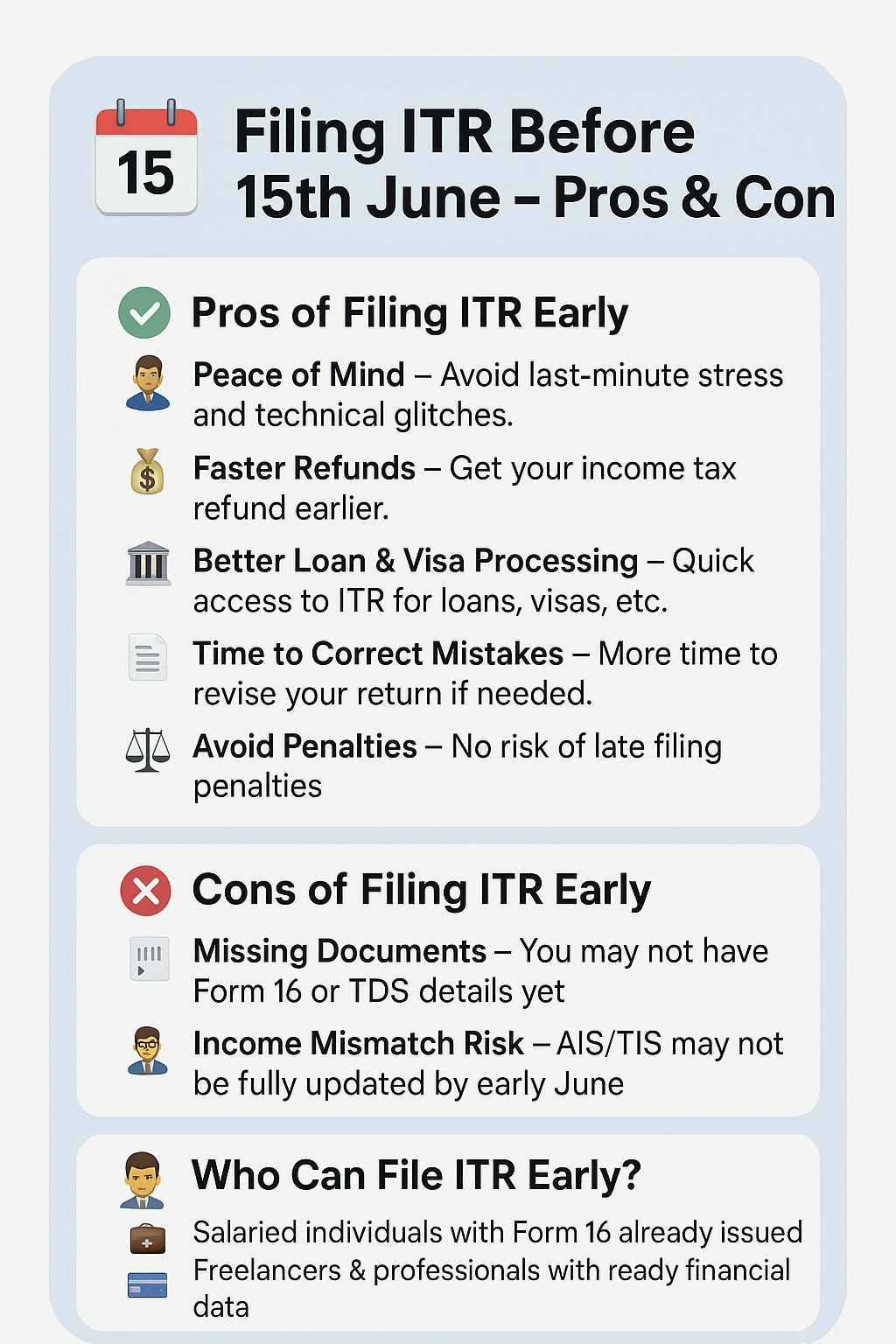

about filing ITR before 15th June, with emojis and clear pros & cons, plus eligibility info: Benefits of Filing ITR Before 15th June 🧘♂ Peace of Mind – Avoid last-minute stress and technical glitches. 💰 Faster Refunds – Get your income tax refund earlier. 🏦 Better Loan & Visa Processing – Quick access to ITR for loans, visas, etc. 📑 Time to Correct Mistakes – More time to revise your return if needed. ⚖ Avoid Penalties – No risk of late filing penalties. Drawbacks of Filing ITR Too Early 🧾 Missing Documents – You may not have Form 16 or TDS details yet. 🧮 Income Mismatch Risk – AIS/TIS may not be fully updated by early June. 🔄 Re-filing May Be Needed – If income details change, you’ll have to revise. Who Can File ITR Early? Who Shouldn’t File ITR Early? Pro Tip Always match your ITR with AIS/TIS & Form 26AS before filing to avoid mismatch notices from the IT department. Different types of ITR and who should file. What Is Form 26AS in income tax What Is AIS in income tax What Is SFT in income tax Contact us for ITR Filing At Finance And Tax Guide, we are offering comprehensive income tax return filing services designed to make the tax process as smooth and stress-free as possible. Our team of experienced tax professionals ensures accurate and timely filing, helping you minimize liabilities and maximize potential refunds. Whether you’re an individual, a small business, or a corporation, we take the time to understand your unique financial situation, offering personalized solutions to meet your needs. Trust us to handle the complexities of tax filing so you can focus on what matters most to you. Don’t rush to file your ITR What can happen? What if you file early? What’s the issue The tax paid and income details on the tax portal may not match with ITR filed What should you do? Real-Life Illustration for ITR filling Reflected in Form 26 AS: 15 June (15 day processing) SFT reporting, which captures high-value transactions (required for AIS) by entities, is also on 31st May If the ITR is filed with nine-month income, details will get updated later. Have to file a revised return when Form 26AS gets updated Conclusion iling ITR before 15th June can save you time and help you receive refunds faster — but only if your data is complete. Always verify your AIS, Form 26AS, and TDS details before submission. When in doubt, wait till mid-June or consult a tax advisor. Contact US FAQs